Tadamichi

It’s always interesting when commodity prices rise. The market produces different narratives as to why prices will continue to grow indefinitely. This applies to all commodities, from oil to orange juice or cocoa beans. For example, Michael Hartnett of Bank of America recently noted:

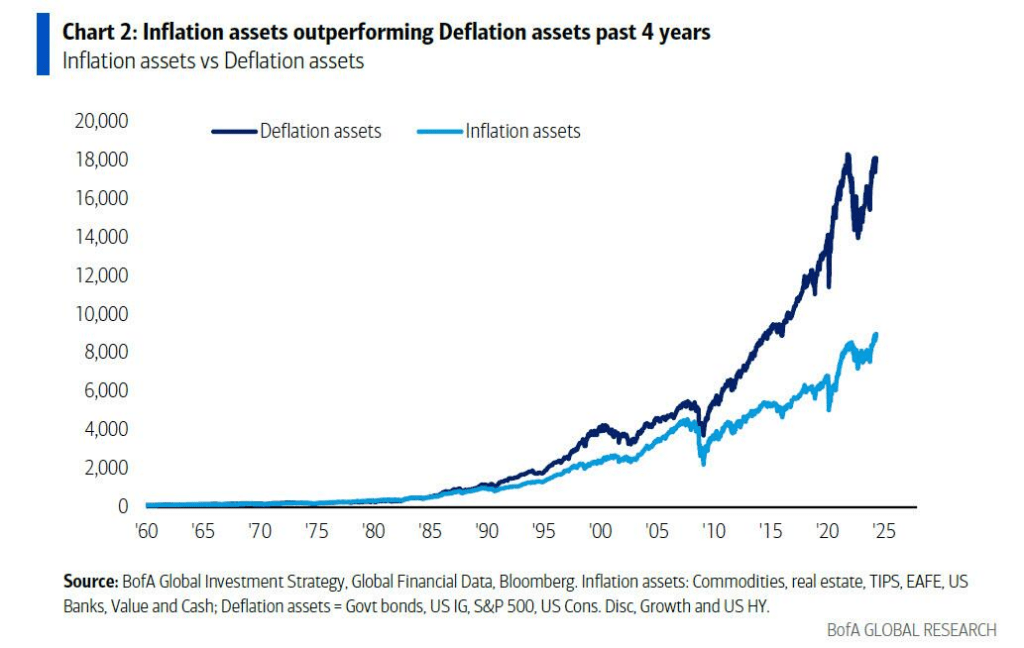

The 40-year period from 1980 to 2020 was an era of disinflation: thanks to fiscal discipline, globalization, and peace, markets saw “deflation assets” (government and corporate bonds, S&P, growth stocks) outperform “inflation assets” (cash, commodities, Tips, EAFE, Banks, Value). As shown below, “deflation” averaged 10% per year versus 8% for “inflation” over the 40-year period.

But a regime change in the past four years has flipped the roles, and now the “wonderful” inflation assets are delivering annual returns of 11% versus 7% for deflation assets.

