William Potter

introduction

Is China investable? This is the first question one might ask before considering buying in this market. The answer is yes, with two important caveats: 1. That the stock has 20 frames, i.e. some reasonable sense of disclosure and audited financial statements and 2. that The ratings offset many other Chinese factors. The Chinese risks are lack of rule of law, the Chinese Communist Party (Chinese Communist Party) can change regulation, policy and capital as it sees fit, the company or adversely affected party has no recourse or protection, the rules can change and there is little that can be done about that. The other factors are geopolitical, where “competition” with the West leads to protectionism, trade barriers, etc., which can make doing business difficult. today I’m Follow-up On the KraneShares CSI China Internet ETF (NYSEARCA: Quip) which I analyzed last December as well as more recent articles about iShares China Great Value ETFs (Fxy) And then PDD (PDD).

summary

I upgrade KWEB to Buy from Hold due to a combination of positive factors that offset the unique risks to China. These factors include a lower relative valuation of 0.6x PEG (PE growth vs. EPS), a 5% EPS growth consensus upgrade, and a 7% price target upgrade vs. December analysis, which combine for 30% upside potential. In addition, the Chinese economy has bottomed out and is gradually regaining growth led by exports, and sentiment appears to have bottomed out.

The main risk of this upgrade is escalation of geopolitical tensions, primarily through further trade tariffs or barriers that could reduce China’s export growth and would therefore hurt domestic consumption on which most stocks in KWEB’s portfolio rely to reach the growth agreed upon above. And profits.

performance

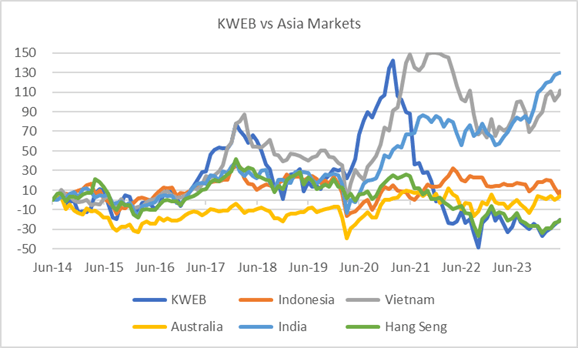

Over the past 10 years, the Chinese technology sector has risen and fallen to produce negative price gains of 20% which is in line with the Hang Seng Index (Hong Kong) where most stocks trade. This is in stark contrast to the market gains in India and Vietnam. The main reason for the collapse was the Chinese Communist Party’s decision to increase scrutiny and regulation in the technology sector, along with other sectors, which affected investor confidence and company results. At the same time, China has objected to overbuilding in the residential sector, which has not been matched by growth through exports or domestic consumption, leading to “weak” GDP growth, which many see as the new normal.

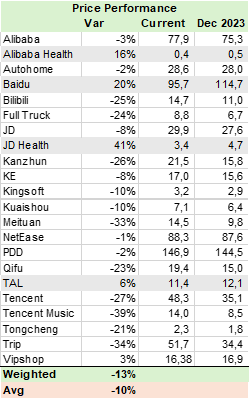

Year to date in 20224, the ETF is up 11%, however, in the table below, I calculated that the price return for current portfolio weights was a 13% decline with Tencent (OTCPK:TCEHY) down 27% and only four stocks It was a positive return.

performance (Created by author with data from Capital IQ) Performance to date (Created by author with data from Capital IQ)

Portfolio price target and reviews

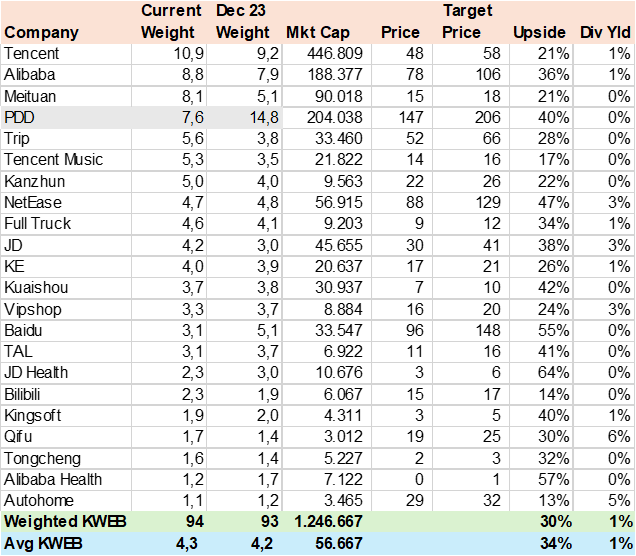

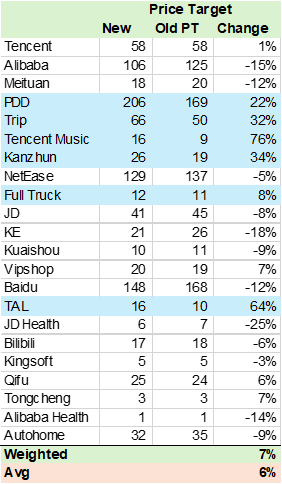

Using consensus estimates of 94% of the portfolio’s AUM, I calculate a 30% potential upside based on analysts’ current price targets to YE24 with PDD at +40%, and Alibaba (BABA) at +36% potential. Since my initial report, analysts have raised their price targets by 7% but BABA has seen a cut of 15% highlighting the company’s weak results and performance. Interestingly, Tencent Music (TME) received the largest upgrade with 76% in target price. In terms of weight changes, the PPD was reduced by 50% to 7.8% from a high of 14.8% likely due to the stock’s performance in 2023 requiring rebalancing on a free float adjusted market capitalization basis.

