Watchiwit

Opera stock suffered a bear market

opera ltd.Nasdaq: Opera) Investors have endured a tough couple of months since buying momentum for OPRA stock peaked and stalled in March 2024, near the $17.5 level. Since my last rise Update on Opera In March, the OPRA index fell nearly 30% during its recent lows in May, underperforming the S&P 500 (SPX) (spy). I’ve confirmed my belief as to why Opera can continue to monetize higher-value users as it expands into Western markets and among gaming-focused users. Although OPRA’s performance was poor, my Opera implementation remained consistent. Furthermore, I assess strong buy sentiment above the $12.5 level, which should be defended firmly until OPRA resumes its thesis for a continuation of the uptrend.

Opera’s first-quarter earnings release in late April was strong as the leading browser company beat Wall Street’s estimates for Opera. However, its relatively cautious guidance has likely disappointed the market, suggesting that Opera is going through a growth normalization phase. In addition to, Opera increased CapEx To invest in “a new AI data center represents an extraordinary amount of CapEx.” Consequently, it burned through a significant level of operating cash flow, resulting in free cash flow of $8 million, indicating an EBITDA conversion of 33%. However, Opera management highlighted that “significant lead time is needed for any expansion of CapEx investments.” As a result, investors concerned about continued incremental capital expenditures that were not anticipated in Opera’s future guidance should be reassured.

Despite Opera’s near-term cash flow impact, I believe Opera is investing to solidify its advantage as a leading AI browser. Opera has strengthened its value proposition in generative AI, launching a home-grown LLM course on its AI browser. As a result, Opera has integrated LLMs into its flagship browser, Opera One, “enabling users to run these models natively on their devices.”

Opportunities for opera’s growth are still emerging

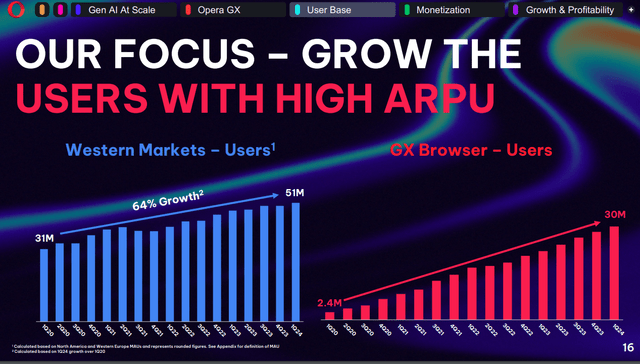

Growth of Opera users (opera files)

ARPU also continued to improve as Opera expanded monetization from the Western market. Accordingly, Opera’s Western market user base has risen to 51 million, representing 64% growth over the past four years. Gaming-focused browser Opera (GX Browser) saw its user base rise to 30 million in the first quarter. While monetization opportunities on its GX browser are still early, Opera estimates a massive TAM of 0.4 billion users (excluding China).

Furthermore, the EU Digital Markets Act has opened up another growth vector for monetizing the potentially lucrative iOS base. The DMA requires that Apple display the browser option associated with iOS results in the region. Opera highlighted that it saw “a 63% increase in new iOS users in the EU from February to March following implementation.”

Therefore, further regulatory action in the US could weaken Apple’s walled garden and possibly benefit Opera, given its increasing focus on the Western market. Hence, it should bolster its existing efforts in the Android space as Opera continues to expand its AI browser’s user base for gaming and non-gaming users.

