Diluc Klaisataporn/iStock via Getty Images

At the beginning of 2024, all the world’s major central banks were on the same page.

Inflation, which rose to a 40-year high in 2022, fell in 2023 and was expected to approach the joint central bank. Target rate 2% this year The world’s major central banks have been looking to ease monetary policy, with the exception of the Bank of Japan, which has already been easy going, having maintained a negative interest rate policy for the previous eight years and still implementing quantitative easing (“QE”).

But as 2024 progressed, the improvement in inflation was uneven, and the world’s major central banks differed in implementing monetary policies to achieve their goals.

Bank of Canada

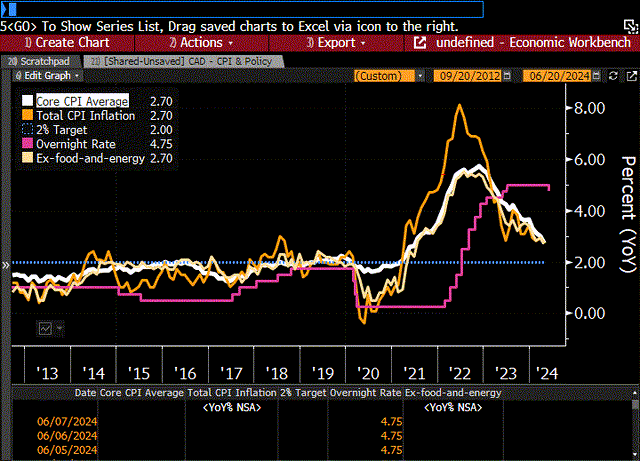

Last week, the Bank of Canada (“BOC”) became the first G7 central bank to cut its overnight interest rate. After remaining stable at 5.0% since July 2023, the Bank of Canada decided Reducing the interest rate by 25 basis points to 4.75%. This was the first interest rate cut in 4 years.

The CPI peaked at 8.1% in July 2022, triggering a series of 10 interest rate increases, raising the overnight rate to 5.0%. These tough measures had an impact, causing the consumer price index to gradually decline. Since the start of 2024, the CPI has fallen below 3%, falling to 2.7% in April. This is the lowest CPI level in three years.

Bloomberg

Bank of Canada Governor Tiff Macklem said when announcing the interest rate cut:

“If inflation continues to decline, and our confidence remains that inflation is sustainably heading towards the 2% target, it is reasonable to expect further interest rate cuts.”

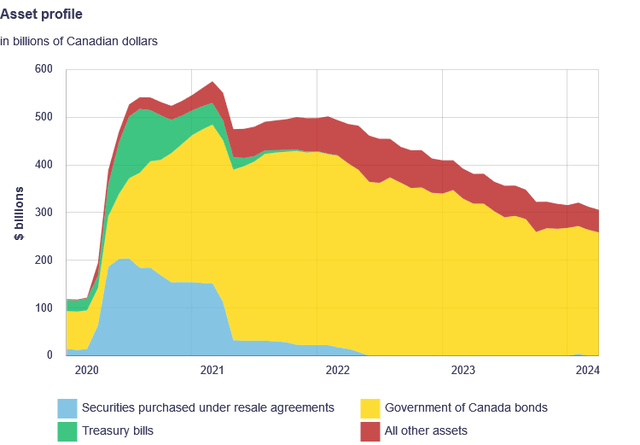

The Bank of Canada also continued its balance sheet reduction program, more commonly known as quantitative tightening (“QT”). Since peaking at C$576.3 billion in Q1 2021, it has managed to shrink its balance sheet by 50% to C$283.9 billion, its lowest level in 4 years, since just before the pandemic.

