xijian

The first quarter is impressive

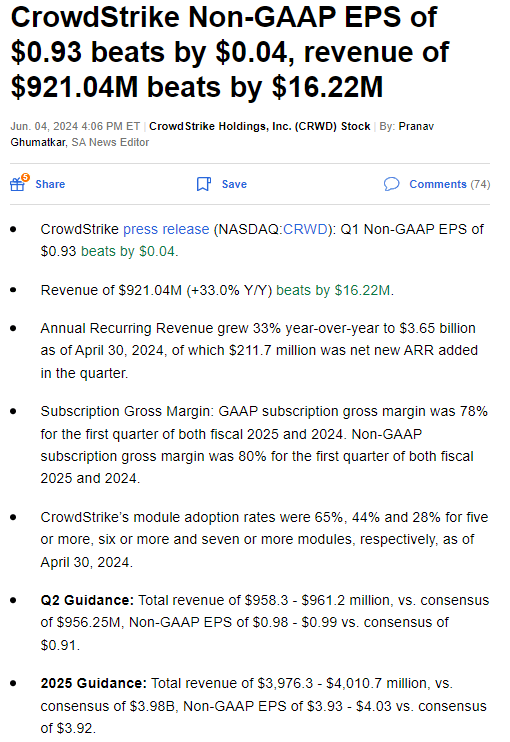

Crowd Strike (Nasdaq:CRWD) had a very strong first quarter with both the top and bottom winning. The company’s revenue increased 33% to $921 million, and its annual revenue rate grew to $3.65 billion, all of which exceeded expectations. Operating metrics continued to improve, and free cash flow margin was reached Record level of 35%. The market liked the results, and the stock rose more than 10% the next day. Other key findings can be seen below:

CrowdStrike’s first-quarter earnings (Searching for Alpha)

CrowdStrike displays impressive revenue performance and strong free cash flow generation. To sustain its growth, the company is implementing an aggressive product expansion strategy. It is expanding its TAM range by entering new markets with its new products (e.g. data protection, identity security, automation and SIEM solutions). This portfolio expansion helps the company capture a larger share of the growing cybersecurity market. look at me Numbers, this strategy seems to be working.

Continued consolidation in the cybersecurity market also benefits CrowdStrike. Customers are trying to integrate their legacy products with more integrated security solutions, and CrowdStrike is very well positioned for such a scenario. We see that this consolidation dynamic results in a significant number of customer wins for the company, which contributes to the company’s strong revenue performance.

Another driver of this strong performance is the high growth of the cybersecurity market due to the continuing rise in data breaches. This is leading to increased spending on cybersecurity by organizations, accelerating the growth of the overall market. Customers prefer CrowdStrike due to its market leadership position recognized by many research companies (such as Gartner and Forrester). These awards stimulate thought leadership, increasing demand for their solutions.

The main argument against CrowdStrike is its high valuation. While we acknowledge this concern, we also recognize that the company is quickly becoming one of the world’s leading cybersecurity companies. CrowdStrike is implementing an aggressive product expansion strategy, capitalizing on the consolidation trend and gaining market share from its competitors. We believe these three dynamics justify its outstanding valuation and position the company as an attractive long-term investment opportunity.

Strong Market Demand – Data breaches doubled in Q1

Despite the headwinds facing the SaaS market, demand for cybersecurity solutions remains very strong. There are three main drivers of this strong demand:

- Increasing the digitalization of companies,

- Growing geopolitical tensions

- The emergence of sophisticated cyber attacks that rely on artificial intelligence.

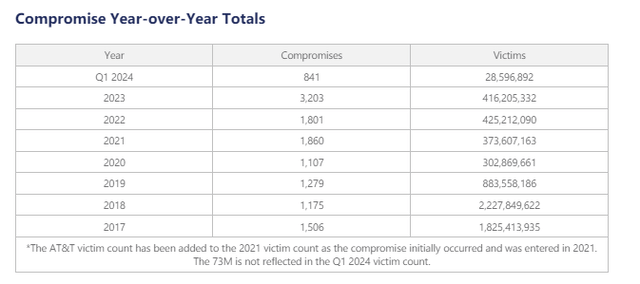

According to a report by the Identity Theft Resource Center, the number of data breaches in the United States nearly doubled in the first quarter of 2024 compared to the same period last year (see below).

Data Breach Analysis Q1 (Identity Theft Resource Center)

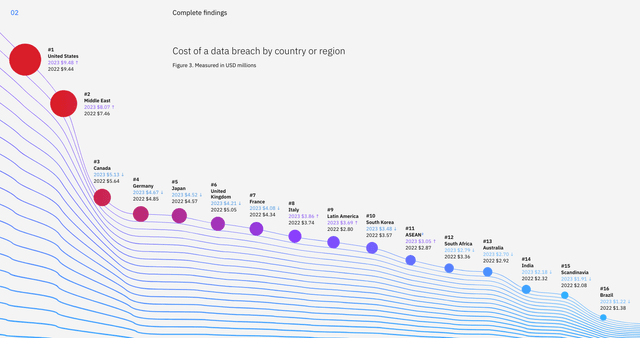

Along with the rate of attacks, the cost of attacks is also increasing for organizations. According to IBM’s 2023 Cost of a Data Breach report, the average cost of a data breach reached a record high of $4.45 million in 2023, an increase of 2.3% from the previous year. Over 3 years, the average cost increased by 15.3%.

