Vivek Vishwakarma

The median wage in America has risen significantly over the past five years, with annual growth of 7-8% in just the past two years. For families with low debt burdens and closed mortgages Lower fixed interest rates, resulting in higher income available for investment.

Although it may be tempting to buy high-flying stocks like Apple (AAPL) with the remaining surplus from high salaries, I prefer to spend the higher income to buy high-quality stocks that are trading at reasonably low valuations, and in some cases much more. Less than it was 10 years ago.

This way, I get the benefit of “time travel” by using inflation-adjusted income to buy stocks at pre-inflation prices. This brings me to my next two picks, which recently dropped in price Trading is much lower than they were 10 years ago. Both pay solid dividends in the 6-9% range which are well covered by cash flow, so let’s get started!

#1: Bristol-Myers Squibb – 6% yield

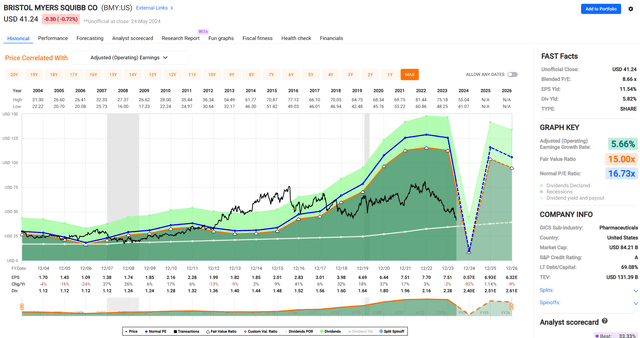

Bristol Myers Squibb (BMY) is a pharmaceutical giant focused on oncology, cardiovascular and immune disorders. BMY’s performance hasn’t been strong over the past 12 months, to say the least, with its stock down 38% over this time. Looking over a longer period of time, BMY is currently sitting even lower than it was 10 years ago, when it was trading at $49.74, as shown below.

BMI Stock (Searching for Alpha)

The market isn’t very interested in BMY at the moment, and that’s likely because it faces generic competitor Revlimid, the blockbuster BMY drug that treats leukemia, MDS. Despite these concerns, BMY still managed to grow its revenue in Q1 2024 by 6% year-on-year on a FX-neutral basis (5% growth including currency effects). This growth was driven by newer drugs Reblozyl, Eliquis and Opdualag, which were partially offset by lower sales of Revlimid and Opdivo.

Investors may also overlook BMY’s pipeline, as it plans to expand into new indications for already approved drugs such as Opdualag (for melanoma), Camzyos (for cardiomyopathy), and Breyanzi (for lymphoma). Additionally, recent acquisitions such as KarXT are set to support BMY’s clinical development programs. This includes treatments for Alzheimer’s disease, which represents a huge market opportunity because it affects nearly 7 million patients in the United States alone. This was addressed by BMY’s CFO during a recent Q&A session of the Bank of America Global Health Conference (BAC):

s: Well, I think there’s another type of player moving into the Alzheimer’s action space as well. I mean they’re developing it. Just kind of your perspective in terms of how this type of market will evolve?

a: Yes. Look, it’s a huge unmet need. (For) caregivers who support patients with Alzheimer’s disease, whether psychotic or agitated, (there is) a significant unmet need for these patients. So having something that addresses this where there is something is going to have a huge impact on the healthcare system overall and improve the quality of life of people as well as caregivers.

We’ll see how the other competition comes out, but we feel really strong. We’ll have to see the data emerge. But as we said before, this is a really big opportunity for us. We see multiple indicators worth billions of dollars. We even see bipolar disorder as an opportunity for KarXT as well.

Meanwhile, BMY maintains a strong balance sheet with an ‘A’ credit rating from S&P, $10 billion in cash and short-term investments, and a safe net debt to TTM EBITDA ratio of 1.56x. It has paid off $10 billion in debt over the past two years alone, including $3 billion already paid off during the first quarter of 2024.

