Trench coats

Nothing has caused more problems than the progress or lack thereof of both EBITDA (since the acquisition) and its place in Warner Bros Discovery’s upcoming growth (Nasdaq:WBD) since the last article. management since then I did a bunch of presentations to try to ease the transition from “cutting like crazy” because the acquisition literally had no cash flow (or certainly nothing close to enough) to grow the business. Mr. Market is upset that growth has not occurred from the beginning, while he is concerned that the lack of growth will impact EBITDA and cash flows. Put Mr. Market in a position of being less than satisfied with the whole situation. But you should also realize that if management follows through with the plan, and everything goes right instead of wrong, Mr. Market may become a fan of his own.

Stock price history

All this confusion has of course affected the stock price.

Discover Warner Bros. History of common stock prices and key valuation procedures (Search for Alpha website June 10, 2024) Discover Warner Bros. Common Stock Price History and Key Valuation Measures (See Alpha as of May 31, 2024)

Not to mention, board member John Malone gave an interview in which he stated that this would take some time to be resolved because things were worse than management expected. He also noted that he sold shows to support the administration.

Mr. Market was clearly disappointed from the beginning (as shown above). Sometimes, a large acquisition is like building a house except for the fact that you receive a value report from the market every day. This value report can lead you astray regarding the progress that management is making. This has led to management doing the latest ‘promotions’.

It offers EBITDA and free cash flow

The last article mentioned management’s frustration with the market’s impatience to rebuild the company in a way that improves profitability and leads to growth.

The market responded by shifting the conversation to revenue and EBITDA growth.

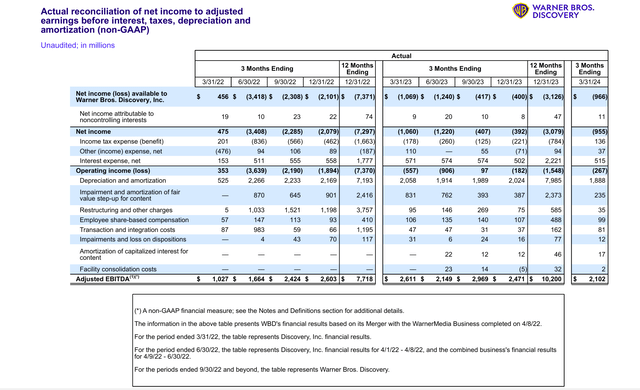

Warner Bros Discovery’s EBITDA progress was revised (Warner Bros Discovery Q1 2024, Earnings Supplemental Calculations)

Note that EBITDA definitely grew year over year. But there was some concern that the quarterly comparison turned negative starting in the fourth quarter.

This is a company whose profits will be greatly influenced by the results of movies (or games, for example). Last year there was a very successful game that was not repeated in the first fiscal quarter. Before that there was the double whammy (among other issues). So, the quarterly comparisons could certainly fluctuate wildly, and wouldn’t really mean much.

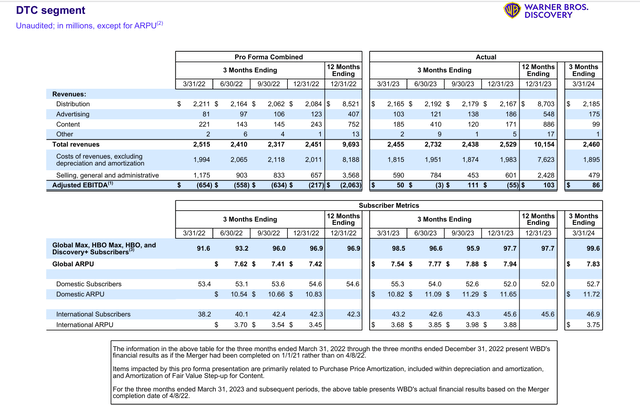

One thing that impacted EBITDA in the previous fiscal year was that DTC went from losing billions to almost breaking even (as covered throughout the year in previous articles).

