JHVEphoto

I published my thesis on “buying” on Marsh & McLennan (New York Stock Exchange: MMC) In February 2024, he highlighted the growth opportunity of revenue shifting towards higher growth areas including digital, climate resilience, sustainability, internet, affordable healthcare, etc. On April 18, the company reported strong growth in the first quarter of FY24, With organic revenue growth of 9% and operating profit growth of 11%. Property and casualty premiums will likely grow at a high-single-digit rate in 2024, contributing to the company’s strong growth momentum. I repeat a “buy” rating at a fair value price of $220 per share.

Strong margin expansion and premium growth

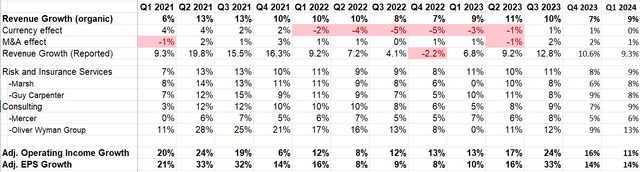

In the first quarter of fiscal 2024, Marsh & McLennan achieved organic revenue growth of 9% and adjusted EPS growth of 14%, with risk and insurance services growing 9% year over year.

Marsh & McLennan quarterly earnings

The strong growth momentum is due to two factors:

- As I noted in my previous coverage, Marsh & McLennan is strategically positioned in high-growth areas including digital, climate resilience, sustainability, internet, affordable healthcare and so on. These high-growth areas enable the company to grow at a faster rate than the general average. Insurance market.

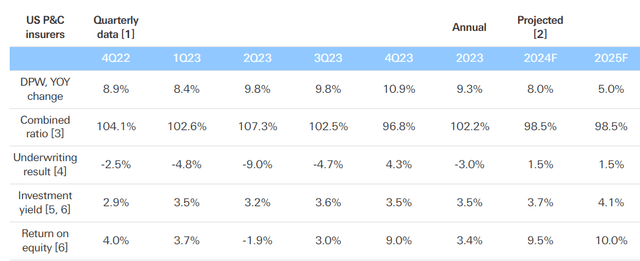

- Due to inflation, U.S. property and casualty insurance premiums are expected to grow 8% in 2024, after 9.3% growth in 2023, according to the latest report from Swiss Re. Even as inflation begins to decline, insurance companies are still raising premiums to offset higher administration and repair costs. Some parts of Marsh & McLennan’s business are related to insurance premiums; So the company will continue to benefit from this trend.

Swiss Re report

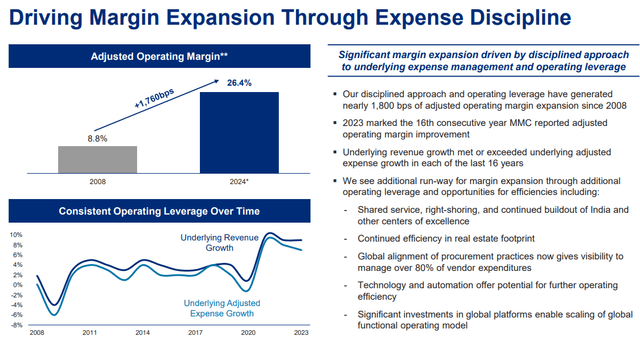

On top of strong revenue growth, Marsh & McLennan also achieved strong margin expansion during the quarter. I expect the strong margin expansion to continue in FY24 for the following reasons:

- As highlighted in my previous reports, Marsh & McLennan’s new growth businesses carry higher margins, and the company has strategically shifted its revenue mix toward these higher-growth, better-margin businesses, contributing to margin expansion over time.

- Marsh & McLennan effectively managed operating costs in areas such as staff recruitment, SG&A and back office, as detailed in the slide below. During the earnings call, their management had a very positive tone about margin expansion in the near future.

Marsh and McLennan’s presentation to investors

FY24 forecast

I expect the company to achieve 9% organic revenue growth in FY24 because:

- Risk and insurance: I expect the risk and insurance business to grow at least at the same rate as insurance premiums, assuming market share stabilizes in FY24. As such, I expect the risk and insurance business to increase by 9% in FY24.

- Consulting business: It’s a little more discretionary compared to the insurance business, as organizations can delay these services. Amid a challenging macro environment, I assume the company’s advisory business will grow 6% in FY24. It’s worth noting that some advisory businesses, such as Retirement Plans and Retirement Consulting, are quite resilient even during a weak macro environment.