OPRA’s assessment remains lenient

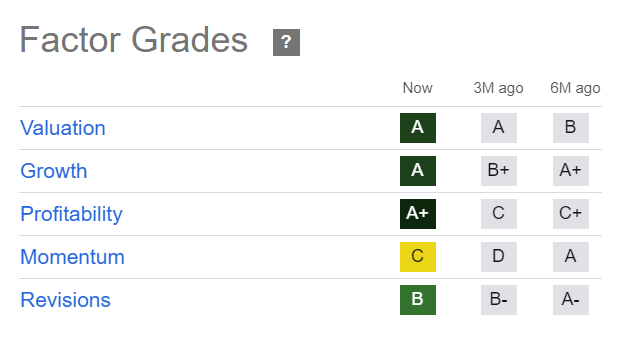

Opera Quantitative Degrees (Searching for Alpha)

The bifurcation of the OPRA rating (“A rating grade”) compared to the “A” growth grade highlights the potential opportunity for a rating re-rating if market sentiment improves. In other words, OPRA is assessed as undervalued relative to its best-in-class growth potential. OPRA’s forward adjusted P/E of 17.59 is more than 40% below its sector average, which supports my assessment. Along with earning a strong profitability grade of “A+,” OPRA has demonstrated its ability to justify a sustainable business model.

Opera’s fiscal 2024 guidance of $459.5 million at the midpoint is in line with Wall Street consensus estimates of $459.8 million (up 15.9%). However, it also represents a deceleration in growth compared to reported FY23 revenue of $396.8 million (up 19.9%). As a result, I assessed management’s need to reassure the market of its capital investments, even with adjusted EBITDA forecasts of between $22 million and $25 million.

Despite this, Opera is still considered a fundamentally strong company and has been given a profitability grade of ‘A+’. The recent extension of Opera’s “search agreement through 2025 on current terms” with Google (GOOGL) (GOOG) should mitigate near-term risks to its earnings outlook. Opera confirms its collaboration with Google, as the search leader “recognizes the shared potential” between Opera and Google.

As we think about Opera’s bullish thesis, it’s also important to keep in mind that Opera’s focus is on risk as a browser company. This is mainly based on advertising (58%) and search revenue (42%). Therefore, a deep cyclical downturn in the advertising market could impact its future guidance significantly and lead to a lower valuation. Additionally, concerns about the ongoing search partnership between Opera and Google could hold some investors back as they reevaluate potential changes in terms that could reduce Opera’s monetization potential.

Is OPRA stock a buy, sell or hold?

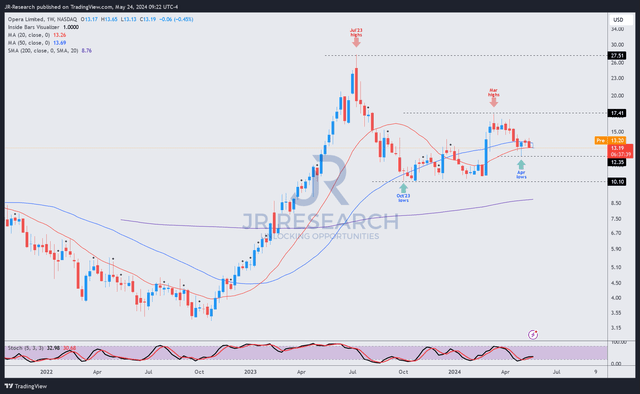

OPRA Price Chart (Weekly, Average Range, Dividend Adjusted) (trading offer)

OPRA price chart is indicating a consolidation area above the $12.5 level for the past four weeks. Staying above this level is crucial to achieve a higher low price movement compared to the consolidation zone of OPRA from October 2023 to January 2024 ($10 level).

Given OPRA’s strong fundamental metrics and cheap valuation (relative to sector peers), OPRA buyers could come back more strongly. Opera remains well positioned to capitalize on its potential in the market as it improves its monetization opportunities.

Therefore, investors who have been unable to add exposure should consider leveraging current levels to buy more shares before OPRA revisits its March 2024 highs.

Rating: Keep buying.

IMPORTANT NOTE: Investors are reminded to conduct due diligence and not to rely on the information provided as financial advice. Consider this article to complement your required research. Please always apply independent thinking. Note that the classification is not intended to specify a specific entry/exit time at the time of writing unless otherwise stated.

I want to hear from you

Do you have a constructive comment to improve our thesis? Spotted a critical gap in our view? Did you see something important that we didn’t do? agree or disagree? Comment below to help everyone in the community learn better!