IBM 2023 Cost of a Data Breach Report (IBM)

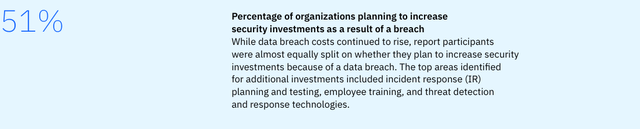

The continuing rise in cyberattacks is causing organizations to increase their investments in cybersecurity. It is clear that the demand for cybersecurity is driven by the increasing frequency and severity of cyber threats, which positions companies like CrowdStrike very favorably in the market.

IBM 2023 Cost of a Data Breach Report (IBM)

TAM expansion raises valuation

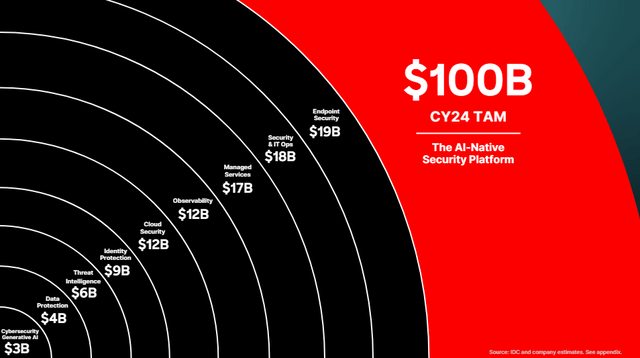

CrowdStrike’s growth strategy is to enter adjacent cyber markets in order to drive revenue growth. By expanding into these new markets, the company aims to capture a larger share of cybersecurity budgets. According to management’s commentary for the first quarter of the year, there appears to be very high demand for its new solutions such as SIEM, Identity Protection, Cloud Protection, Data Protection, Security Automation, and Charlotte AI. All of these products have significant market size and growth rates, and the company believes they add up to $100 billion in TAM volume (see below). The company expects TAM to grow to $225 billion by 2028, so the opportunity is very large indeed.

First quarter earnings presentation (crowdstrike)

This TAM expansion has far-reaching implications for the company’s future growth and valuation. This will increase customer retention, new customer acquisition and cross-selling opportunities. As a result, we believe CrowdStrike will maintain its growth momentum and increase its share of the large and growing cybersecurity market.

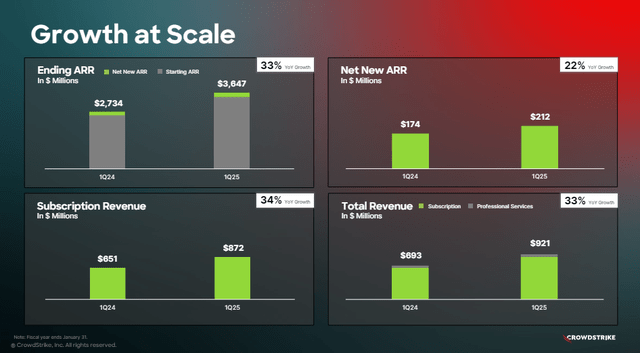

Revenue momentum and ARR are strong

CrowdStrike’s revenue momentum remains very strong, driven by high retention rates and new product adoption rates. The company generated revenue of $921 million (33% YoY) and subscription revenue of $872 million (34% YoY) and now has an annual revenue rate of $3.7 billion, which is growing at 33%. CrowdStrike has a long-term goal of reaching $10 billion within four years, which we believe will be achieved within three years.

First quarter earnings presentation (crowdstrike)

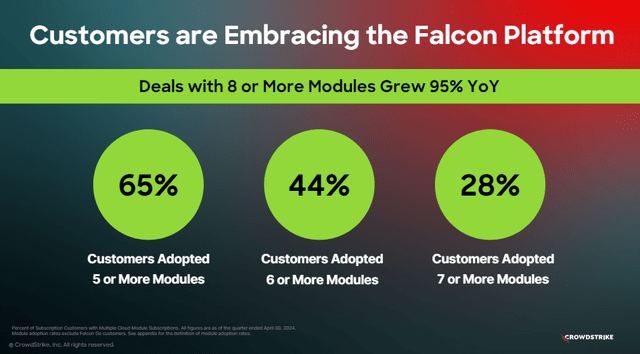

Deal-related metrics show the company is effectively executing its land and expansion strategy, with the number of deals containing eight or more units up 95% compared to the first quarter of last year. The proportion of customers with five, six, seven or more modules rose to 65%, 44% and 28% respectively, and the number of deals involving cloud, identity or SIEM modules more than doubled compared to last year (see below)

First quarter earnings presentation (crowdstrike)

