Boston Properties Stock: Tentative Signs That the Office Market Is Becoming Less Soft (NYSE:BXP)

Unicorn planet

boston real estate stocksNew York Stock Exchange: BXP) has performed strongly over the past year, up 20%, although it is still down more than 50% from five years ago, as rising rates and increased hybrid working have weighed heavily on office property valuations. Grant Because of my concerns about long-term occupancy trends, I rate BXP as “He sells” in November. Since then, shares have returned roughly 19%, slightly less than the market’s 21% gain — and in hindsight, I view this performance as closer to a ‘hold’ than a ‘sell’, given the positive return and relatively weak performance Just… Given this performance and updated financials, it’s a good time to revisit BXP. Recent developments have made me less pessimistic.

Seeking alpha

In the company’s first quarter announced on April 30yBoston Properties generated $1.73 funds from operations (FFO), which beat consensus by 2018 One penny. Revenue also rose 4.5% to $839 million. FFO was flat year over year, as higher rental income was offset by higher expenses. In particular, rent expense rose 8% to $314 million, and interest expense rose to $162 million from $134 million. In contrast, G&A decreased by 10% to $50 million.

High interest rates continue to push interest expenses higher. In fact, along with the results, it lowered its full-year FFO guidance to $6.98-$7.10, down $0.06, entirely due to higher prices. With the Fed unlikely to cut interest rates until late this year, at the earliest, Boston Properties’ floating-rate debt costs will remain high for longer. In addition, you will likely continue to roll over outstanding debt at higher yields. I find this guidance credible, a Fed rate hike unlikely, and staggered office lease maturities provide a solid near-term revenue outlook.

Between both the interest expense and rental trends, my concerns about BXP were more in the “gradual and sustained decline” camp rather than a sudden collapse in results, just given the nature of the office business. As a reminder, BXP operates a portfolio of high-quality office builders, mostly in central business districts. Unsurprisingly, 36% of its rent comes from Boston, followed by 25% from New York, 19% from San Francisco, and 15% from Washington, DC. 21% is leased to technology and media companies, 19% to legal services, and 17% to financial services. In general, banks and law firms had stricter in-office policies than technology companies.

Overall, BXP’s occupancy rate in the fourth quarter was 89.9%, which was flat sequentially. However, there is a tangible geographic difference with West Coast markets, which have a greater technology presence, recording significantly lower occupancy than the Northeast. While we can debate the future of work, I expect occupancy to remain structurally lower on the West Coast than in the Northeast, where technology companies are likely to continue with more flexible office attendance policies than the banking industry, for example.

Boston properties

Usually, weaker markets hurt lower quality players first. Let us consider a world where the demand for occupancy is 100%. Even the worst building has a tenant. This means that quality is becoming less important as potential tenants fight over which property is put on the market. However, as the market declines, potential tenants may become more choosy, meaning that older or faded properties may remain vacant for longer. This is indeed what is happening as vacancies skyrocket for “non-premium” properties. All other factors being equal, this will help BXP weather the ongoing office downturn better than lower-quality properties.

Boston properties

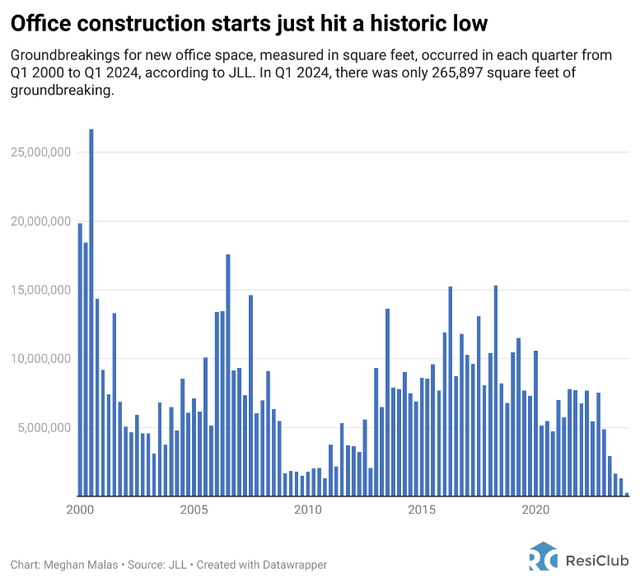

Another tailwind is the lack of office supply. It is difficult to find many people who are optimistic about office space, and financing to build new offices will likely be difficult to obtain. As vacancies across all types of properties are high (to varying degrees), there is little justification for building more office buildings. Unsurprisingly, new office construction has essentially stopped. New construction, with state-of-the-art facilities and amenities, competes more clearly with leading properties, and this lack of supply in the market has also helped to offset weak demand.

JLL

Last quarter, BXP was able to sign 894,000 square feet worth of leases for an average of 11.6 years. This represents an increase of approximately 1/3 from the first quarter of 2023, although down sequentially. The first quarter is typically seasonally softer for leasing, so I see the year-on-year increase as more pronounced than the quarter-over-quarter decrease. Additionally, there was 9.6% growth in second-generation rents in the first quarter, led by Boston at 21% while Los Angeles, Seattle and D.C. declined. In other words, BXP was able to sign new leases at higher rates than previous contracts. This is because although rents are lower than they were 4-5 years ago, with some leases being more than 10 years old, current market prices are still higher than those on the books.