Bank of Canada

European Central Bank

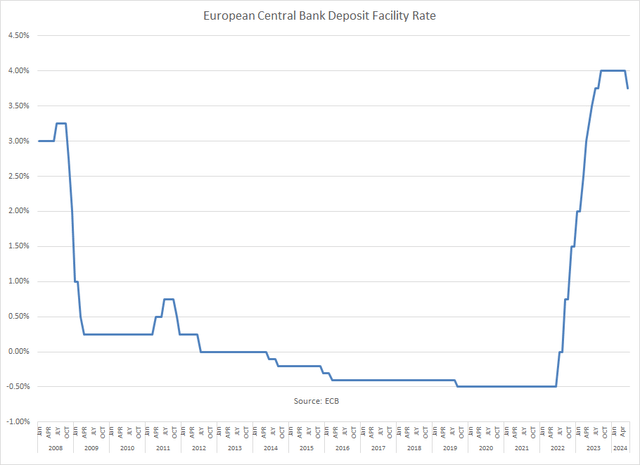

Following Canada, the European Central Bank also cut its deposit rate by 25 basis points last week, to 3.75%.

The European Central Bank represents three additional G7 countries, namely Germany, France and Italy, in addition to 24 other European countries.

The deposit interest rate has stabilized at 4.00%, the highest level in the ECB’s history, since September 2023. This represents the first interest rate cut by the ECB since 2019. It is also the first time the ECB has moved interest rates before… Federal Reserve Bank.

European Central Bank

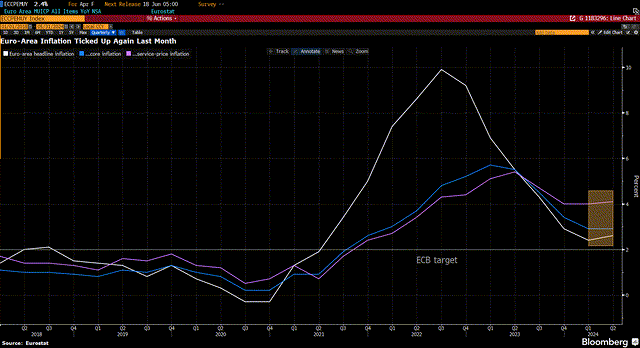

European Central Bank President Christine Lagarde strongly hinted at a rate cut in April, when the euro zone consumer price index recorded a second consecutive reading of 2.4%. This showed the significant progress that has been made on inflation due to the 10-fold hike in interest rates, after headline inflation peaked at 10.6% in the third quarter of 2022.

Bloomberg

However, the rate cut was an embarrassment, as it came with some surprises. First, just before the ECB meeting, the just-released headline inflation rate for May jumped to 2.6%. Then, along with the interest rate cut announcement, the Governing Council said:

“Despite the progress made over recent quarters, domestic price pressures remain strong with wage growth rising, and inflation is likely to remain above target until next year. The latest Eurosystem staff forecasts for both headline and core inflation for 2024 and 2025 have been revised compared With March forecasts, staff now expect headline inflation to average 2.5% in 2024, 2.2% in 2025, and 1.9% in 2026. For inflation excluding energy and food, staff expect inflation to average 2.8. % in 2024, 2.2% in 2025, and 2.0% in 2026.

“Data-driven decisions must be data-based decisions,” said ECB policymaker Robert Holzmann, who was the only Governing Council dissenter from cutting interest rates.

The rise in inflation, coupled with increases in the European Central Bank’s inflation forecasts over the next two years, gives pause to the timing of future interest rate cuts.

As Christine Lagarde said: “We have made the right decision, but that does not mean that interest rates are on a linear downward path.”

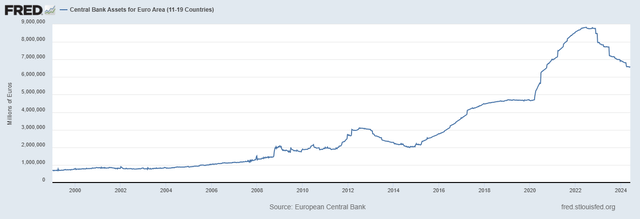

The ECB also reduced its balance sheet through QT. After peaking at €8.84 trillion in the second quarter of 2022, the ECB cut its balance sheet by 25.8% to €6.56 trillion. This represents the lowest level since the third quarter of 2022, and also represents a 55% reversion to pandemic-related quantitative easing.

unique

Federal Reserve

The Fed has been on a slightly different path this year.

