hirun

Investment thesis

The ideas of artificial intelligence or artificial intelligence are very popular these days because this new technology is making some investors very rich. For example, NVIDIA Corporation (NVDA) stock is up 210.9% in the past year.

Brand Engagement Network, Inc. (Nasdaq: BNAIL) began trading as a public company on March 15, and provides an opportunity to invest in the field of conversational artificial intelligence. Its products go beyond traditional chatbots because they can learn to respond almost like actual humans.

It is an interesting field due to its ability to bridge workforce gaps, increase productivity, and enhance user experiences. But potential investors should be careful.

BEN, as the company is commonly known, is a relatively new company with emerging technology in a competitive field. Prudent investors need to see several quarters of results, especially improving results, before spending their money.

About the brand Sharing network

The company started as Blockchain Exchange Network, or BEN, in Jackson, Wyoming in 2018. In its first-quarter 2024 earnings report, its first as a public company, it described itself as an artificial intelligence platform provider. She added that its applications help companies “improve customer experiences, improve cost drivers, mitigate risks, and enhance operational efficiency.”

In a recent press release, the company also calls itself a provider of conversational AI technology with human-like AI avatars. It “provides highly personalized, multi-modal (text, voice, vision) interaction with AI, with a focus on industries where there is a huge workforce gap and an opportunity to transform how consumers interact with networks, service providers and brands.”

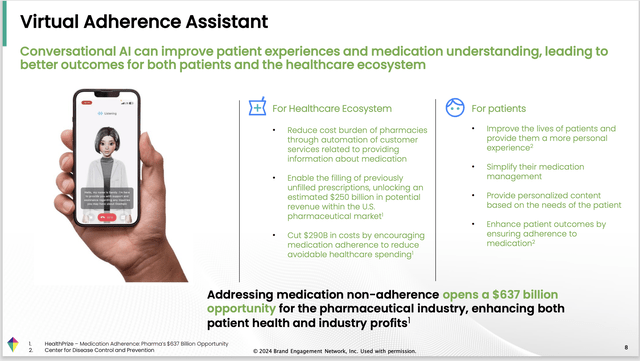

How does all this work? In its April 2024 investor presentation, the company provided this example of its technology:

BNAI Virtual Assistant (investor presentation)

As the slide indicates, one of the first markets management is targeting is health care. On February 27, it announced a pilot partnership with MedAdvisor Solutions, which the companies expect to deliver improved patient experiences at pharmacies. According to a press release announcing the deal, BEN’s products will replace chatbots to deliver a personalized conversational experience for patients.

On June 4, a press release announced the collaboration with the Department of Surgery at NewYork-Presbyterian/Weill Cornell Medical Center. In this arrangement, the companies will “explore the use of BEN AI assistants to improve access to healthcare and support patients, as well as ongoing training in the use of new technologies in healthcare settings.”

The goal is to “improve real-world patient outcomes through the strategic use of BEN’s human-style AI avatars, which can see, hear, understand, remember, analyse, speak, and gesture in the same way a person would in an interaction with a human.” Interactions.”

In the automotive market, the company launched “BENAuto” in partnership with AFG companies (Automotive Financial Group). It’s a deal that will provide “unique AI assistants” that will help AFG with various elements of auto financing.

Comments: I am encouraged by BEN’s statement above about focusing on industries with “huge workforce gap(s).” That suggests the company is keeping pace with the overall trend in North America at least, where retiring baby boomers and work-life constraints among some young people are causing problems for employers.

I also found the company more reliable because of its partnership with Weill Cornell Medical College, a major and respected healthcare organization. Another partnership is with OSF HealthCare, a 16-hospital system in Illinois and Michigan.