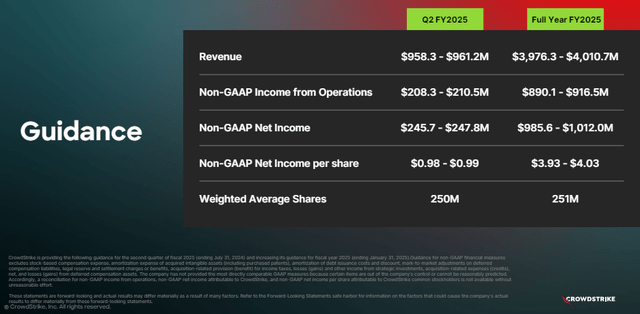

The management team expects revenue to be between $958 million and $961 million for the second quarter, representing 31%-32% year-over-year growth. For the full year, the company expects revenue of $3.98 billion to $4.01 billion, representing 30%-31% year-over-year growth.

We believe the company’s full-year guidance is somewhat conservative, reflecting the company’s cautious approach to managing expectations. The company is generally beating guidance by 1% to 2%, leading to expectations of revenue growth of 32%-33% for the full year.

Strong margins and free cash flow

CrowdStrike’s operating metrics continue to improve. Free cash flow margin reached a record high of 35%, compared to 33% a year ago. Gross margin was 80% for the first quarter, driven by data center investments and better pricing. Operating margin was also strong and beat expectations at 22% (vs. 17% last year).

First quarter earnings presentation (crowdstrike)

For the second quarter, the company has free cash flow margin guidance of 31% to 33% and operating margin guidance of 21% to 22%. Overall, we think CrowdStrike is successful in its margin expansion strategy. The company maintains its growth while also improving its profitability through disciplined operations.

Rating: Potential upside

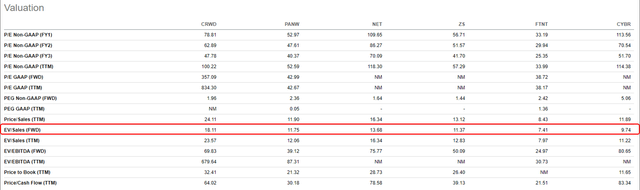

CrowdStrike is an expensive stock that trades at premium valuations. The market expects sustained high growth, driven by the company’s long-term potential. Management is on track for 31% growth in fiscal 2025, which is impressive given the overall SaaS market headwinds. The stock trades at a premium of 18 times forward sales, which is significantly higher than its software peers (see below).

Rating comparisons (Searching for Alpha)

Despite the high valuation, we believe there is still room for further upside. Our main issue to the upside is TAM expansion due to entry into new markets and market share gains from legacy vendor consolidations. We believe these strategic moves will drive revenue growth and set a higher valuation for the company’s revenue stream.

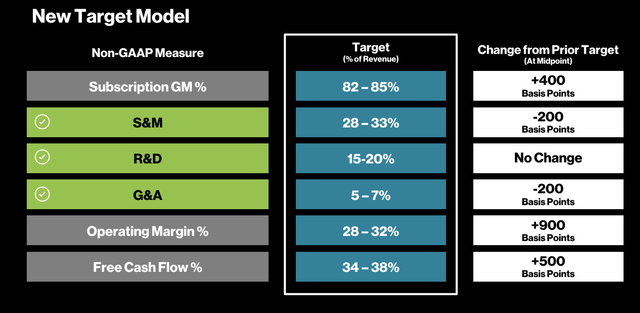

According to our DCF model, we expect CrowdStrike to reach revenues of $12.4 billion in fiscal 2029, implying a CAGR of 31%. Our key assumption is that 30%+ revenue growth will continue over the next five years due to the company’s significant TAM expansion and market share gains. The company’s long-term free cash flow margin target is 34%-38%; However, we believe it can reach 40% within five years due to the operating leverage capabilities of its Falcon platform.

CrowdStrike Investor Day (crowdstrike)

Our model assumes 9.7% weighted average cost of capital (WACC) as calculated using the GuruFocus WACC calculator. Additionally, we assume a terminal growth rate of 6%, based on expectations that the cybersecurity market will grow at a double-digit rate over the next five years and at a rate higher than GDP growth thereafter.

Based on a discounted cash flow model, we calculate a fair value of $412 per share, which implies a 20% upside from current price levels.

Discounted cash flow model (author)

Risks

The cybersecurity industry is moving very quickly due to advances in artificial intelligence and evolving threat factors. There is increasing competition and disruption in the cybersecurity market, both from existing players and new entrants. Another obvious risk is that CrowdStrike’s price and valuation will rise. The stock trades at double the multiple of its peers, and is priced for perfect execution. Any missing forecasts, or deficiencies in guidance can cause the stock price to collapse and cause price volatility. We’ve seen this recently with several SaaS companies, as their stocks have seen a major sell-off.

Conclusion

We are very optimistic about CrowdStrike’s future potential. The company consistently delivers revenue growth in excess of 30%, increases its margins, and generates record free cash flow. It has successfully implemented its growth strategy by expanding TAM and gaining market share from its competitors.

In terms of valuation, the stock may not be considered cheap, but we think it still has long-term upside potential. We rate the company a Buy with a price target of $412.