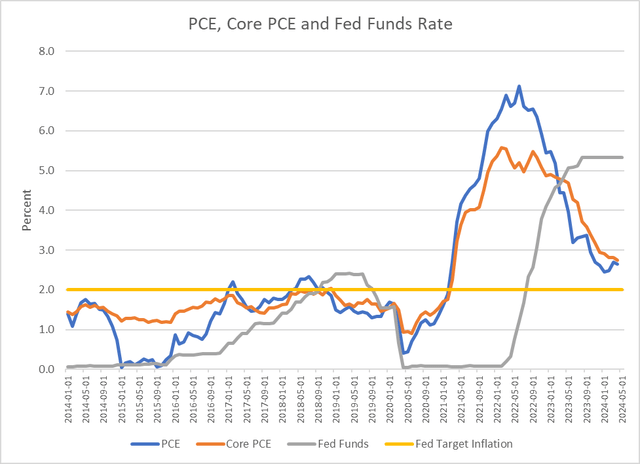

In December 2023, Fed Chairman Powell stated that the Fed’s summary of economic outlook was looking for inflation to continue its downward movement, and that the Fed would cut interest rates in three steps for a total of 75 basis points in 2024. However, the year progressed And there was no significant improvement. The headline PCE rate is 2.7% and the core PCE rate is 2.8%.

unique

The balance of inflation-related risks remains tilted to the upside. Many economists expect little movement toward the Fed’s 2% target over the remainder of the year, partly due to the comparison with lower inflation numbers from the second half of 2023.

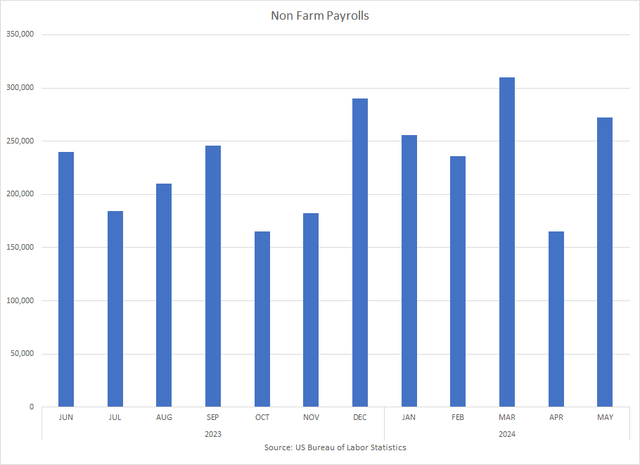

In addition, the labor market remained flexible. The US economy added 272,000 jobs in May, compared to a downwardly revised 165,000 jobs in April. The May reading was well above expectations of 185,000.

Bureau of Labor Statistics

With inflation appearing to remain above its target level, and hiring remaining strong, several Fed leaders have indicated in public comments over the past few weeks that the Fed is in no rush to cut interest rates.

The Federal Open Market Committee meets this week, and the Fed is expected to keep its benchmark interest rate in a range of 5.25% to 5.50%. This will be the seventh straight meeting for the Fed to hold its benchmark interest rate at its highest level in 23 years.

The Fed will update its summary of economic forecasts for the first time since March, and the market will be looking to see how many interest rate cuts the Fed expects over the remainder of the year. With only four more FOMC meetings before the end of the year, speculation ranges between one and two, but there is little chance there will be no cuts before 2025.

A small minority, such as Minneapolis Fed President Neel Kashkari, a non-voting member of the Federal Open Market Committee, would not rule out raising interest rates.

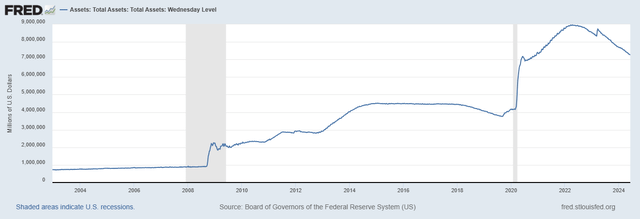

As for the less public part of its monetary policy, the Fed has also made significant progress on its quantitative program. After peaking at just under $9 trillion in the second quarter of 2022, the Fed has reduced the size of its balance sheet to $7.25 trillion. This represents $1.7 trillion in volume, or a 19% decrease. The Fed’s total assets now stand at the lowest level since December 2020. They also represent a 36% decline in pandemic-related asset growth due to quantitative easing.

unique

Starting this month, the Fed has begun to reduce returns of Treasury securities, so the pace of QT will slow. The Fed will now have a cap of $25 billion per month on returns of Treasury securities, down from a cap of $60 billion per month over the past 18 months.

