Photoschmidt/iStock via Getty Images

We previously covered Broadcom (NASDAQ:Nasdaq:AFGO) in February 2024, to discuss why we finally upgraded the stock as a Buy, after several rounds of a Hold rating.

This is attributed to reasonable FWD ratings compared to Its peers and management’s very optimistic forward guidance for FY2024, with the consensus already being to moderately raise their estimates through FY2026.

Since then, AVGO has posted another 7.5% increase in stock gains, outperforming the broader market by +5.7% with $1.2K set as the minimum. Much of the tailwind was naturally attributable to accelerating profitable growth reported in the fiscal first quarter of 2024 and higher AI-related sales guidance in fiscal 2024.

The same promising trend has been observed in the market by AI market leaders, such as Nvidia (NVDA), Super Micro Computer (SMCI), and c3.ai (AI), with increasing demand for generative hardware. AI offerings break through the infrastructure layer to the SaaS layer.

Combined with the excellent returns to shareholders to date, we believe AVGO remains a buy option on every moderate pullback to improve the margin of safety, maintaining our bullish investment thesis on this generative AI play since our last article. Repeat purchase.

AVGO continues to be a compelling, creative AI game – thanks to the updated guidelines

For now, after the very insightful comments and promising future guidance from several Generative AI players in recent Q1 2024 earnings calls, we believe the market is eagerly awaiting AVGO’s upcoming earnings call on June 12, 2024.

For example, NVDA, the market leader in AI chips, reported impressive Q1 2024 revenue of $26.04 billion (+17.8% QoQ/+262.1% YoY) while revenue for the quarter was 2Y24 of $28B (+7.5% QoQ/+107.4% YoY), smashing consensus estimates of $22.03B and $26.8B respectively.

With SMCI, a complete server solutions company, also reporting strong 1Q24 revenue of $3.85B (+5.1% QoQ/+200% YoY) while guiding 2Q24 revenue of $3.85B. 5.3 billion (+37.6% QoQ/+143.1% YoY)), it’s clear that there remains “continued strength in demand for AI/ML computing and networking products from hyperscale customers.”

At the same time, we’re starting to see AI infrastructure productivity growth trickle down to the SaaS layer, as C3.ai similarly reported in its latest earnings call, with “exceeding the high end of both original guidance and analyst expectations.”

AVGO management highlighted the same, with Q1 2024 generating strong network revenue of $3.3 billion (+6.4% QoQ/+43.4% YoY) with “strong demand for dedicated AI accelerators.” “Resulting in increased network revenue guidance for 2019. Growth of +35% YoY in FY2024.

This compares to its original guidance of +30% year-on-year, meaning its offering remains the top choice for many super-expanders thus far.

At the same time, AVGO expects fiscal 2024 to generate higher AI-related revenues of more than $10 billion, compared to the original guidance of $7.5 billion provided in the fiscal 2023 Q4 earnings call and the $6 billion annualized amount reported About in the fourth quarter of 2023.

As a result, we think AVGO’s Q2 2024 consensus estimates look somewhat conservative, with revenues of $12 billion (+0.3% QoQ/+37.4% YoY), and EBITDA estimates of $7.05 billion (-1.3% QoQ/+24.1% YoY), and adjusted EPS estimates of $10.84 (-1.3% QoQ/+5% YoY), with a possible beat Another performance increase.

This is particularly so because management has posted an impressive sixteen consecutive P&L wins since Q2 2020, and is also reiterating its FY2024 revenue guidance of $50 billion (+39.6% YoY) and EBIT and depreciation and amortization of $30 billion (+29.2% y/y).

These developments also underscore why we believe AVGO remains a productive and compelling AI play – thanks to elevated networking guidance in FQ1’24, adding further strength to its key investment thesis.

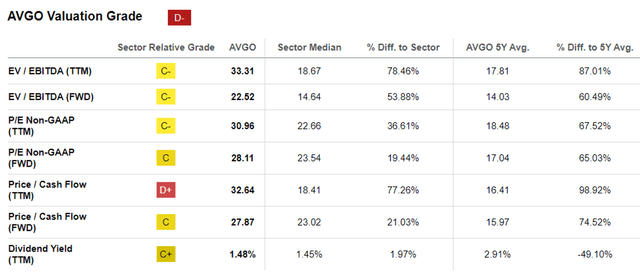

AVGO appears to be reasonably valued compared to its peers

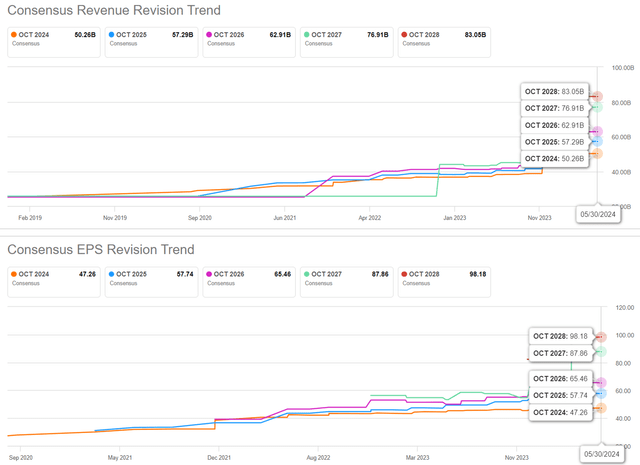

Consensus future estimates

Seeking alpha

For now, the consensus continues to raise their forward estimates, with AVGO expected to report accelerating gross/net profit growth at a CAGR of +20.7%/+15.7% through FY2026, compared to previous estimates of +18.6%. / +13.8%, respectively.

The higher estimates are likely attributable to AVGO’s remaining strong multi-year performance commitments of $27.7 billion (+36.4% QoQ/+21.4% YoY) in fiscal Q1 2024, adding visibility to its pipeline. higher in the long term.

