Ihor_Tailwind/iStock via Getty Images

Main thesis/background

The purpose of this article is to evaluate the Nuveen California Quality Local Income Fund (New York Stock Exchange: NAC) as an investment option at the current market price. This is a closed box whose purpose It is “to seek current income exempt from ordinary federal income taxes and California personal income taxes; its secondary investment objective is to enhance the value of the portfolio.”

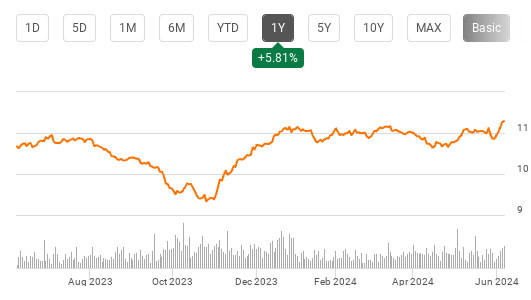

I cover the California Money market regularly, and as my followers know, there are plenty of options to choose from in the land of CEFs. But NAC has become interesting recently because it has recently seen a sharp increase in income and is run by Nuveen, a well-known player in this space. This fund is back on my radar because since late last year, this fund has been on a very strong run – offering investors tax-free and tax-free income. Capital increase:

NAC performance (Searching for Alpha)

With momentum on its side, but feeling a little neutral on the Muni space as a whole, I wanted to dig deeper into NAC specifically to see if a buy argument could be made here. Looking ahead to the second half of 2024, I see continued gains for CEF and believe a ‘buy’ rating is warranted. I’ll explain why in more detail below.

Increased income is always a plus

I’ll start with what may be the biggest development for NAC in the short term. This is the increase in distribution – by almost 50% – that has provided a nice boost to the fund in recent weeks:

Increase distribution (Noveen)

Now, on the surface, this sounds pretty convincing. In fairness, I see this as a positive and likely explains the strong performance of this position as mentioned in the opening paragraph. All things being equal, Muni CEF investors want to see high levels of income. Unlike taxable distributions, municipal mutual funds are expected to generate tax-free income, so the tax implications of receiving this cash are moot. So, while “high” dividends are not always beneficial in the investing world because they can trigger taxable events, that is not always the case here. So it’s a win for NAC in my view.

But this increase should also be taken with a pinch of salt for several reasons. First, NAC wasn’t the only fund to see a boost. Nuveen had a few dozen mutual funds in this latest round of raises, so investors have plenty of options to choose from (although there is only one other central mutual fund with a specific focus on California municipal bonds).

The second reason is that this boost may not be sustainable in the long term. In Nuveen’s announcement (linked above), the rationale for this increase is laid out in black and white. Suffice it to say, it is not because the underlying securities suddenly generate more income that can then be passed on to us as investors. Instead, the company is actively trying to narrow current price discounts to its net asset value and generate interest in these specific funds in the open market:

These distribution increases are intended to provide higher monthly or quarterly cash flows to shareholders, enhance shareholder returns, as well as help support secondary market trading in each fund share. For funds traded at a discount to NAV, distribution increases are intended to increase demand for each fund’s common shares, which may, over time, help narrow the discount between the market price of the fund and its underlying net asset value.

Source: Novin

My takeaway from this is that the income increase may be temporary and/or until Nuveen achieves its goal. For example, if NAC buying activity rises and the discount to NAV shrinks, Nuveen may say “mission accomplished” and restore the distribution back to its previous level – or at least a lower level than the current level. Likewise, if demand does not change in a meaningful way over time, Nuveen may determine that the boost is not achieving what was planned and that over-dividend is not sustainable. We will likely see a return of capital in this distribution (and others that were part of this programmed increase) and there will only be so long a fund can do that with CEF before it has a negative impact.

The bottom line is that I view this as a short-term tailwind, but readers should keep in mind Nuveen’s goal to support market trading for this fund. If this goal is achieved (or not), the distribution will likely be reset at a different level. We must take positions that are open to this reality.

The discount at par is very broad

The second reason for my “Buy” rating has to do with the attribute I mentioned in the previous paragraph. This is the fund’s valuation – which currently comes at a double-digit discount to NAV. In fact, at the time of writing, buyers could take positions in this ECB for approximately 11% less than the total value of the underlying bonds in the portfolio:

NAC – Quick statistics (Noveen)

This is a straightforward measure, so I won’t say much except that I view this very favorably. It supports why NAC is part of the income boost discussed above and shows that buyers still have plenty of time to get in. Simply put, the discount has not tightened yet, and while it may never completely tighten, this is a very attractive entry point. It protects against some downside and offers value in a broader market that lacks a lot of value (in my opinion). This supports the bullish case going forward.

Keep an eye on Golden State’s headlines

Of course, no investment comes without risk and no mutual fund comes with unique challenges. Although I believe a buy case in NAC is justified at these levels, my followers know that I am categorically not making any investments. there always Cons of any investment, should be included and discussed in any review. Although this doesn’t always happen elsewhere, I make a point of discussing headwinds and/or risks for any fund I cover – including funds I own and/or plan to buy.

With that in mind, what are some of the risks facing NAC? Well, since the fund focuses specifically on California Muni bonds, there is a significant amount of concentration risk. For state residents, this may make a lot of sense because the tax savings are a good reason to own this type of product. But for those who don’t reside in California, I would caution making sure this balances out a broader range of monies because you don’t need to just focus on one state that’s not your own. The tax benefits are limited to out-of-state people (you can save on federal taxes but likely not state taxes), so keep that in mind.