Bank of Japan

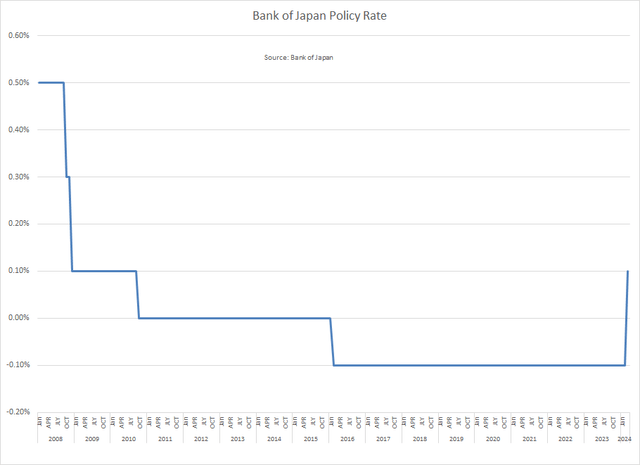

Japan was the outlier among the G7 countries. Over the past two years, while other central banks were raising interest rates to fight inflation, the Bank of Japan (“BOJ”) maintained easy monetary policy. They also witnessed a sharp rise in inflation rates, but they did not change their policies to combat it.

Until this year.

In March, the Bank of Japan reversed eight years of negative interest rates and raised interest rates from a range of -0.1% to 0.0% to a range of 0.0% to 0.1%.

Bank of Japan

While this was the first tightening move by the Bank of Japan, there is still a wide yield gap between the Bank of Japan and the world’s other major central banks. Because of these yield differentials, bond yields rose and the yen weakened.

For a detailed analysis, please see my recent Seeking Alpha article, “Japanese government bond yields at 13-year high, while yen hits 34-year low.”

Despite the tightening in March, the market is calling for further tightening to narrow the yield gap.

The Bank of Japan meets this week, and there is a possibility it will tighten policy again while raising interest rates again, although a rate hike in July is more likely.

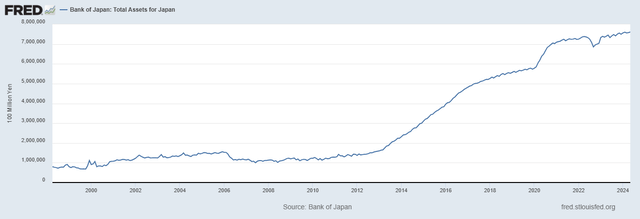

The Bank of Japan is also looking to reduce its asset purchases. Over the past two years, while other central banks were implementing a QT policy to shrink their balance sheets, the Bank of Japan continued its policy of quantitative easing through regularly scheduled asset purchases.

As a result, the Bank of Japan’s balance sheet reached an all-time high of 761 trillion yen.

unique

In May, Bank of Japan Governor Kazuo Ueda said:

“It is appropriate for the bank to reduce the amount of Japanese government purchases as it proceeds with its exit from broad-based monetary easing.”

At the Bank of Japan’s meeting this week, they are expected to discuss reducing their monthly bond purchases. Currently, the Bank of Japan buys 6 trillion yen worth of Japanese government bonds a month. If a cut in bond purchases is passed, the Bank of Japan will effectively implement the QT policy de facto as it faces nearly 5.8 trillion yen per month in 2019. JGB maturities.

By purchasing fewer Japanese government bonds than the number due each month, the Bank of Japan will begin to reduce its balance sheet, or begin implementing QT.

