Eoneren/E+ via Getty Images

Co-authored by Treading Softly

Passive investing in market-wide ETFs has been both a huge benefit and a huge disaster. Today, there is more than $7.1 trillion invested in various passive market ETFs. This has caused collectibles It has become, among various indicators, highly overvalued compared to its historical standards. This has also allowed millions of Americans to enjoy the benefits of a rising stock market. But the question that often arises is: Is value rising because companies are worth it, or simply because investors are blindly investing more money in passive market ETFs? Academics on both sides have argued for various reasons whether either or both are likely to be true.

I use my unique income method as a lens through which I view the market. I love getting passive income, but most passive market ETFs don’t provide passive income The income I am seeking. You’ll have to own them and then liquidate your shares to unlock any kind of usable return. Unrealized gains are not an actual return until they are realized. That’s why the tax man doesn’t go after them today because they could disappear as quickly as they appeared.

Today, I want to examine two funds that I use to generate significant income from various sectors of the overall market. These are diversified funds that will provide me with income for the rest of my life.

Let’s dive in!

Pick #1: PFFA – Yield 9.4%

If I were to run an exchange-traded fund focused on preferred securities, its composition and strategy would be similar Virtus InfraCap US Preferred Stock ETF (Pfffa).

I’ve been commenting on how attractive fixed income investments are in current market conditions. Preferred stocks are a great way to take advantage of the high returns and low prices in the fixed income space through investments that are likely to remain outstanding for a much longer period than debt investments. While structurally “equity,” preferred stock receives predetermined dividends that are not subject to the discretion of the board of directors like ordinary dividends. Dividends are a set amount, usually fixed, but can be floating. In most cases, the amount owed to the preferred shareholder must be paid in full before dividends are distributed to investors in the common stock.

The end result is an investment that pays a predictable amount like a bond but has a higher return because it carries some of the risks inherent in equity.

Pfa It is structured as an exchange-traded fund (ETF), which means there are mechanisms in place to ensure it trades close to net asset value, unlike some preferred CEFs (closed-end funds) that may routinely trade at a premium or discount.

In addition, the PFFA uses leverage to enhance returns by targeting leverage of 20-30%, depending on financial conditions. This is common for mutual funds, but rare in ETFs.

Finally, PFFA is Actively managed. Management tracks the portfolio daily and trades within the portfolio to maximize returns, which has been a very important contributor to its outperformance.

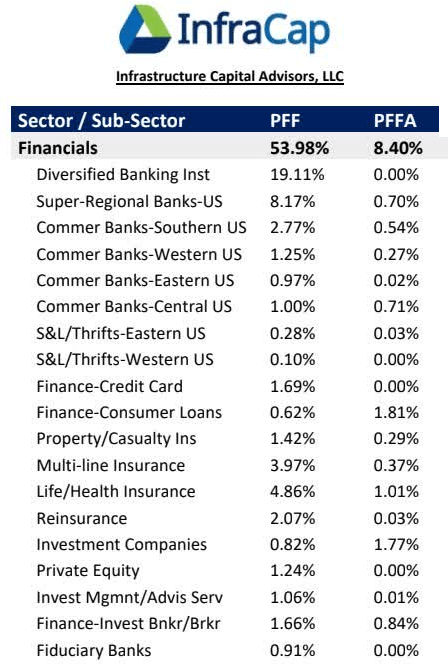

Do you remember when the bank panic happened last year, and bank stock prices were collapsing, and blue-chip stocks were not spared from fear? We noted that PFFA had low exposure to financial institutions and very little exposure to banks. Especially when compared to the iShares Preferred ETF and the Income Securities ETF (PFF). We wrote an article highlighting this:

Infracap

Fast forward a year and the share of the PFFA portfolio invested in “finances” has doubled: source