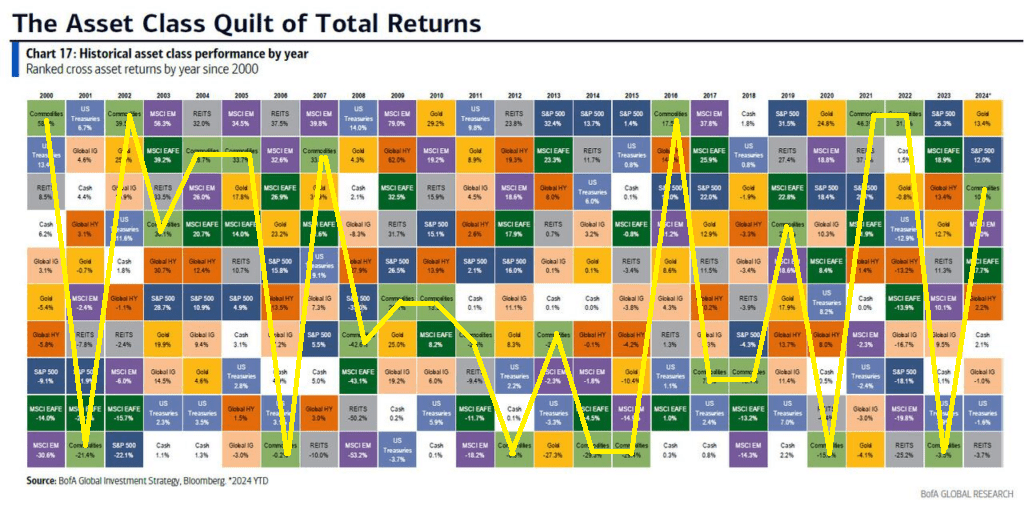

It should be noted that this is not the first time that markets have trended toward a “commodity cuckoo.” Latest episode In 2007 it was “Peak Oil.” However, most importantly, this time will be no different. As shown below, commodities regularly see an uptick in performance and are the best performing asset class in a given year or two. This performance then reverses sharply to the worst-performing asset class.

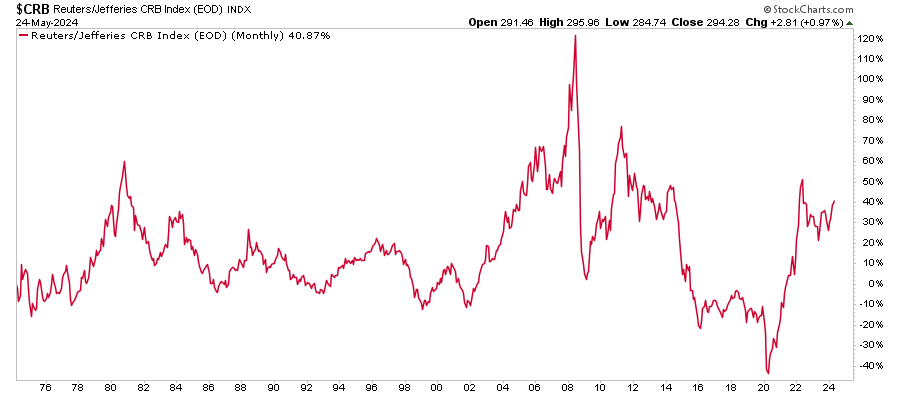

This performance “Boom and bust” It has been around since the 1970s. The chart below shows the performance of the commodity index over the past 50 years. On a buy-and-hold basis, investors received a total return of 40% on their investment. This is because, along the way, there have been amazing rises in commodities followed by huge falls.

This brings us to the big question? Why do commodities regularly boom and crash?

Why do commodities boom and crash?

The problem with the idea of a structural shift towards commodities in the future, and why this has not happened in the past, comes down to commodity price drivers.

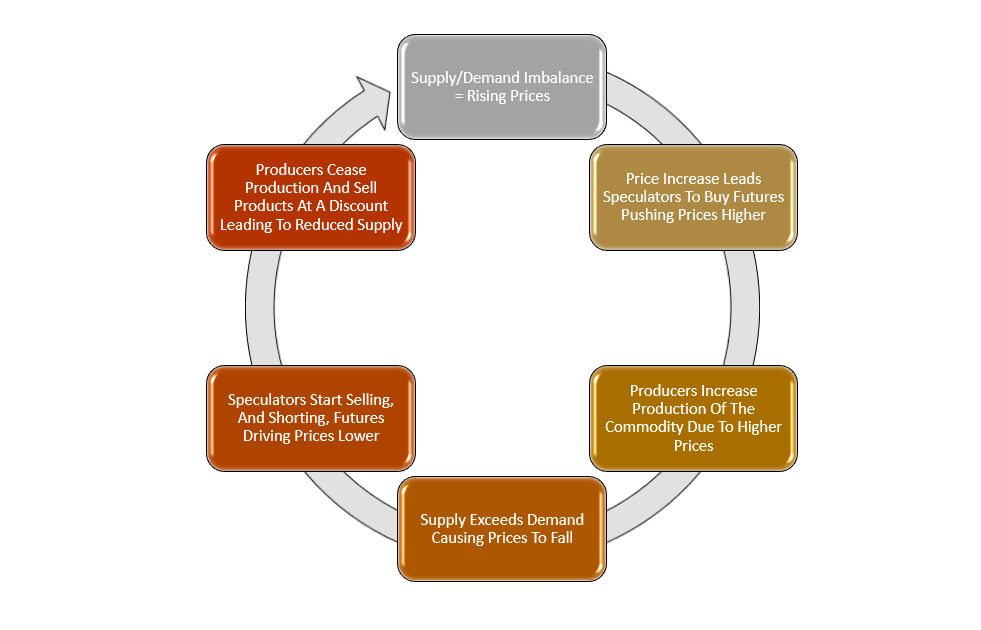

Here is a simplified example.