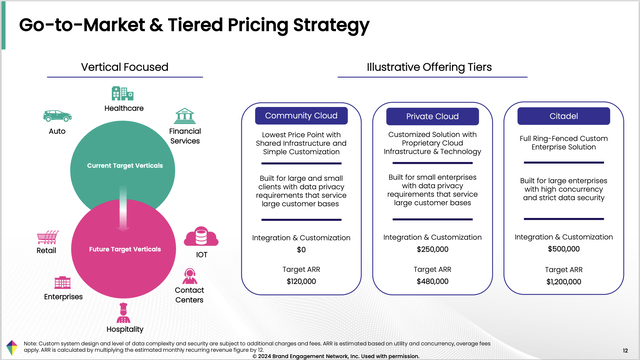

Marketing and pricing

This slide from the investor presentation shows how BEN plans to generate revenue (ARR stands for Annual Recurring Revenue):

BNAI marketing and pricing segment (investor presentation)

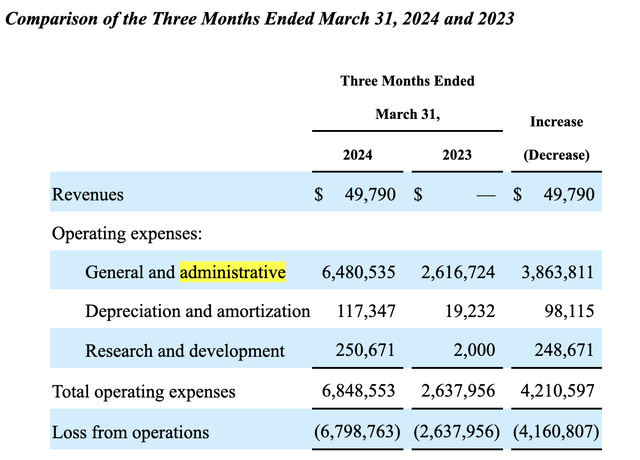

In its Q1 2024 earnings report, BEN reported revenue of $49,790, versus zero revenue in the same quarter last year.

Financial results

Against those revenues for the first quarter of 2024, we find the usual expense categories. The most important of which is general and administrative costs amounting to $6,480,535. Obviously, this represents many multiples of its revenue, but it is not unexpected for a small company to go public.

As the company noted in its first-quarter 10-Q report, “The increase was primarily due to transaction costs of $3.2 million incurred in connection with the closing, an increase of $1.5 million in employee-related costs, an increase of $1.0 million in professional fees, and an increase of $0.2 million in promotional costs, and a $0.1 million increase in insurance costs, all related to the expansion of our operations and includes a total of $0.1 million of insurance, professional services and payroll expenses resulting from the acquisition of DM Lab Co., LTD (“DM Lab”). In May 2023.

The 10-Q abbreviated income statement compares BEN’s first-quarter performance with its non-public predecessor (known as Pre BEN):

BNAI’s income statement for the first quarter of 2024 (Brown 10-S)

Comments: We would need to see significant increases in revenue to be confident in the viability of BEN’s products.

Liquidity of brand engagement network

At the end of the first quarter, BEN had $3.3 million in cash, derived from proceeds from the transaction with AFG, sales of common stock, warrants, and debt issuances. On the liabilities side, it had $20.2 million in debt.

Its finances received a boost on May 29 when a group of existing shareholders bought another $4.95 million worth of stock and warrants. Additionally, the same group agreed to provide additional funds if the company is unable to raise another $3.25 million by October 31. This would bring the total to $8.2 million ($8.25 million according to the press release).

Adding $3.3 million to $8.2 million means the company will have $11.5 million in cash, plus debt proceeds that it uses in the short term. However, potential investors should be cautious, especially until we see its cash burn rate in the next quarterly report.

a race

Given the successes of Nvidia and other major players in the AI space, there is no shortage of competition in this space. Even in the conversational AI space, a quick search engine scan reveals that several companies are also in the race, including major players like International Business Machines Corporation (IBM) and Google/Alphabet (GOOG) (GOOGL).

If BEN is to gain a competitive advantage through conversational AI, it will need to exploit it quickly and effectively. Otherwise, it may fail or be acquired by a stronger company in the same field.

Growth plans

Following its acquisition of DM Lab Co, BEN valued its ongoing research and development business, an intangible asset, at $17.0 million (10-Q). If the company could generate 20% internal returns on this asset, for example, it would generate $3.4 million annually or $850,000 per quarter in available cash flow. This is not much when we take into account current expenses and interest payments.

There are tailwinds that help support strong revenue and cash flow visions, including workforce shortages due to demographics, growth in healthcare spending, and competition to deliver more effective customer service than ever before.