This was positive, and BXP will need to maintain this leasing pace in order to maintain current occupancy, given 2.4 million SF exiting the lease this year. Fortunately, the Boston real estate company said at a conference on Tuesday that its rents are “significantly higher” than they have been for the past four quarters. Although overall demand for offices is not rising, it is winning a larger share of the market, given the quality of its real estate portfolio, the management said. Given the pressures on office demand, I do not expect improvements in occupancy, but this comment makes me think that occupancy may still be better than I had previously feared.

Now, overall, BXP has an average life of 7.5 years on its leases. As you can see, they overlap fairly well over the coming years. Even if it renews only 85% of its leases, its total occupancy will decline by less than 1% annually. Given recent resignation activity, a re-lease rate of 85% is likely conservative. About 30% of the portfolio is still due by the end of 2028, so the risk remains that occupancy is somewhat lower in several years than somewhat higher. The biggest challenge in the medium term is likely to be maintaining the same rental rate, rather than occupancy. As you can see below, the SF price has risen from $65 this year to $86 in 2026. That’s about 33% higher, which dwarfs the 9% gain in recent leasebacks. By 2027, we will be applying leases signed at the peak of the market, just before the coronavirus outbreak, rather than leases signed in 2013 when the market was still growing. Although they have similar amounts of space, the revenue impact is greater. That’s why I still think there will likely be pressure on FFO over the next few years.

Boston properties

Furthermore, rising interest expenses are a persistent headwind. Interest expense was $28 million higher than last year in the first quarter, a pre-tax impact of $0.18. I expect interest costs to rise further next year as it faces $1.36 billion in maturities in 2025, at a cost of just under 5%. If the Fed cuts interest rates two to four times over the next year, that will be of some help, and the pace of rising debt costs will slow significantly. I’d also like to point out that BXP has a highly leveraged balance sheet with its properties carrying $15.4 billion in debt, versus a 57% debt-to-capitalization ratio, from 33% pre-coronavirus. Prices are higher, the office market is weaker, yet BXP is now more leveraged than it was in the past, at nearly 8x EBITDA. I don’t expect to see interest rates rise further, but BXP’s leveraged financing structure represents a risk.

Boston properties

That’s why management has kept the dividend steady at $3.92 per year since 2020, as it sought to retain cash flow to support its development program. Currently, there is a $2.4 billion development pipeline. 54% pre-leased. This pipeline requires $1.2 billion in additional equity. BXP will hold about $450 million in cash after its dividend this year, which could go to fund its development needs. With this ongoing cash need and already high debt levels, I think it would be wise for BXP to maintain its payouts rather than increase them.

Boston Real Estate continues to face two ongoing secular pressures. First, higher interest rates put pressure on its balance sheet and income statement. Second, a staggered rent vesting schedule means that occupancy will not drop suddenly and sharply. Instead, BXP is essentially running on a treadmill, trying to gradually re-sign outstanding leases. However, as leasing rates are rising, this treadmill is gradually going faster, and it will take a stronger office market than current conditions for it to continue renewing leases at its current revenue rate. On the bright side, anecdotal evidence suggests that employers from Truist (TFC) to Walmart (WMT) are bringing workers back to their offices.

BXP shares have an 11.8% FFO return after the rally. After accounting for approximately $45 million in annual maintenance needs, the potential distributable return is 11.3%. I agree that the underlying picture is less negative than it used to be; However, this improvement appears to have been priced in. Assuming a required rate of return of ~10% to be a ‘buy’, BXP can offer this assuming FFO declines of 1.3% per year. That would be about $16 million in 2025, and assuming a refinancing rate of just 6%, BXP would face a $16 million increase in interest expense from its maturities. This does not provide room to cover operating costs and loss of occupancy.

Now, I see that “hold” refers to the potential for a market-like return or around 8%, and FFO can decline 3.3% and still achieve that, which happens to be the likely 2024 decline in FFO, based on management’s guidance. This seems to me like a reasonable central case, as interest expenses will be less of a headwind, but re-signing leases becomes a more difficult hurdle in the coming years. I still see business declining, but with BXP’s re-leasing efforts going well, limited supply, and a clear shift to at least hybrid versus remote work, I don’t see a strong case for a faster decline in FFO, unless the labor market softens or rates rise Significantly.

As such, I’m moving the stock to hold, after having been very negative for several months, with shares rising almost as much as the market. I don’t see market outperformance as likely, absent a significant drop in interest rates, as the less bad office fundamentals lie in the price. However, it can continue to deliver market-like returns even if the company continues its recent pace of decline, and its dividend is safe for several years. As such, I view the stock as a hold, but if we see shares heading towards $67 or a 10% distributable yield, I would take advantage of that to sell BXP, as the company will likely face downside pressure over time.