- During the commodity cycle, The first stage of commodity price increases is due to rising demand that exceeds current supply. This is often seen in orange juice, where drought or infestation has wiped out the season’s crops. Suddenly, the current demand for orange juice greatly exceeds the supply of oranges.

- As orange juice prices rise, Wall Street speculators begin bidding up the price of orange juice futures. As orange juice prices rise, more speculators buy futures contracts causing the price of orange juice to rise.

- Growers have canceled plans to produce lemons and increase the supply of oranges in response to rising orange juice prices. As more oranges are produced, the supply of oranges begins to exceed the demand for orange juice, leading to an abundant supply of oranges. The excess supply of oranges requires producers to sell them at a cheaper price; Otherwise they will rot in warehouses.

- Wall Street speculators start selling their futures contracts as prices fall, Pushing the price down. As prices fall, more speculators dump their contracts and sell short orange futures, causing prices to fall further.

- As orange prices collapsed, farmers stopped planting orange trees and started growing lemons again.

- Then the cycle repeats.

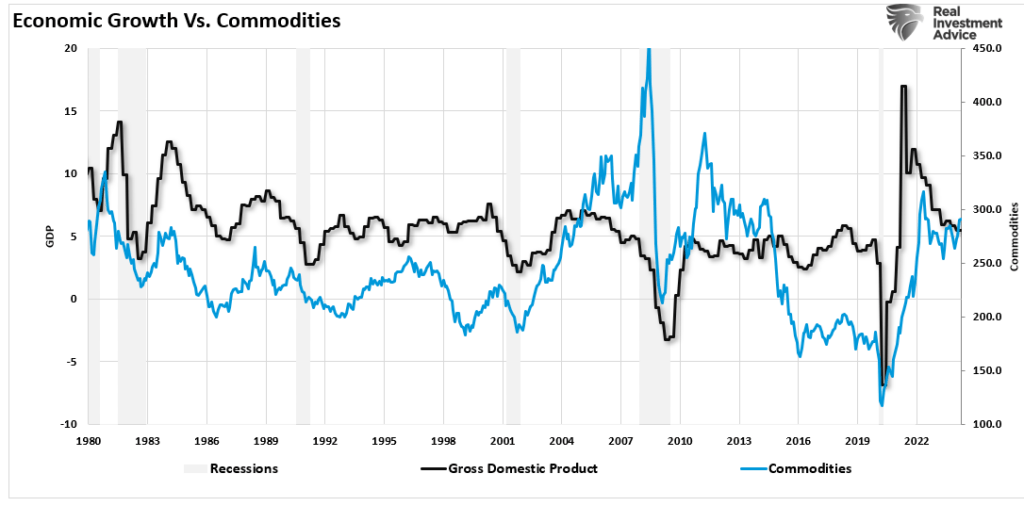

Moreover, high commodity prices threaten the same. as always, “High prices are a cure for high prices.” If orange juice prices become more expensive, consumers will consume less, resulting in decreased demand and a buildup of supply. The following chart of goods compared to nominal GDP shows the same thing. Whenever there is a sharp rise in commodity prices, this leads to a slowdown in economic growth rates. This is not surprising since consumption represents about 70% of GDP.