Warner Bros. Discovery DTC trend results (Warner Bros Discovery Q1 2024, Earnings Supplemental Calculations)

One thing to remember about this is that the improvement in DTC shown above came a year ahead of schedule. Comparisons can be consistent or slightly different in both cases because the growth plan is on schedule. But it has now been presented in a recent conference presentation.

Now the market is pretending to be tired of hearing “the same old thing” when the real reason is that there has been no significant improvement compared to the previous financial year. However, the absence of those significant losses was a factor in the debt being repaid far ahead of schedule.

Management will likely raise some targets where possible when something like this happens. But anticipating the “full next step,” which will likely be a growth strategy a year ahead of schedule because the financial improvement occurred early, is probably unreasonable. Instead, it is reasonable to expect some stable results until the next step is implemented as planned.

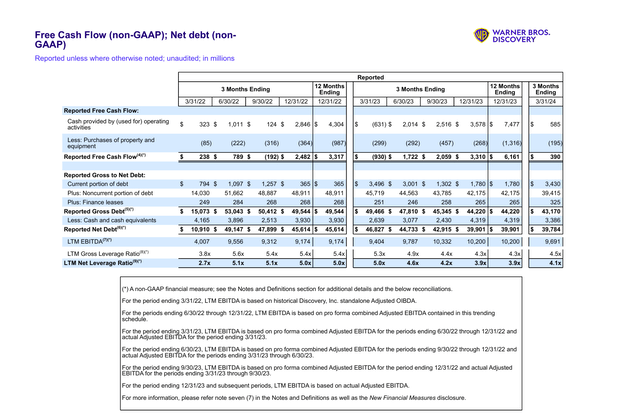

Free cash flow

It’s also important to note that “you can’t spend EBITDA.” Therefore, progress in EBITDA should be compared with cash flow and progress in free cash flow. So, you, the investor, have to decide whether you agree with how the GAAP number is spent and whether you agree with counting non-GAAP free cash flow as a spendable number.

Discover Warner Bros. free cash flow and related trends (Warner Bros Discovery Q1 2024, Earnings Supplemental Calculations)

Since the first quarter of fiscal 2023, the free cash flow comparison with the previous quarter has improved. For an acquisition of the size of the one made here, this is a huge improvement in a period of time that few departments can match. This funded an unexpectedly aggressive debt reduction plan that gave the company significant financial flexibility earlier than some of us expected.

Note especially that the first quarter showed a cash flow improvement of more than $1 billion compared to the previous fiscal year. Much of it focused on EBITDA. But the cash flow improvement shown above is spendable while EBITDA is not.

Also note that the company has paid down nearly $10 billion in long-term debt since the acquisition in 2022. Since the end of the quarter, management has called in more debt. That led to a comment on the latest conference call about paying down the roughly $13 billion in debt since the acquisition.

Reduction strategy

Perhaps the single most important goal is to generate cash to reduce debt. Management stated in numerous conference calls and presentations that cash was not significant prior to the acquisition. As a result, they find out which items need to be invoiced as well as what else needs to be collected. This has likewise helped in the debt reduction process.

Mr. Market may not care about this because it is a “one-time” or “non-recurring” item. However, paying down debt gives management a lot of flexibility. It was mentioned in the last presentation that management would consider acquisitions. A leverage ratio of less than 4 would likely give management the option to do so. Management’s debt ratio will likely be below four with the next quarterly report.

Once this happens, other business strategies will increase in importance.

Business strategy

The last conference focused on the idea that management will now work to grow the business. It’s been talked about ever since the acquisition took place.

Overriding the problem was the lack of cash flow for the acquired assets. That had to be fixed first. Therefore, management redirected its efforts towards profitability through cost control and proper accounting. Obviously, systems had to be put in place first to make this happen. This has led to management becoming frustrated with the market more than once.

