The growing piles of coins along with the piggy bank represent the power of the installation. erdikocak

There is a lot to be said about the strength of compound. Depending on which side of finance someone is on, this could be the case Their greatest friend or worst enemy.

My favorite quote that applies to compound interest is often attributed to Albert Einstein. Whether he said that or not is a matter for debate. In any case, this does not detract from the validity of the statement:

Compound interest is the eighth wonder of the world. Whoever understands it wins it. And who does not pay it? Albert Einstein (maybe)

To double down, I can focus on sound personal finance principles, like paying off credit card debt in full every payment cycle. Since Seeking Alpha is all about investing, this is what it is I will focus here today.

atmos energy (New York Stock Exchange: ATO) is one of the great acts on our main roster of The Dividend Kings that has caught my attention recently. From my perspective, this is a practical example of what a compound could look like in the real world.

Dividend distribution channel

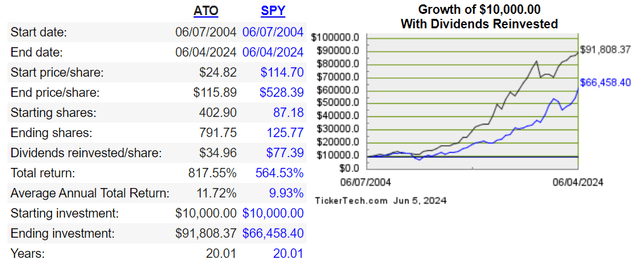

A $10,000 investment in regulated gas utilities in 2004 would now be worth $92,000 with dividends reinvested for each dividend channel. This is significantly higher than the $66,000 that the same investment amount in the SPDR S&P 500 ETF Trust (SPY) would be worth today with dividends reinvested.

Today, I will initiate coverage on Atmos Energy (hereinafter referred to as ATO) with a Buy rating. The reasons for this Buy rating which I will break down as I publish the article include:

- Potential for respectable future earnings growth. Catalysts for this include a growing customer base and significant capital investments planned through 2028.

- A strong balance sheet to fund growth ambitions.

- I believe the ATO can build on its 40-year record of dividend growth.

- The current stock price makes valuing the stock interesting.

Demographic trends and capital investments can fuel continued growth

ATO presentation to investors in May 2024

ATO is the largest distributor of pure natural gas in the country. The company’s network of approximately 73,500 miles of major distribution and transmission lines serves 3.3 million customers across the United States. The ATO rate base is about 65% and is concentrated in Texas. The remaining rate base is located in Kentucky, Tennessee, Virginia, Louisiana, Mississippi, Colorado and Kansas.

The company is divided into two operating segments:

- Distribution: This segment provides regulated natural gas distribution services to customers in the eight states listed above. The ATO expects this sector to account for two-thirds (66%) of net income in FY2024.

- Pipelines and Storage: This segment is involved in the transportation of natural gas for third parties and also owns and operates five underground storage facilities in Texas. The company expects the sector to contribute the remaining third (34%) of net income in fiscal year 2024.

ATO presentation to investors in May 2024

The ATO’s financial results in the first half of the financial year were a testament to the strength of its fundamentals. The company’s operating revenue fell 7.2% year over year to $2.8 billion during the first half.

At first glance, this seems to be a contradictory statement. How can a decline in operating revenues be an indicator of strength?

As a regulated natural gas company, the answer lies in the ATO’s business model. The company can pass on the cost of natural gas to its customers. This means that increases in natural gas costs are offset by increases in operating revenues.

In the first half, the opposite happened. Natural gas prices were lower, so ATO received less operating revenue via bills to its customers.

These top line headwinds were partially offset by the exceptional demographics of its service area. According to opening remarks by ATO President and CEO Kevin Akers during the second quarter 2024 earnings call, favorable hiring trends in Texas have helped the company’s client count grow. The company added 56,000 customers to its customer base in the 12 months ended March 31, 2024. More specifically, 43,000 of those new customers were located in Texas. The booming economy continues to attract net migration to the state.

The ATO’s lower operating revenue base came with a notable benefit: improved profitability. A 24% decline in purchased gas costs helped the company expand its net profit margin by 570 basis points to 26.5% during the first half of the fiscal year.

That’s how the ATO’s net income rose 18.1% compared to the same period last year to $743.3 million in that time. As a regulated company, the company recently issued additional shares to fund its growth spending. This resulted in a 5.3% increase in the weighted average number of shares to 150.5 million shares. However, diluted EPS rose 12.1% year over year to $4.93.

ATO presentation to investors in May 2024

Looking to the future, the ATO’s growth outlook is positive.

According to Akers, new home starts in North Texas rose 44.7% in the first calendar quarter of 2024. The annual rate of new home starts reached the highest pace since mid-2022. This should bode well for new customer growth in the coming quarters and years .

In addition, the ATO plans to invest $17 billion in capital spending until 2028. The majority of this spending will be allocated to improving the safety of its infrastructure, with the remaining spending allocated to meeting growing customer demand.

This is expected to push the overall rate base from $18 billion in FY2023 to a midpoint of $29 billion ($28 billion to $30 billion) by FY2028. This should support annual diluted EPS growth of The 6% to 8% that the ATO is targeting. .