Consensus target price (Created by author with data from Capital IQ) Review target price (Created by author with data from Capital IQ)

Earnings per share and reviews

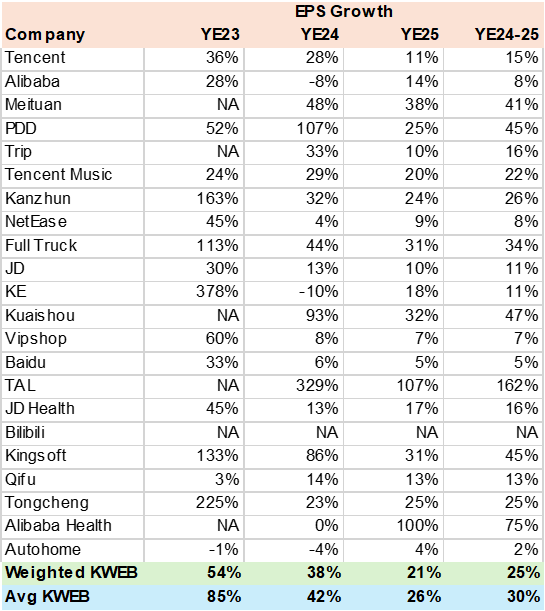

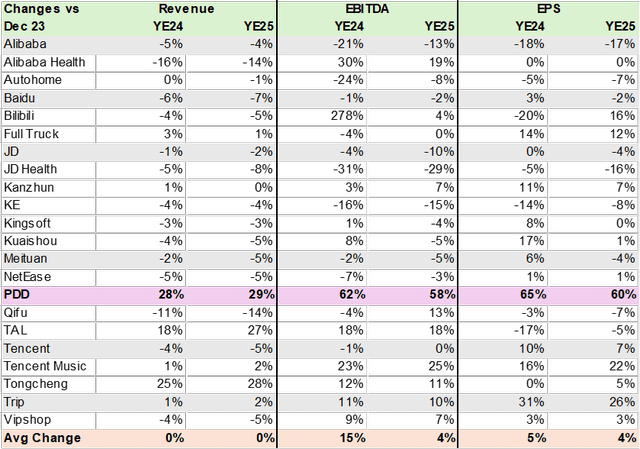

The market is estimating an EPS growth rate of 25% in the YE24-25 period. Educational stocks TAL and Alibaba Health have the highest estimated growth, while PDD and Meituan Dianping (MEIT) are the heavyweights in the portfolio that contribute the most while Alibaba is the primary draw. However, as we have seen, the outlook could be subject to sharp corrections, calling into question the earnings outlook for China’s technology sector. Analysts have increased 2024 and 2025 EPS by 5% and 4% on average, with PPD featuring a 65% increase in estimated EPS.

EPS consensus estimates (Created by author with data from Capital IQ) Consensus estimates (Created by author with data from Capital IQ)

evaluation

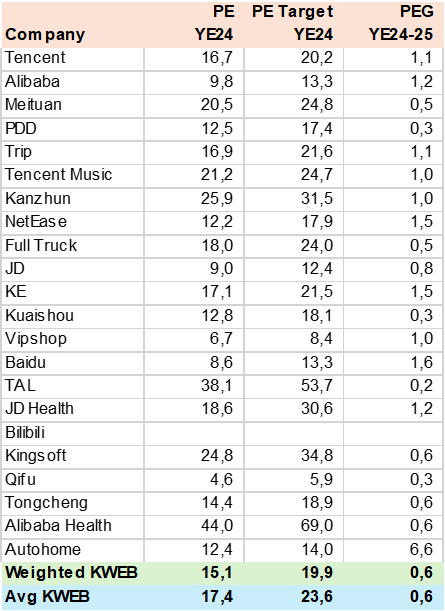

KWEB’s portfolio is cheap at 15x PE (versus 30x historically) on YE24 estimates and even more so with a PEG of 0.6x for the YE24-25 period. I’ve used consensus estimates and weighted PEG at 25% from YE24 EPS growth and 75% from YE25 EPS growth. This way, the relative valuation captures future growth that can be considered more consistent over the long term. This valuation discount versus the Nasdaq which trades north of 1.8x PEG may be excessive but would require improved regulation or at least an extended timeframe for positive macro and government news flow to bring the rate back.

Consensus evaluation (Created by author with data from Capital IQ)

Conclusion

I upgrade KWEB to Buy from Hold. Although my view on the risks facing China has not changed, it appears that the economy has bottomed out and so has sentiment. The portfolio’s current valuation is attractive given generally positive earnings revisions. The main risk is major geopolitical events.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.