But what is emerging now is the market attitude that the company has not grown and therefore cannot grow. However, it is very essential to have the right strategies in place with support systems before profitable growth can be achieved.

To this end, there was discussion at the conference about clustering as this company has long been at the forefront of discussing this concept. It also took some time to come up with a rational growth strategy after the support systems came into being. With a large company, this takes longer than the market has been patient with.

Now management laid out these growth plans during a conference presentation. To some extent, these plans were also discussed in conference calls and other presentations. What’s different is that after two long years of waiting, some of these plans have been released.

Mr. Market was yawning as if it was too late. But entertainment is a very fragmented market with no one really controlling a significant portion of the market. Therefore, a good product is needed, otherwise growth will fail. It also means that there may not be uniformity due to the fragmented nature of the market. This could change as the live streaming market progresses. Basically, anyone with a competitive product can “join” anytime now. Barriers to entry are low to nonexistent in some cases. As a result, the consumer has a lot of choices.

Despite the market reaction, there is a good chance that the company now has the financial flexibility to adjust its strategy once that strategy is launched. Money can do miracles. The fact that the debt is paid off so early gives management the flexibility to implement upcoming growth strategies that are often not available in leveraged buyouts.

To the extent that these strategies will lead the company to greater profitability as the effects of the initial deleveraging effort (and building support structures) wear off, this may vary. Most likely it will surprise the market.

The market has been bored to death by now with the initial steps. But if these steps are done correctly, the market will likely love what comes next.

Sports

The market has been interested in NBA contract negotiations for some time. But management noted that sports coverage (or delivery) had been a global organization for some time. Therefore, the loss of any tangible major item, such as an NBA contract, is unlikely to be a long-term problem.

The French Open Tennis Championships have just been announced. This is exactly the type of advertising that could lead to the necessary rebuilding (or loss replacement) of sports coverage in the event of an NBA contract being lost. It will of course take many of these things because an NBA contract is much more important. But as a global company, there are many things that can ultimately make up for the loss of an NBA contract.

Of course, this loss did not occur despite market concerns. But the presence of a global organization is another benefit that may help during negotiations. There can be economies of scale that competitors do not enjoy, in addition to other benefits.

summary

The initial steps of the acquisition were a painful process with many negative consequences that caught Mr. Market’s attention. This has Mr. Market concerned about the progress of free cash flow because he believes the company will not grow (mostly because it has not).

But the growth of the remaining companies is difficult to measure because a lot of non-essential “functions” have been eliminated. This led to shrinkage by removing non-core and unprofitable parts of the company while improving the core processes that represent the future of the company. This type of progress is not currently witnessed in the market and cannot be measured with certainty, while the losses and mistakes seemed very real.

This is a solid buy based on the idea that management has done what it was meant to, and it’s done to properly support the upcoming growth that the market will love a lot. What gets lost in all this worry is the greatly improved debt ratio at a completely unexpected rate.

While the market is clearly skeptical of many of the recent management conference presentations, the market will remember what was said if management performs according to the set of guidelines. This could cause the stock price to rise significantly later.

Risks

Newer strategies, such as MAX release and bundling, may fail or encounter unexpected problems. They may also fail to meet management’s expectations. As the CEO and others have indicated, they intend to continue working with new ideas until satisfactory returns are obtained. This may also take longer than the market has patience. It is possible, but unlikely that it will never happen, and the stock price never recovers or exceeds the price it was before the takeover.

The potential lack of success in renewing the commercial relationship with the NBA also affects the future of the stock price. There can be no assurance that a loss on a contract can be made up for by sufficient business elsewhere.

The films are currently running ahead of expectations. There is absolutely no guarantee that this will result in a good year or a good year (or years) to come. Likewise, there’s a risk that games will never have another “hit” game.

Management claims to have found physical “skeletons in the closet” that need some major action. There is no guarantee that another physical discovery will not occur in the future.

The loss of key employees can materially derail a company’s plans.