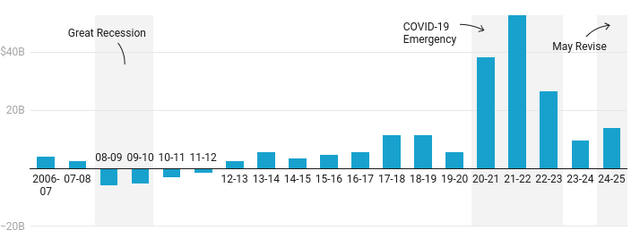

This is especially important given the challenges facing the “Golden State” at present. Many of these are budgetary in nature, as the country has gone from running a notorious surplus to now facing a severe deficit. This resulted in a sharp decline in California’s year-end reserve balance:

End of year balance (CA) (California Department of Finance)

With more than a quarter of the fund’s securities backed by either California GO bonds or other forms of taxes, this decline in the state’s finances is a worrying sign for funds like NAC:

NAC Properties Collapse (Noveen)

The conclusion I draw from this is that investors need to be careful about how budget talks progress and whether tough decisions are made. California used to be a “steady spiral” investment, but recent years have seen booms and busts in the state’s public finances making the sector more volatile. Is it still relatively safe? I would bet “yes” on this question. But is there more to monitor and focus on than before? The answer is also “yes” – meaning I urge my followers to be more active than passive when evaluating this arena.

Utility-backed bonds are an interesting play

Keeping the focus on NAC specifically, I would like to highlight the property distribution shown in the chart in the previous paragraph. As shown, NAC has approximately 18% of its core assets in the “Utilities” sector. This may seem strange, because most investors probably have exposure to utility companies through stocks – and perhaps not so much in municipal bonds. But this is actually a growing subsector of the muni market, and more state and local governments are turning to these issues to finance energy and utility projects. The premise is that the cost of the investments required is paid back over time by customers using the infrastructure or public services provided.

I actually like this exposure in the box for a number of reasons. The first is that it helps with diversification even within the Muni portfolio. Many CEF offerings do not contain much (or any) utility-backed bonds. So this is a good way to complement a wider collectibles collection. Moreover, many of these utility companies are public companies, and unlike for-profit utilities, these institutions often do not need regulatory approval to raise interest rates. This provides more flexibility when it comes to passing on costs to end users (businesses and households) – something bond investors want to see. Finally, expanding on the previous point, these can act as more of an inflation hedge than other bonds because of their variable rate feature. When input costs rise, they don’t have to wait until the next fiscal or calendar year to make their case for raising interest rates. If inflation proves to be a problem, municipal utility providers will raise rates faster to account for the inflationary trend. This is a huge benefit compared to other muni bonds – no matter which subsector you compare them to.

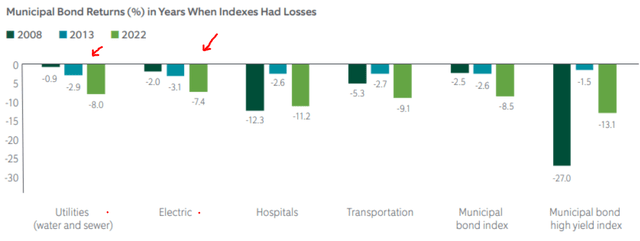

But don’t take my word for it. We can use history to guide us. During times of economic stress, including when the broader muni sector posts losses in the calendar year, this subsector often outperforms its peers:

Returns (by sector) in down years (Standard & Poor’s Global)

What I see here is a more stable sector that can also act as an inflation hedge. This should help explain why I view the NAC top sector favorably and provides support for why I rate this fund a ‘buy’.

Monies offer diversification

Another factor to consider is relevant to the NAC, but also to the muni sector more broadly. My followers know that I’ve been cautious with most bond exposure over the past year – and that’s true of leveraged mutual funds like NAC. In fairness, given that the yield curve has not normalized yet and “higher for longer” is the reality for the Fed, I wouldn’t be too aggressive here even with high-quality funds at discounts like this. Do I see a higher path – yes – but there are inflation/interest rate risks and readers should be aware of that.

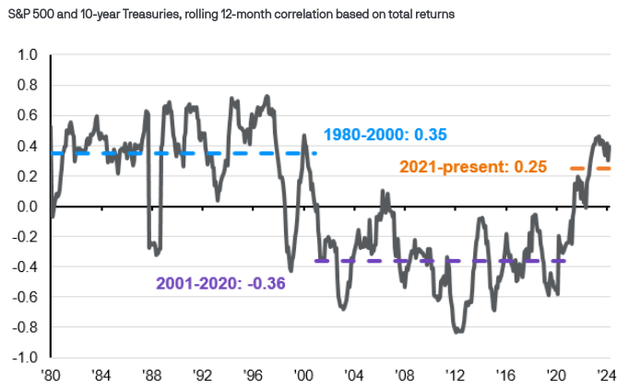

However, if I were to recommend exposure to fixed income, MONS is still the place to do so. The tax-exempt status naturally interests me, but I’m also troubled by the increasing correlation between stocks and Treasuries. This relationship was negative in the past, but it has become constantly more positive in the short term, which limits its usefulness in my opinion:

Stocks/Treasuries: Correlation over time (JP Morgan)

The bottom line for me is that Treasuries act less like a hedge than stocks than in years past, and this opens the door for investors to get more creative than the typical 60/40 (or similar) portfolio. Mons can fill this void, and while it is not a cure-all for the challenges facing the market going forward, I find it to be a more useful sector in comparison.

minimum

NAC has had a tough few years, but in the short term, it has a lot of momentum that I think can continue. There was a second increase in income for 2024 earlier this month, as the fund enjoys a significant discount to net asset value, and its underlying holdings provide diversification and protection from inflation. With these factors supporting the outlook, I feel comfortable with a ‘buy’ rating for the fund. As a result, I would encourage my followers to give the idea some consideration at this time.