Richard Drury

We’ve previously covered 3M (New York Stock Exchange: mmm) in January 2024, discussing an oversold condition at that time, due to highly effective cost optimization efforts, increased net profit, and almost resolved legal settlements.

We rated the stock a Buy at the time, with We concluded that the dividend investing thesis remained strong with the potential for capital appreciation as headwinds subside.

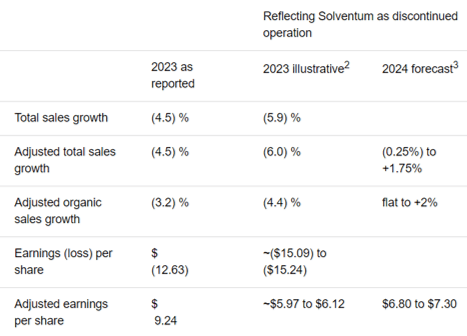

Since then, 3M has posted a total return of +12.2%, beating the broader market by +11.6%. With Solventum’s (SOLV) divestment completed as of April 01, 2024, and its balance sheet healthier, we believe the company remains well positioned to invest opportunistically in its long-term growth.

For now, readers may want to temper their near-term expectations, as the uncertain macroeconomic outlook remains a headwind for industrial/consumer companies as a dividend cut nearly halves yield.

Otherwise with Being a smaller and focused company, we maintain our Buy rating, especially since upside support has already been established at $76.

MMM is leaner and healthier – thanks to the SOLV filtration process

Currently, MMM reports double-digit Q1 2024 earnings on April 30, 2024, with adjusted revenues of $7.7 billion (included QoQ/+0.8% YoY) and adjusted EPS of $2.39 (-1.2% QoQ/ +21.3% per year).

With the divestment of SOLV effective from April 1, 2024 onward, readers may expect the second quarter of 2024 to present a separate segment for discontinued operations, resulting in several adjustments to the company’s overall financial reporting.

This is particularly because management continues to highlight impacted demand in industrial specialties and the consumer sector, negating the strong organic growth reported in the automotive/electronics sector, with keen readers keeping a better eye on its near-term performance.

Otherwise, based on MMM’s growing operating margin of 21.9% (+1 point QoQ/+4 point YoY) and free cash flow margin of 10.3% (-15.7 points QoQ/-1.3 point YoY). In the first fiscal quarter of 2024, it is clear that the ongoing restructuring efforts have been accretive.

This is while allowing management to intensify its investments in water filtration systems across its global factories along with other growth opportunities, as noted in the extensive capital expenditures of $1.61 billion in fiscal year 2023, $1.74 billion in fiscal year 2022, and $1.63 billion in fiscal year 2023. Fiscal 2021, compared to the pre-pandemic average of $1.4 billion, as they also aim to complete their litigation obligations related to water purification using PFAS before the end of 2025.

The eventual improvements are also due to a significant reduction in headcount by -7K per year to 85K as of December 2023, and the divestment of SOLV will likely result in another drastic reduction, based on the latter’s “global team of approximately 22K employees”. From the most recent deposit.

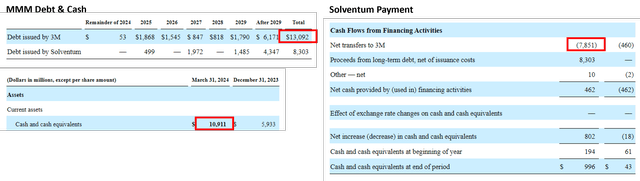

Debt/Cash MMM

Seeking alpha

Meanwhile, the divestment of SOLV has already contributed to MMM’s balance sheet, with the latter only reporting $13.09 billion of adjusted debt (embedded quarterly/+1.1% y/y) and $10.91 billion of cash/equivalents in the fiscal quarter. 1st of 2024 (+83.9% QoQ/+185.6% YoY), meaning a much lower net debt of $2.18 billion (-69.5% QoQ/-76% YoY).

Much of the QoQ tailwind was attributable to the divestiture of SOLV, with MMM retaining $7.85 billion in proceeds following the spin-off.

As with most divestitures, adjusting the dividend is prudent, given the significant structural changes at the top/bottom of the company moving forward, especially since the divested healthcare segment consists of $2.03 billion/25.3% of its total net earnings And $1.6 billion / 26% of its net profits in fiscal year 2023.

However, we can also understand why there is some hesitation for dividend-oriented investors, with MMM’s free cash flow to dividend ratio falling significantly from 65.4% in fiscal 2023 to 40% going forward.

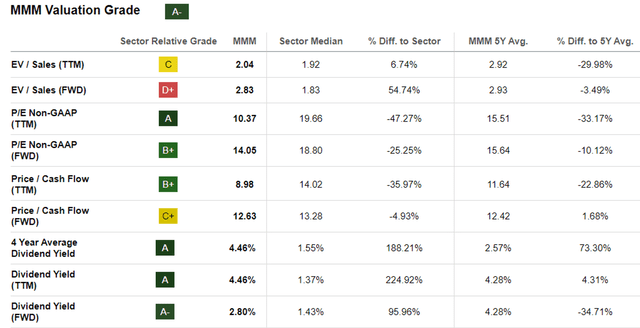

The change in payout ratio also ended Dividend Aristocrat’s 65 years of consecutive dividend growth, with the stock now offering an underwhelming forward yield of 2.80%, compared to its historical four-year average of 4.46% although it is still above the average The sector amounted to 1.43%. .

