Mihailomilovanovic

Maybe I’m weird, but I’ve always liked interesting companies with interesting business models. The more bizarre the work, the more fans I have. So, you can imagine how excited I was when I first stumbled upon this in December 2022 Bolero (New York Stock Exchange: Pot), a publicly traded company that operates traditional bowling centers and other entertainment concepts. Examples of this include facilities with lounge seating, arcades, enhanced food and beverage offerings, and more.

In my last article on the company, published in June 2023, I ended up rating it a ‘Buy’. I have been impressed by the strong store sales growth and continued physical expansion of the company. The company’s shares were also attractively priced at the time. This led me to point out that there could be an attractive upside on the table. But since then things have not gone according to plan. Shares have actually seen A decrease of 6.5%. This compares to the 25.3% increase the S&P 500 saw over the same time period. You might think, given this weakness, that the company’s fundamental position was getting worse. If we limit the results to 2023, that would be false. But results for 2024 have been mixed so far. Despite this, the shares look attractively priced, and the company appears to offer enough upside to justify the “buy” rating I assigned it previously.

Not bad, but could be better

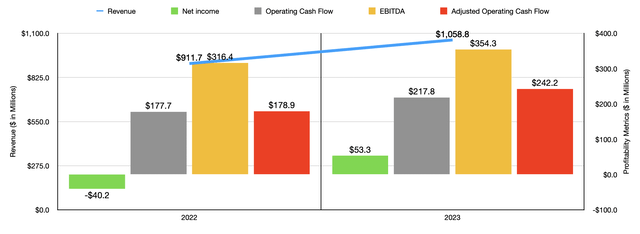

Basically, things are mixed up with the Bolero. In 2023, the company’s revenue finally surpassed $1 billion, bringing its total revenue to $1.06 billion. This represents an increase of 16.1% compared to the $911.7 million achieved one year earlier. This increase was driven in part by a rise in the number of operating locations from 317 to 328. The company also benefited from a 12% increase in same-store revenue. This increase is due to the strong demand for the company’s services. In addition, the company also benefited from a 51% increase in media-related revenue, as well as new and closed sites, and most of that was related to the addition of the sites you mentioned.

Author – SEC EDGAR data

As revenues rose, the company’s bottom line improved dramatically. The company went from a loss of $40.2 million in 2022 to a profit of $53.3 million last year. Although the company’s gross margin shrank, selling, general and administrative costs decreased by $42.8 million. This was mostly thanks to transaction costs of $68.4 million during fiscal 2022 that were not repeated in 2023. The company also benefited from an income tax benefit of $84.2 million that exceeded the benefit of $0.7 million reported one year earlier. Otherwise, profits in 2023 would also have been negative. Other profitability metrics followed a similar path. Operating cash flow increased from $177.7 million to $217.8 million. If we adjust for changes in working capital, we would see an increase from $178.9 million to $242.2 million. Finally, the organization’s EBITDA increased from $316.4 million to $354.3 million.

Author – SEC EDGAR data

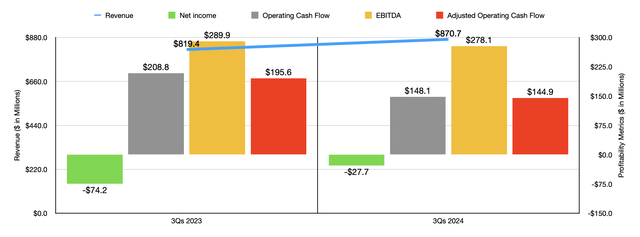

Unfortunately, the company’s strong performance didn’t continue into fiscal 2024. The big exception to this was revenue, which grew from $819.4 million in the first three quarters of 2023 to $870.7 million at the same time this year. But the bottom line took a hit during this time. Part of this is due to the company’s gross profit margin shrinking from 34.8% to 28.3%. This decline was actually due to the rise in the number of sites which caused various costs to increase to the tune of $88 million on an annual basis. There were other pain points as well. For example, net interest expense jumped from $80.1 million to $130.6 million. High interest rates, as well as increasing debt, were to blame. Other profitability metrics also worsened during this time. Operating cash flow decreased from $208.8 million to $148.1 million. On an adjusted basis, it decreased from $195.6 million to $144.9 million. Finally, the company’s EBITDA contracted from $289.9 million to $278.1 million.

Bolero

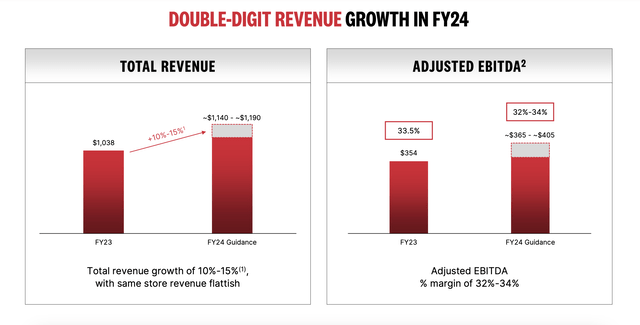

Despite these difficult points, the administration appears optimistic. Excluding service fee revenue, the company expects revenue this year to grow to between $1.14 billion and $1.19 billion. They also believe EBITDA will be between $365 million and $405 million. At the midpoint, that would be 8.7% higher than what the company achieved in 2023. However, in the company’s third-quarter earnings release, it stated that investors should expect these results to be near the lower end of the range. So, for the purposes of this article, I’ll be using EBITDA of $365 million. That should translate to adjusted operating cash flow of about $249.5 million. This growth should be driven in part by the significant investments being made. Management expects acquisitions worth $190 million. This is higher than the $160 million originally planned for this year. This is in addition to $40 million allocated for new construction facilities and $80 million spent on conversions and other growth initiatives. The latter represents an increase from the $75 million initially planned for 2024. Furthermore, the company also intends to spend $45 million on maintaining current operations.