PFFA Fact Card

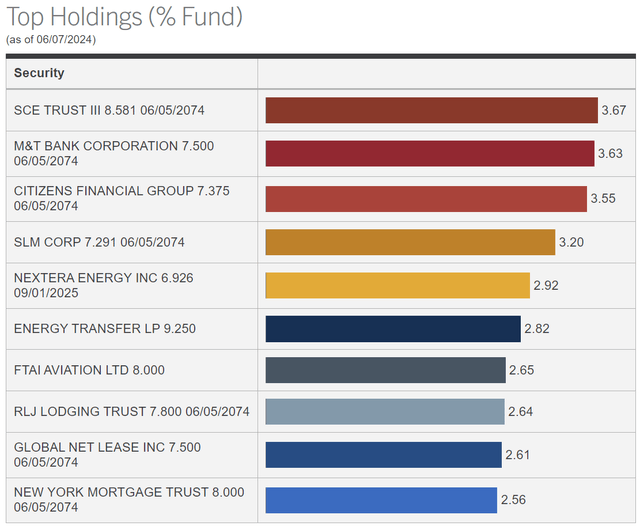

And when we look at the top ten PFFA holdings today, we see two banks. source

PFFA website

PFFA were not buyers of banks when rates were high, and this helped them avoid risk. He is a buyer when prices are lower.

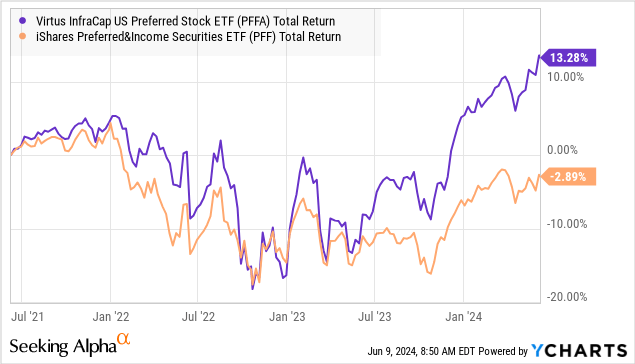

Thanks to this active management, PFFA has been able to significantly outperform PFF over the past three years.

PFFA pays $0.1675 per share in monthly dividends, a 9.4% yield at current prices. What makes this especially notable is the benefit of PFFA. As they say, “leverage cuts both ways.” In a bear market, all other things being equal, leveraged investing will underperform. However, through the preferred stock market decline, the PFFA outperformed. This is due to effective PFFA management. Management continues to do a great job during difficult times; We are keen to see what they can do in the good times.

Choice #2: Headquarters – 13.5% return

abrdn healthcare investors (HQH) is a CEF formerly known as Tekla Healthcare Investors. Aberdeen acquired Tekla with all its funds. Most importantly, Tekla’s money management remained unchanged. The skill of Tekla’s employees is one of the reasons Aberdeen bought the company, as it lacked experience in the healthcare sector.

The only thing Aberdeen changes is distribution. Headquarters It has a variable distribution policy where it pays out a portion of the net asset value every quarter. HQH was paying 2% each quarter when Aberdeen acquired the fund. It has increased this amount twice and now pays 3% of NAV every quarter. In the press release, Aberdeen said it expects to maintain this higher level of dividends for at least a year “unless there is a significant and unexpected change in market conditions.”

The press release continues to indicate its bullish outlook for the sector in the medium to long term to support increased distribution.

“After a long period of weak returns in this sector, merger and acquisition activity has picked up, clinical trial successes have been achieved, and select new products have been approved. The tremendous success and impact of the recently approved GLP-1 product portfolio on obesity and diabetes is an indication of the prospects and potential impact of the pharmaceutical sectors.” and biotechnology on human health and well-being. Furthermore, it appears to us that the macroeconomic environment is improving directly, which has had a negative impact on growth-related sectors. Biotechnology appears to have peaked followed by the prospect of potential interest rate cuts which we expect to provide a tailwind. For the sector, funds are poised to benefit from these trends.

He also notes that a higher payout ratio may help the fund trade at a lower discount to its net asset value.

We’ve previously discussed how the distribution policies of mutual funds like HQH do not materially impact a fund’s total return over the long term. The reason is that any distributions are subtracted from the net asset value. If the distributions are higher than the total return produced by the portfolio, the NAV will decline. If the distributions are less than the total return, the net asset value will increase. The end result is that long-term shareholder return will be a combination of the distributions received and the change in net asset value. Since HQH’s policy is variable, distributions will rise or fall in line with changes in net asset value.

However, where the distribution policy can have an impact on the premium/discount to the net asset value at which the fund trades. Many investors are attracted to a higher distribution, and if a fund is trading at a discount to NAV, a higher distribution can assure shareholders that they will be able to extract their value.