Then again, we think there’s another way to look at this, as MMM’s management has pledged to ramp up “investments in high growth, attractive end markets” specifically in automotive electrification, climate technology, and industrial automation. This is due to growing hybrid vehicle sales, ramping up renewable investments, and the AI boom, meaning cash flow will be put to good use while stimulating new growth opportunities.

If anything, readers should remember that the company is set to pay $10.3 billion in a public water supplier settlement through 2037 and $5.3 billion in a combat arms settlement through 2029, contributing in part to the lower dividend on Medium range.

MMM appears to be a reasonable value compared to its peers

MMM Guidance for FY2024

Seeking alpha

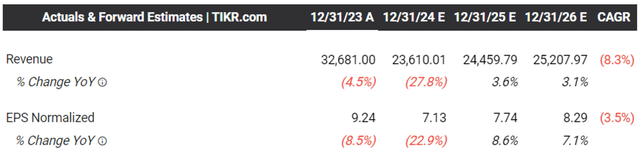

At the same time, MMM management is already guiding decent FY2024 pro forma revenue growth of +0.75% YoY and adjusted EPS growth to $7.05 at the midpoint (+16.7% YoY), meaning net income growth will accelerate thanks to the efforts Ongoing restructuring through 2025.

These numbers are not overly aggressive either, given that management has guided enhanced semiconductor market activities from the second half of 2024 onwards, with automotive OEM rates likely to grow once borrowing costs decline, as similarly observed in the transportation and electronics segment’s revenue growth to $2.1. B in the first fiscal quarter of 2024 (+1% QoQ/+2.4% YoY).

MMM Reviews

Seeking alpha

As a result of these developments, we believe MMM does not look expensive at FWD P/E valuations of 14.05x, despite the recent upgrade from the October 2023 low of 9.01x and the previous article at 12x.

This is because the stock remains inherently undervalued compared to its pre-pandemic 3-year average of 20.39x and its direct peers, including Honeywell International (HON) at 20.34x and DuPont de Nemours (DD) at 22.73x, implying… To an opportunistic upward return. – Rating of MMM upon successful transition from a renewable growth opportunity.

This comes in addition to the recent management change, and will likely result in a fresh start after the legal issues are settled and SOLV’s assets are liquidated.

Consensus future estimates

Consensus future estimates (tucker station)

This is particularly because management’s promising initial guidance for FY2024 has resulted in relatively accelerating growth in top/top net income at a CAGR of +3.3%/+7.9% between FY2024 and FY2026, respectively.

This compares to historical growth of +1.2%/+1.8% between FY16 and FY2023, thanks to the company’s leaner move and focus on moving forward.

When compared to HON’s top/bottom EPS growth forecasts of +5.1%/+9.1% and DD at +4.3%/+11% through FY2026, we think MMM’s discounted valuations at FWD P/E valuations of 14.05x look attractive here. .

So, is MMM stock a buy?Sell, sell, or hold?

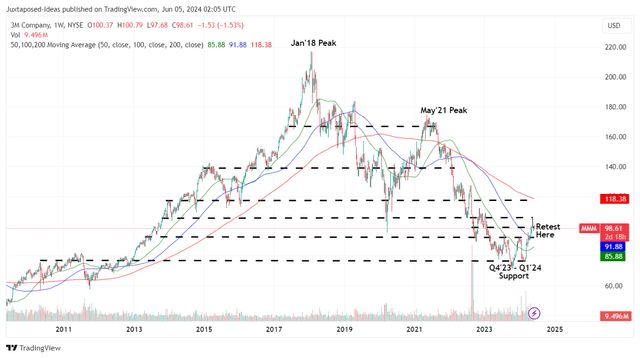

MMM 14Y stock price

Trading offer

Currently, MMM has already drawn strong support at the Q4 2023/1Q 2024 low at $76, while it has recovered significantly to retest the next resistance levels of $99.

Based on FY2025 consensus estimates for EPS of $7.74 (updated from previous article of $10.57, accounting for the impact of SOLV divestiture) and a 5-year normalized P/E valuation of 16.29x (consistent with previous article) , there appears to be decent upside potential of +27.8% to our long-term price target of $126.10 (updated from previous article of $172.10, representing the impact of SOLV stripping).

Assuming an upside rerating closer to MMM’s historical P/E valuations of 20x, as discussed above, we could see an upside long-term price target of $154.80 as well, resulting in excellent upside potential of +56.9%.

Combined with decent dividend yields, we believe it continues to offer double-digit return prospects, which has led to our rerating as Buy.

It goes without saying that interested investors may want to monitor the stock’s movement for a little longer and add according to their risk appetite and dollar cost averages.

Otherwise, they may consider adding after a moderate pullback to previous support levels of $91 to improve the margin of safety and the extended forward dividend yield of ~3.1%.