Author – SEC EDGAR data

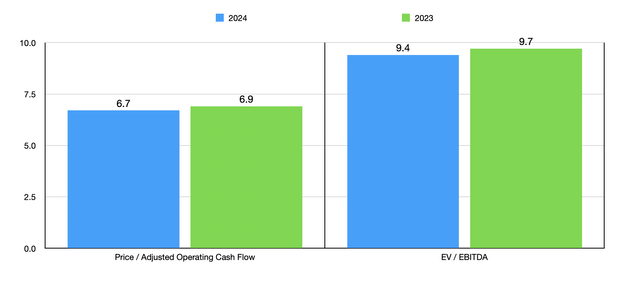

Assuming this pays off, shares look very cheap, both on an absolute basis and relative to similar companies. In the chart above, you can see how the stock is priced using historical results for 2023 and estimates for 2024. I then compared the company to five companies it has similarities to as shown in the table below. On a price-to-operating cash flow basis, only one of the five companies was cheaper than Bowlero. This rises to just two out of five when using the EV to EBITDA approach.

| a company | Price/operating cash flow | Value added/EBITDA |

| Bolero | 6.9 | 9.7 |

| Rice Fair (FUN) | 6.0 | 8.8 |

| Six Flags Entertainment (SIX) | 7.6 | 12.6 |

| Topgolf Callaway (MODG) Brands | 8.7 | 10.6 |

| XPOF Fitness (XPOF) | 13.3 | 9.0 |

| Vail Resorts (MTN) | 12.6 | 12.8 |

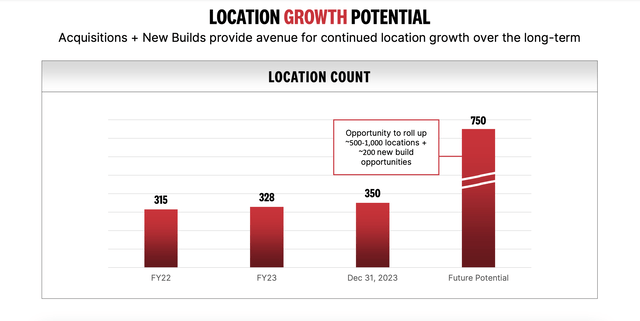

As value investors, we must also focus on long-term growth, not just short-term growth. The good news is that management is very transparent about its goals. For starters, the company is converting more than 150 of its sites to a more upscale format. This is expensive but the end result is a 25% increase, on average, in total returns. Management is also looking at other opportunities. For example, they believe there are about 200 new construction opportunities in the market as the company expands from about 350 operational sites at the end of last year to an eventual goal of about 750 sites. They said that number could grow to as many as 1,000 sites, and that’s excluding 200 new construction opportunities.

Bolero

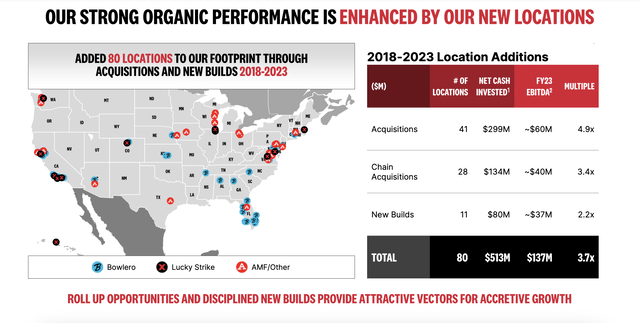

Of course, this doesn’t come cheap. From 2018 through 2023, for example, the company acquired 41 different locations for $299 million. This was in addition to the chain’s 28 acquisitions worth $134 million and 11 new builds worth $80 million. In total, the cost to shareholders was $513 million. But the great thing is that the total effective EV to EBITDA multiple for these investments was about 3.7. This is significantly less than what the company as a whole is trading at during this time.

Bolero

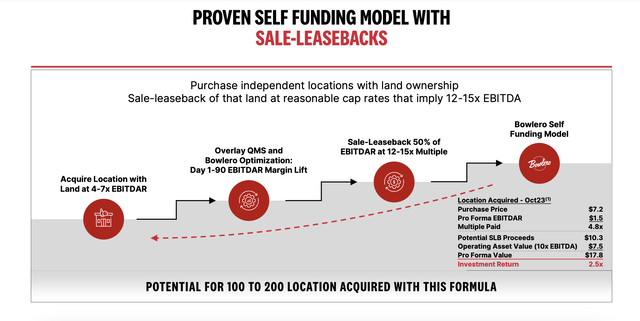

As the company expands, it looks for other ways to create shareholder value. I have already tried sale and leaseback transactions in the past. In the image below, you can see exactly how this specific scenario has played out in the past. Management believes that approximately 100 to 200 sites could eventually follow this specific formula, with the potential for huge investment returns.

Bolero

He stays away

Given the bottom-line financial performance so far this year, Bowlero shares have seen some weakness. However, investors should focus on the long term. Even if financial performance doesn’t improve much from here and just matches management’s expectations, the stock looks very cheap, both on an absolute basis and compared to companies that have some similarities to it. For this reason, I see no reason to be bullish on the company in the long term. For this reason, I have decided to keep the company with a “buy” rating for the time being.