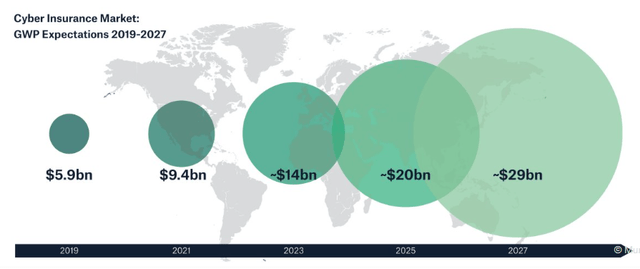

- New growth areas: According to a Munich Re cyber insurance report published in April 2024, the global cyber insurance market is expected to grow from $14 billion in 2023 to $29 billion by 2027, indicating a compound annual growth rate of 17.8%.

Munich Cyber Insurance Report

Regarding environmental, social and governance (ESG) issues, enterprise clients are paying more attention to ESG initiatives due to public interest and regulatory requirements. For example, in March 2024, the Securities and Exchange Commission (SEC) adopted rules to strengthen and standardize climate-related disclosures for public companies. Enterprise clients need an ESG database and related advisory services to meet their environmental, social and governance obligations. As such, I expect Marsh & McLennan’s ESG business to continue to grow rapidly in the near future.

Overall, I assume that new businesses, including cyber, ESG and digital businesses, will contribute an additional 1% growth in total revenues. As such, I believe the company will achieve 9% organic revenue growth in FY24.

evaluation

For normalized revenue growth after FY24, I expect Risk & Insurance revenue to grow 6%, assuming 4% growth from premiums and 2% growth from market share gains.

Additionally, after fiscal year 2024, the consulting business should grow by 6%, a growth rate in line with its historical trend.

As such, the overall organic revenue growth rate is expected to reach 6%.

In addition, Marsh & McLennan is actively engaged in the mergers and acquisitions market. I assume that the company will allocate 4% of total revenue to mergers and acquisitions, contributing 2% growth in total revenue.

On the margin side, I assume the company can generate operating leverage from both compensation and SG&A expenses. Assuming leverage of 10 basis points from compensation/benefits, and 10 basis points from SG&A, I assume a margin expansion of 20 basis points in the model.

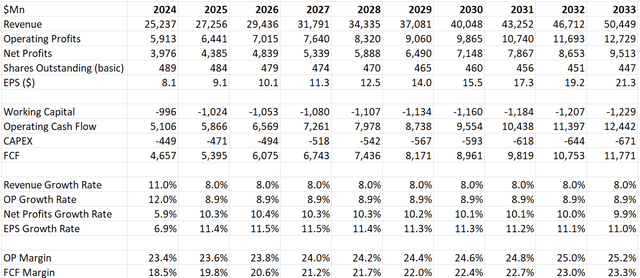

Marsh and McLennan DCF – author’s calculations

The weighted average cost of capital is calculated as 7.3% with the following assumptions:

- Risk-free rate: 4.25% (10-year US Treasury yield)

- Beta: 0.76 (Seeking Alpha)

- Equity risk premium 7%; Cost of debt 7%

- Equity balance: $12.3 billion; Debt: $13.4 billion

- Tax rate: 25.5%

Deducting all future free cash flows and adjusting the net debt balances, the fair value is calculated at $220 per share, according to my estimates.

Main risks

Marsh & McLennan has some trading exposure in the reinsurance market. Insurance Journal reported that the reinsurance market is expected to peak in 2024 due to increasing rates and tightening terms and conditions, which could lead to a weak market situation in 2025. A weak reinsurance market would create some growth headwinds for Marsh & McLennan In 2025. FY25.

In addition, Marsh & McLennan is a low volatility stock with a low beta. When the Fed starts lowering interest rates, the market may favor growth and high beta stocks, which could put Marsh & McLennan stock into a penalty box. However, a company’s intrinsic value is determined by its long-term growth potential.

Conclusions

I admire Marsh & McLennan’s leadership position in the insurance consulting industry and its strategy to expand into high-growth areas. They are poised to benefit from premium growth in FY24, in my view. I repeat a “buy” rating at a fair value price of $220 per share.