The beauty of this capital expenditure is that it is also well supported by the business model. This spending is done through constructive pricing mechanisms that reduce regulatory price lag. This means that 90% of an ATO’s annual capital expenditure starts generating a return within six months of completion.

The permitted blended return on equity of 9.8% is well above the cost of capital. As evidence of what I mean, the ATO recently issued approximately $1.2 billion of debt/equity to support operations. Of that, $500 million were 30-year bonds at 6.2%, another $400 million were 10-year bonds at 5.9%, and $254 million were equity issues.

This is made possible by the ATO’s A- credit rating with a stable outlook from S&P. This is supported by an interest coverage ratio of 9.2 over the first half of FY2024 (unless otherwise stated or hyperlinked, all details in this subheading were in accordance with the ATO’s May 2024 investor presentation and the ATO’s Q2 2024 filing 10 -Q).

Shares can be worth up to $125 each

Fast Charts, FactSet

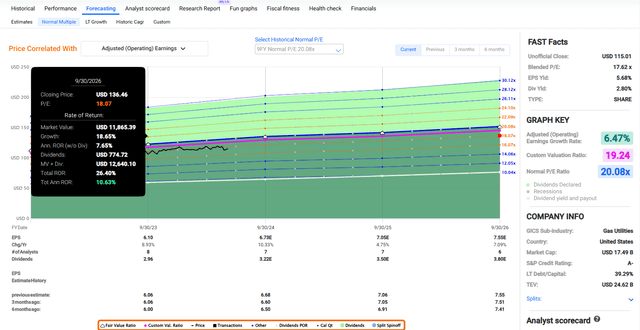

ATO shares look to offer decent value from the current share price of $115 (as of June 6, 2024).

Regulated natural gas utilities are priced at a current year P/E ratio of 17.1. This is moderately lower than the normal 9-year P/E ratio of 20.1 per quick charts.

Of course, for most of that time, the Fed observed a zero interest rate policy. Interest rates are likely to fall by about 200 basis points in the next two years or so. But this would still be higher than the average over the past nine years.

The company appears to be positioned to deliver diluted EPS growth in the high single digits year over year. This would also be in line with what it has accomplished historically.

These high interest rates are why I believe the fair value multiple will revalue at 10% below the normal 9-year P/E ratio. In other words, this is one standard deviation. This would be a fair value multiple of 18.1.

As the first half of FY2024 is completed for the ATO, I will weight 50% of my earnings inputs using FY2024 and the other 50% using FY2025. This gives me a 12-month forward diluted EPS forecast of $6.89.

Plugging that into a price-to-earnings ratio of 18.1, I arrive at a fair value of $125 per share. From the current share price, that means ATO shares are undervalued by 8%. If ATO returns to my fair value multiple and matches the growth consensus, cumulative total returns of 26% could be posted by the end of FY26.

I expect more of the same strong earnings growth

In my view, the ATO’s 40-year dividend growth streak that makes it a dividend aristocrat shows no signs of ending anytime soon. This is enough to get an A+ grade from Seeking Alpha’s Quant System for profit consistency.

ATO’s 2.8% forward dividend yield is well below the utilities sector average of 3.9%. That’s why it received a D+ grade for forward dividend yield from Quant.

ATO makes up for this lower income with its high dividend growth rate. The company’s profits have compounded at 8.9% annually in the past five years, better than the industry average of 5.2%. This is why the quantitative system gives the ATO a grade of B for the scale.

The most recent 8.8% dividend increase suggests that earnings growth isn’t slowing down either. An examination of the ATO’s payout ratios supports similar earnings growth going forward. That’s why Quant System expects dividend growth per share of 8.7%.

Thanks to Zen Research Terminal, ATO’s 48% EPS payout ratio is much better than the 75% EPS payout ratio preferred by industry rating agencies.

The company is scheduled to pay $3.22 in earnings per share in fiscal 2024. Against analyst consensus of $6.73 for the fiscal year, the payout ratio will be 47.8%. Combined with the strong balance sheet, that’s why I also think earnings growth could come before earnings growth for the foreseeable future.

Risks to consider

ATO is an exceptional all-rounder, but there are risks to the investment thesis.

Geographic concentration represents one set of risks for a company. This is because approximately 65% of the ATO’s distribution rate base is in Texas (according to the ATO’s May 2024 investor presentation). The good news is that this regulatory environment has been favorable and this is expected to remain the case in the coming years. If this does not hold up, it could be a drag on the ATO’s growth prospects.

Additionally, this geographic concentration means that the company’s infrastructure is vulnerable to natural disasters. If serious natural disasters occur, they may interfere with ATO operations. In a worst-case scenario, a company’s infrastructure could be damaged beyond the insured amounts. This could erode the ATO’s earnings power.

The occurrence of any of these events could also result in a downgrade of your credit rating by rating agencies. If this happens, the ATO’s cost of capital could rise. If this amount rises significantly enough, it could jeopardize the company’s plans to spend $17 billion on upgrading/expanding infrastructure through 2028.

Summary: The attractiveness of the total return potential of Dividend Aristocrat

ATO is a utility that checks all the boxes for me. According to FAST Graphs, the company’s diluted EPS has grown in 17 of the past 20 years. Population growth across the ATO’s service areas and capital spending plans should translate into healthy growth going forward. The company must also have the means to continue paying high single-digit annual dividends. Finally, the stock offers a large margin of safety for me to rate it as a buy now.