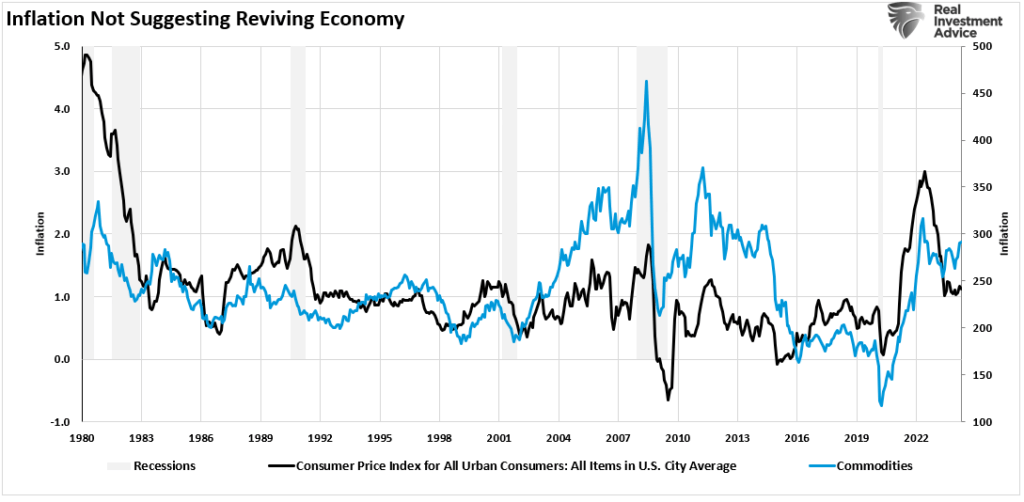

There is also a high correlation between commodities and inflation. It should be clear that when commodity prices rise, the cost of goods and services also rises due to higher input costs. However, price increases are constrained because consumers are unable to purchase those goods and services. As mentioned, the result of higher prices is lower demand. Decreased demand leads to lower prices or inflation.

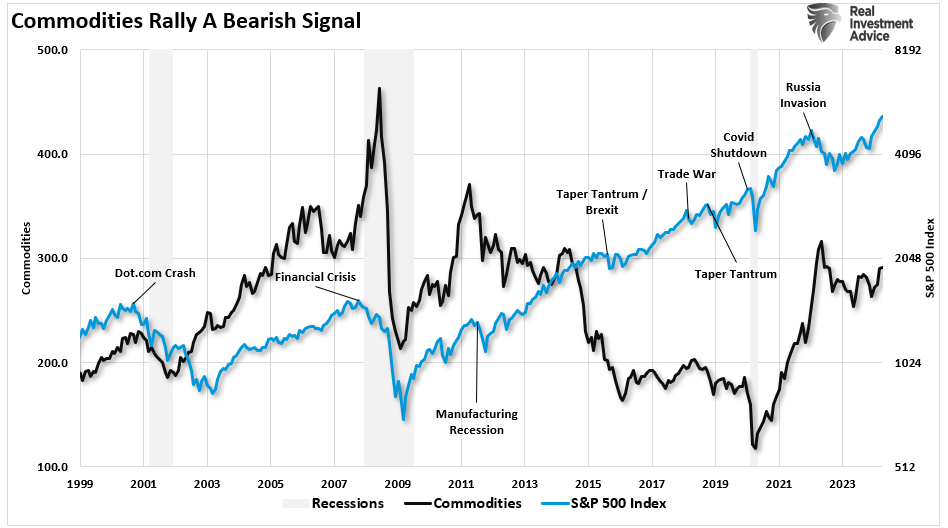

This is why hard asset trades frequently end poorly, despite the most enthusiastic media coverage.

Difficult asset trades tend to end badly

Commodities and hard assets in general can be an exhilarating and profitable ride up the road. However, as shown in the long-term chart above, this trade tends to end poorly. Commodities have repeatedly led recessions and recessions in markets.

Will this time be different? This is unlikely to be the case for two reasons.

As we discussed, prices rise (economic inflation) It is a cure for high prices because it reduces demand. As shown above, as consumers reduce spending, demand will decline, leading to lower inflation in the future.

Second, as the country moves toward a more socialist profile, economic growth will remain capped at 2% or less, with deflation remaining a constant long-term threat. Dr. Lacy Hunt suggests the same thing.

“a companyContrary to conventional wisdom, a decline in inflation is more likely than an acceleration of inflation. Since the price deflation in the second quarter of 2020, the annual inflation rate will rise temporarily. Once these base effects are exhausted, cyclical, structural, and monetary considerations suggest that inflation will ease by year-end and fall below the Fed’s 2% target. The inflationary psychosis that has gripped the bond market will fade in the face of this persistent deflation.“

As he concludes:

“The two main structural impediments to conventional economic growth in the United States and globally are the massive debt burden and deteriorating demographics, both of which have worsened as a result of 2020.“

The last point is crucial. As liquidity drains from the system, the debt burden affects consumption as income is transferred from productive activity to debt servicing. As such, demand for goods will weaken.

While commodity trading certainly is “Bright – Mazhar” As liquidity increases, one must be careful of its eventual reversal.

For investors, deflation remains an issue “A trap in the making” For hard assets.

There is nothing wrong with owning goods; Just don’t forget to take profits.

Original post

Editor’s note: The summary points for this article were selected by Seeking Alpha editors.