Internally, the costs of going public will decline and eventually disappear, helping the company achieve significantly better profit margins. At the same time, its marketing and sales strength must improve to boost revenue growth.

However, any estimates of future revenues and profits must necessarily be speculative. We’ll need to watch the next few quarters and years to see if BEN can capitalize on its $17 million worth of research and development.

Management and strategy

CEO Michael Zakarski was described in the investor presentation as having held multiple long-term executive positions, and more than 15 years of experience in the technology industry. He is also said to have experience driving growth, improving operations and leading product/solutions initiatives.

CFO Bill Williams has over 20 years of experience in corporate finance, legal, technology and management consulting. The presentation indicates that he has held various executive positions in several industries.

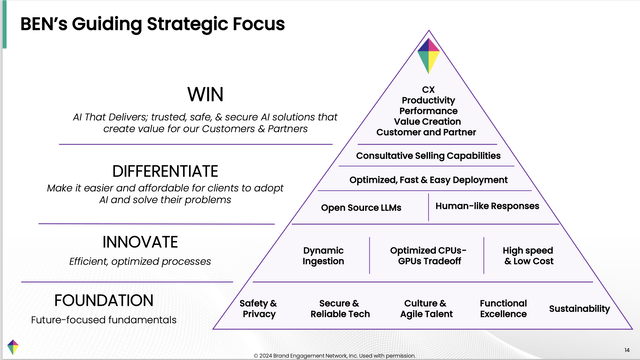

BNAI strategy slide (investor presentation)

This is an ambitious strategy, and I see tactical challenges. Looking at just the foundational level, can it develop the culture it wants, hire and retain the talent it needs, and achieve functional excellence in less than several years?

On the plus side, both the CEO and CFO have extensive experience, and what appears to be relevant expertise, to drive these tactics forward.

Appreciate this beginning

BEN has been publicly traded for just under three months, and during that time it has been volatile. As this chart shows, it peaked at $13.75 one business day after trading began. It then fell to $1.05 on May 15, before rising again the following month:

BNAI price chart (Searching for Alpha)

It doesn’t take a lot of news to cause the price to rise. On May 29, the company announced a $4.95 million private placement. By the close of that day, the price had risen from $1.27 to $2.64; Two days later, on May 31, the price rose to $5.44. It then drifted again and closed at $4.36 on June 6.

This was good news in the sense that it improved BEN’s financial flexibility, but since the offer included new shares, it also meant some dilution. So, there was a huge reaction to the mixed news.

Obviously, investors are trying to evaluate its value and what to expect from it.

Where does the price go from here? This is almost impossible to predict now, because the publicly traded company has so little history and because of the impact of the news.

Right now, we are in pure speculative territory. I believe the markets you serve now need BEN products and plan to serve them in the future. However, there are other players also active in those markets and we don’t know yet how well the company is being managed.

For most investors, patience will be key, waiting to see at least four quarters of results.

Risk factors

As I just said, this is a new company in an industry/sector that is notorious for trial and error. Will BEN be able to turn its IP assets into salable products and services, are there competitors dominating this AI field, and will the conversational field itself gain widespread acceptance?

Conversational AI will interact with users who will provide confidential information, including their health indicators and financial situation. If companies in this space, including BEN, cannot provide robust privacy controls, their future will be limited.

The company’s senior managers have experience with other companies, but will they be able to work together to develop an effective team? Will they be able to employ the types of expertise and experiences they need to grow?

We’ve seen a few encouraging partnerships, but we don’t yet know if the company will find enough partners and/or other clients to generate more profit than it spends on operating costs.

As a company grows, it will need increasing amounts of cash or debt. But adding equity capital means dilution and debt reduces its financial strength. This is not unusual for emerging technology companies, but should be taken into account when making any investment decision.

Conclusion

The Brand Engagement Network, or BEN, offers investors another way to invest in the booming AI industry. It is also an opportunity to get to the so-called “ground floor”.

But unless you’re a savvy tech investor or want to put a few stocks in a small corner of your portfolio, it’s best to take a wait-and-see approach. While the opportunities are great, so are the risks; This is a high-risk/high-reward technical situation.

I classify it as a hold, because I don’t yet see a clear path to profitability. It may exist, but I need to see the evidence before upgrading it to purchase.