The recent share price decline has pushed BMY’s dividend yield to 5.8% and the dividend is well covered with a payout ratio of 33% based on management’s 2024 adjusted EPS guidance of $7.25 at the midpoint. BMY has also paid a dividend for 93 consecutive years and has raised it annually for the past 15 years.

At the current price of $41.23, there is no doubt that BMY is trading in the bargain basket with a forward P/E of just 5.7x, based on the adjusted EPS guidance mentioned above, which is well below its historical P/E of 16.7, as shown below. .

Quick charts

While BMY’s earnings growth could be lumpy due to patent cliffs and new product launches, I believe the current valuation represents a very bearish trend. With a promising pipeline and a 5% yield, BMY can deliver long-term annualized total returns (dividends plus EPS growth) in the high single digits to the low teens even without reverting to mid-range valuation.

#2: MPLX LP – 8.5% yield

MPLX LP (MPLX) is a master limited partnership that issues a Schedule K-1. It owns and operates a strong portfolio of energy, storage and onshore offshore assets through its general partner, Marathon Petroleum (MPC). Like BMY, MPLX is another stock that is trading much lower than it was 10 years ago, as shown below.

MPLX shares (Searching for Alpha)

Unlike its counterpart Enterprise Products Partners (EPD), which is heavily involved in Texas’ Permian Basin and export facilities in Houston, MPLX is focused on the Appalachian region and export facilities on the East Coast, although it has acquired the US Gulf Coast. The facility for several years was known as Mount Airy Station.

Most investors turn to MPLX for its stable and growing cash flows due to its largely contract and/or fee-based business model, with its sponsor, Marathon Petroleum, being its primary client. MPLX has not disappointed on this front, increasing its EBITDA and DCF (distributable cash flow) by 6.4% and 7.7% CAGR since 2020.

MPLX is also benefiting from the inflationary environment, as evidenced by a 13% y/y tariff increase during the first quarter of 2024, which offsets a 6% y/y decline in pipeline volume during the same quarter. Higher tariffs combined with a 9% and 7% increase in natural gas processing and fractionation volumes contributed to a 7.6% year-over-year EBITDA increase during the first quarter.

It is worth noting that MPLX is expanding its presence in the Permian Basin, with a natural gas processing plant, Preakness II, with a capacity of 200 million cubic feet per day, and is expected to be available during the second quarter of 2024.

Meanwhile, MPLX carries one of the strongest balance sheets in the transportation sector, with a BBB credit rating from S&P and a net debt-to-EBITDA ratio of 3.2x, below 3.5x from the prior-year period, and slightly above 3.0x. . The influence of enterprise product partners.

At present, MPLX is yielding an attractive yield of 8.5% and distribution is well covered by a DCF-to-distribution coverage ratio of 1.6x, leaving plenty of capital locked up to fund internal growth. It has grown its distribution by 10% annually over the past two years, and given its strong results so far this year, it is on track to deliver an annual distribution increase in the fourth quarter.

I find MPLX attractive after its price recently dropped from the $42 level to $40.21 at the moment. With a price-to-cash flow of 7.5x, MPLX is reasonably attractive, especially compared to many high-priced tech giants with little to no yield. With an 8.5% yield, MPLX can produce long-term DCF growth (which is below management’s expectations) in order to deliver market-level returns, with plenty of upside potential beyond that.

As shown below, MPLX’s valuation falls slightly below EPD’s valuation of 7.6x P/CF, and higher than Kinder Morgan’s (KMI) 6.7x, due in part to MPLX’s recent faster growth and better balance sheet.

MPLX vs peer price to CF (Searching for Alpha)

Investor takeaways

Bristol Myers Squibb and MPLX LP offer a compelling opportunity to purchase undervalued high-yield stocks that offer strong dividend yields and long-term growth potential. BMY offers a solid 6% yield backed by a strong pipeline and strong balance sheet, despite current market challenges. Meanwhile, MPLX is yielding an impressive 8.5%, supported by stable cash flows and strategic expansions in natural gas infrastructure. Both companies are trading below their recent prices, offering investors an opportunity to acquire high-quality shares at a discount.