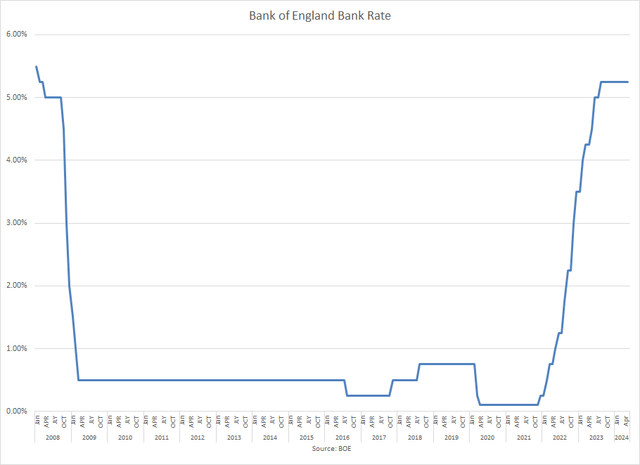

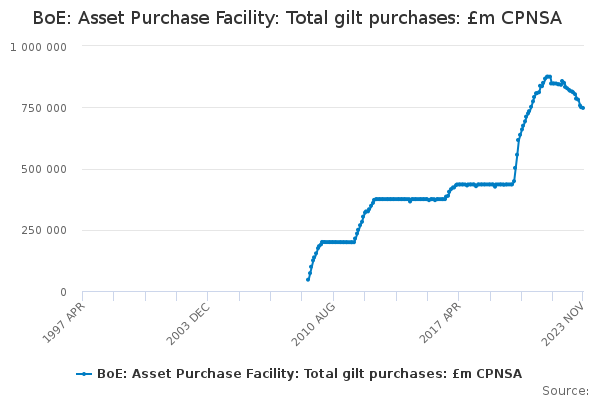

Bank of England

The Bank of England’s Monetary Policy Committee raised interest rates to their highest level in 16 years at 5.25% last August to combat inflation, and has kept prices at that level since then.

Bank of England

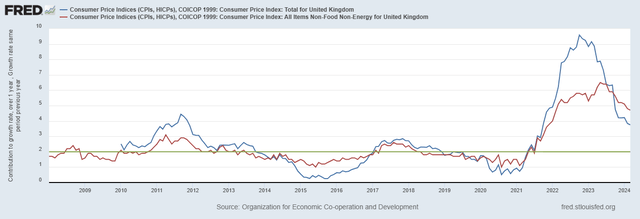

Despite strong monetary tightening, inflation has remained stubbornly high, well above the target rate of 2%. The core CPI (excluding food and energy) was 3.9% in April.

unique

Services inflation was higher in April, at 5.9%.

In addition, there is uncertainty on the labor front, with strong wage growth of 6%, even as unemployment rates rise to 4.3%, their highest level in almost a year.

Given this background, when the Monetary Policy Committee meets on June 20yThey are expected to keep interest rates at the current level again. Despite the approaching general election on July 4thyhigher-than-expected core inflation extinguished any hopes of a rate cut before the election.

The Bank of England continued to reduce its balance sheet through QT. After peaking at £895bn, their bond holdings now stand at £700bn, a decline of 22%.

Office for National Statistics

The Bank of England is the first central bank to implement the QT program through asset sales, rather than redemptions. Although they incurred significant losses on their bond sales, the Treasury offset these losses through an offset agreement. This cost is ultimately borne by taxpayers.

Conclusion

While at the beginning of 2024, the world’s major central banks were all on the same page in expecting inflation to reach their 2% target, which would allow them to lower policy interest rates, erratic inflation paths have played into their monetary policies. Distancing policies.

The Bank of Canada and the European Central Bank, which together represent 4 of the G7 countries, have cut interest rates once each this year. Two other G7 central banks, the Federal Reserve and the Bank of England, have refrained from easing monetary policy due to the instability they have seen in their battle to reduce inflation. The last G7 central bank, the Bank of Japan, went in the opposite direction, raising interest rates, marking its first step towards tightening monetary policy after many years of easy money.

The Bank of Canada and the European Central Bank are experiencing an internal struggle with their monetary policy, as they are easing by cutting interest rates, while at the same time tightening monetary policy by continuing with QT policies.

This is an unusual period where we have such a wide divergence in the implementation of their monetary policies by the world’s major central banks as they are all trying to achieve the same target of 2% inflation.