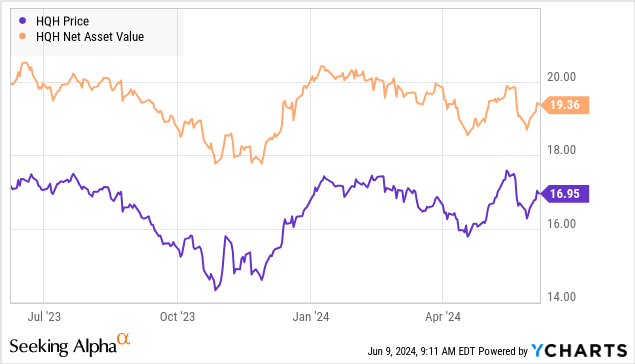

HQH has been priced well below NAV over the past year and is currently at a 12% discount to NAV:

What happens if NAV increases by $1 to $20.36? With HQH’s old distribution, it would pay $0.41, leaving $19.95 in NAV. At a 12% discount to NAV, the stock price would trade at around $17.56. So the NAV increased by $1.00, but the shareholder saw a total return of $1.02 ($0.41 dividend + $0.61 increase in price)

Under the new policy, if NAV rises to $20.36 in the next quarter, HQH will pay a $0.61 dividend, leaving $19.75 in NAV. The price would be around $17.38 assuming the same 12% discount to NAV. So, the shareholder gets $0.61 in cash and a $0.43 increase in price for a total return of $1.04. In both cases, the NAV increased by exactly $1.00, but shareholders had a higher total return through the higher distribution.

The reason for this difference is that when the price is at a discount to NAV, any changes to NAV as it clears will be discounted to the stock price. If shares trade at a premium to NAV, the opposite is true, as any increase or decrease in NAV per share is magnified in the share price if the premium remains the same.

Of course, premiums and discounts can change, and Aberdeen will likely hope that a change in distribution policy will reduce or even eliminate the discount to NAV at which the headquarters trades.

We agree with the long-term outlook for the healthcare sector. Health care has underperformed in recent years due to a variety of issues including rising interest rates, rising inflation, regulatory uncertainty and some natural rotation as the coronavirus-era boom slows.

Essentially, long-term demand for healthcare is very strong and will continue to rise.

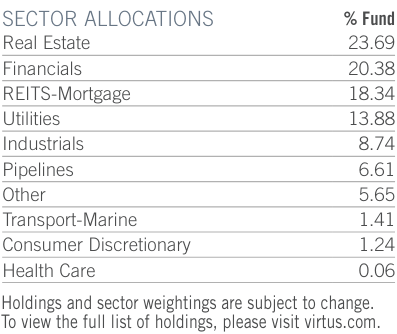

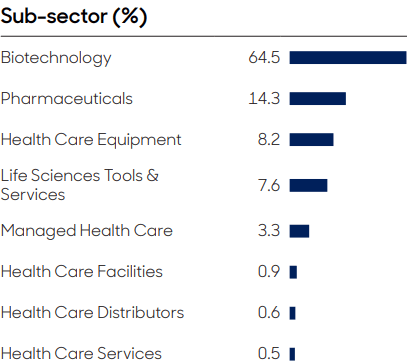

HQH mainly invests in biotechnology and pharmaceuticals. source

High Quality Headquarters Fact Sheet

The market has given us the gift of being able to buy HQH at a discount to NAV. The fact that HQ now pays a higher distribution helps ensure that we get our total return, even if market sentiment toward HQ remains negative.

As income investors, we want to own companies that produce things people use every day, and healthcare is something most of us use and prioritize regularly. The market allows us to purchase the headquarters at a significant discount, and Aberdeen increases the amount we charge, lining our pockets with cash!

Conclusion

By leveraging skilled managers at both headquarters and PFFA, I am able to generate generous amounts of income on a regular basis from market sectors capable of providing this income for decades to come. When a house is built, it is not built with the expectation that it will last 12 months before it collapses or collapses. A home is built with the expectation that it will be lived in and used for decades and decades. The average holding period for an investor has decreased from roughly a decade ago to being able to be measured in months and sometimes weeks. This rapid decline in an individual’s ability to hold something as a long-term investment has led many to build a portfolio as if they were building a shoddy house, with the expectation that their possessions will not remain in place even for a year.

When I build a portfolio designed to pay for my retirement, I don’t want to have to rebuild it every 12 months. I want a portfolio that will stay with me throughout my retirement, and provide me with regular income. I do this by holding at least 42 different high-quality investments, reinvesting 25% of the income I receive into my portfolio to keep my income stream growing, and enjoying my life to the fullest in the meantime.

That’s the beauty of my income method. That’s the beauty of income investing.