At the same time, readers should note that management continues to report growing annual SaaS revenue of $18.19 billion (+148% YoY), albeit with SaaS gross margin deteriorating by 81.9% (-9.9 points YoY). The latter is mostly due to several factors. Time adjustments from the recent VMWare integration.

However, with SaaS revenue increasingly making up its sales at 37.9% (+17.4 points YoY), we believe AVGO may be at the forefront of the AI race, as accelerating SaaS growth will likely boost its future earnings as well. .

AVGO Ratings

Seeking alpha

As a result of these developments, we can understand why the market continues to give AVGO higher FWD EV/EBITDA ratings of 22.52x and FWD P/E ratings of 28.11x, compared to the previous article’s 20.16x/26.95x and the sector average of 14.64x/23.54. x, respectively.

We think the upgrade is actually reasonable, as AVGO’s value is still reasonable compared to the premium value embedded in the AI segment/its AI peers/key competitors, such as NVDA at 34.47x / 40.62x, and Advanced Micro Devices (AMD) at 54.45x / 47.49 x, and Intel (INTC) at 11.20x/28.24x, respectively.

This is especially because AVGO is expected to post decent gross/net profit growth at a CAGR of +20.7%/+15.7% between FY2023 and FY2026, (or normalized at +15.8%/+17.5% Between fiscal year 2019 to fiscal year 2026), compared to:

- NVDA at +43.7%/ +46.4% (or settled at +49.5%/ +61.4%),

- AMD at +19.2%/+40.3% (or settled at +28.3%/+41.6%), and

- INTC at +8.1%/ +34.7% (or settled at -0.7%/ -8.7%, due to ongoing PC correction/price cuts), respectively,

Which implies that AVGO is reasonably valued at FWD P/E valuations of 28.11x compared to its peers given the relative comparison in growth rates.

Needless to say, the VMWare merger has directly contributed to the deterioration of its balance sheet, with the company now reporting moderate Q1 2024 cash/equivalents of $11.86 billion (-16.3% QoQ / -6.1% YoY ) and current/long-term debt of $75.89B (+93.4% QoQ/+93.2% YoY), implying massive net debt of $64.03B (+155.7% QoQ/+140.4). % on an annual basis).

The same effect was also observed in AVGO’s Q1 2014 adjusted EPS of $10.99 (-0.6% QoQ/+6.3% YoY) QoQ, as annual interest expenses rose significantly to $3.7 billion. USD (+128% QoQ/+128% YoY).

However, with very rich Q1 2024 free cash flow generation of $5.35B (+13.8% QoQ/+37.1% YoY) and margins of 45% (-6 points QoQ/+ 1 on an annualized basis), we’re not really too concerned, especially since only $13.3 billion of its long-term debt matures in 2025, while the rest will last very well into 2051.

So, is AVGO stock a buy?Sell, sell, or hold?

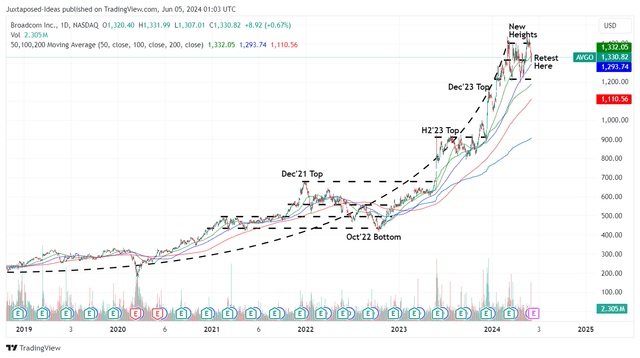

AVGO 5Y stock price

Trading offer

Currently, AVGO has established a strong support level at $1.2K and a clear resistance level at $1.4K, as the market oscillates between a bullish AI boom and bearish/extended inflationary pain, with the stock potentially trading sideways in the near-term.

For context, we provided a fair value estimate of $1.13K in our last article, based on FY2023 adjusted EPS of $42.25 (+12.2% YoY) and a prior front-end EPS of 26.95x.

However, based on AVGO’s LTM EPS of $42.91 (+1.5% from previous article) and high FWD EPS of 28.11x, the stock appears to be trading at a slight premium compared to our new fair value estimate of $1.2K. .

Based on the raised consensus of FY2026 EPS estimates from $62.21 in our previous article to $65.46 and a high forward P/E of 28.11x, there remains excellent upside potential of +38.3% to the long-term price target of $1.84K.

More importantly, AVGO’s rich $21 annual dividend cannot be ignored, as it allows long-term investors to continually reinvest on a quarterly basis while lowering dollar cost averaging.

As a result, we maintain our Buy rating, although there is no specific entry point as it depends on individual investors’ risk appetite.

Based on the current trading range of $1.2K-$1.4K, interested investors may want to add a moderate pullback to the lower end of the range to optimize upside potential, depending on individual dollar cost averages and portfolio allocations.

Risk warning

It goes without saying that with high P/E valuations come high expectations. This is especially true if AVGO reports any earnings losses and/or disappointing forward guidance, potentially leading to painful corrections.

This is especially because it is not yet clear when NVDA’s sales might eventually slow down, which could lead to the potential withdrawal of all other AI players like AVGO.

At the same time, with inflation remaining steady and a Fed pivot likely by Q4 2024, we may see a prolonged macroeconomic normalization process, with the stock market likely to remain volatile for a bit longer.

Finally, as the US-China trade war continues, we may see a portion of AVGO’s FY2023 China-related revenue of $11.53 billion at risk, something we similarly observed with Micron (MU), Advanced Micro Devices (AMD), and Intel (you are K).

Investors beware.