Trevor Williams

As a dividend growth investor, healthcare is one of my favorite sectors where you can find companies with proven track records of growth that allow for long periods of dividend growth.

This sector tends to be more recession-resistant More than most, people are looking for food fixes regardless of the state of the economy. These companies are more likely to produce consistent revenue and earnings growth, which may allow shareholders to receive annual dividend increases.

One name that has always piqued my interest is Cardinal Health Inc. (New York Stock Exchange: Kah), which has paid ever-increasing dividends for nearly 40 consecutive years.

The stock has also performed well, with shares up more than 13% in the past 12 months.

Seeking alpha

An increase in stock price has increased the valuation above the stock price Average, which makes the name an unattractive investment option in my opinion.

Background and recent earnings results

(MCK) and Cencora, Inc. (COR), formerly known as AmerisourceBergen Corporation, Cardinal Health is one of the “Big Three” pharmaceutical distribution companies. The company provides solutions for hospitals, clinical laboratories, physician offices, pharmacies, and more.

Cardinal Health consists of three operating segments, including Pharmaceutical & Specialty Solutions, which distributes branded and generic pharmaceutical and consumer products in the United States, Global Medical Products and Distribution, which distributes branded medical and surgical products in both domestic and international markets, and Other. , which provides home solutions, nuclear and precision sanitary solutions, and OptiFreight Logistics.

Cardinal Health reported third-quarter earnings results on May 2Second abbreviation, 2024. Revenue grew 9% to approximately $55 billion, while adjusted EPS of $2.08 compared favorably to $1.74 a year earlier. Adjusted earnings per share were better than expected, but revenue was $1.2 billion less than what the analyst community had expected.

Revenues from the Pharmaceuticals and Specialty Solutions segment, which represents the bulk of sales, rose 9% to $50.7 billion. Profits of this sector increased by 4% year-on-year. The primary driver of growth during the quarter was increased branded and specialty drug volumes for existing customers. Even with these gains, the sector’s profit margin fell by 5 basis points to 1.15%.

The global medical products and distribution company posted 4% sales growth to $3.1 billion. Segment profit totaled $20 million and was much better than the $46 million loss in the previous quarter. Sector margin turned positive and improved by 218 basis points to 0.64%.

Other revenues of $1.2 billion were up 14% from the prior year due to gains across all businesses, while segment profits improved 4.7% to $111 million. Profit margin fell 83 basis points to 9.51%.

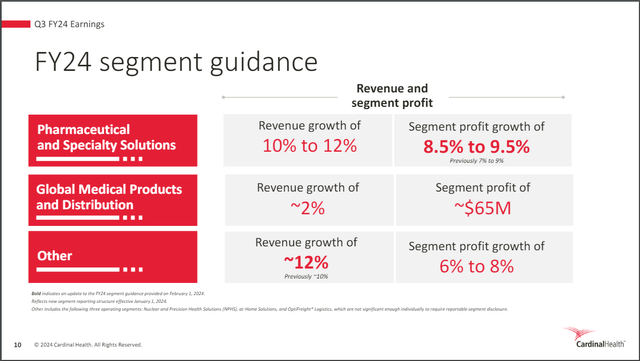

Cardinal Health provided updated guidance for the fiscal year which is interesting.

Cardinal Health Investor Relations

The company expects double-digit revenue growth for its Other, Pharmaceutical and Specialty Solutions segments, the latter of which now has a midpoint for segment earnings growth of 9% compared to 8% previously.

This raised expectations for adjusted EPS to between $7.30 and $7.40, up from $7.20 to $7.35. At the midpoint, this would represent 27% growth compared to FY2023.

Additionally, Cardinal Health provided its initial guidance for fiscal year 2025. Growth for the next fiscal year is expected to be at least 2% compared to the midpoint of the revised guidance.

Earnings analysis

Operating in an area of the economy that is typically more immune to the effects of an economic downturn has enabled Cardinal Health to increase its profits for 37 consecutive years. As such, the company is one of fewer than 70 names with the quarter-century of dividend increases required to earn the Dividend Aristocrat title.

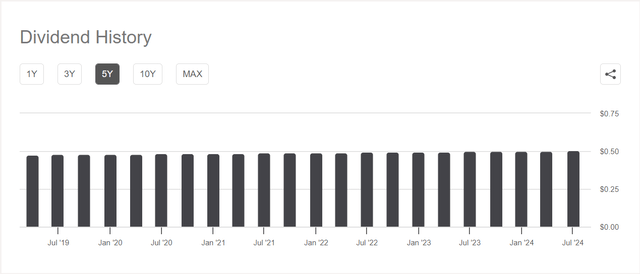

However, the dividend amount has barely budged over the past five years.

Seeking alpha

The dividend’s compound annual growth rate is just 0.7% over the past half-decade, compared to a compound annual growth rate of 4.7% for the period from 2014 to 2023. The most recent increase announced earlier this month was just 1%.

A significant slowdown in earnings growth could signal an impending cut, but Cardinal Health has an expected dividend payout ratio of 28% for this fiscal year. This compares favorably with the average 10-year payout ratio of 35%. Therefore, Cardinal Health is unlikely to cut its dividend, as it is comfortably covered by profits.

The company’s shares offer a 2.1% yield, which, according to Seeking Alpha, is higher than the healthcare sector average, but lower than Cardinal Health’s five-year average yield of 3.2%.

Risks of Investing in Cardinal Health

Even with the improving earnings growth outlook, there are several risks that investors should be aware of before buying the stock.

Cardinal Health has very small profit margins, as evidenced by the company’s sector results last quarter. During this period, the profit margin was only 1.3%, compared to 1.2% last year. Operating a business on razor-thin margins can make navigating weaker periods very difficult.

This can be the case even during periods of growth. The pharmaceutical and specialty solutions company achieved strong revenue and profit growth during the first quarter, but its profit margin remained shrinking. On the positive side, the profit margin for the other category remained high even after its decline, and it was a good indicator that the margins turned positive for the International Medical Products and Distribution Company.

Turning to forward estimates, Cardinal Health’s fiscal 2024 should be much improved over fiscal 2023, with adjusted EPS growth in the high 20% range, but this is expected to be a significant one-time results increase. The company’s preliminary guidance for fiscal 2025 calls for growth that is broadly similar to its recent performance. For context, Cardinal Health’s earnings per share have achieved a compound annual growth rate of 1.8% and 4.2% over the past five and 10 years, respectively.

Given the high base from which earnings per share start, it may be difficult for Cardinal Health to grow at a higher rate than investors are accustomed to in the medium and long term.

The impact on the company’s ability to grow will be the cancellation of contracts. One example is the upcoming loss of a contract with OptumRx, a subsidiary of UnitedHealth Group (UNH). This contract, which is scheduled to expire at the end of June, deals primarily with bulk shipments of non-specialty products.

While the impending loss of this revenue stream doesn’t necessarily put Cardinal Health in dire straits, it does mean that clients sometimes let contracts expire. Too many of these types of losses, and Cardinal Health’s very weak margins will be under tremendous pressure.

OptumRx represented 16% of revenue in fiscal 2023, which could mean near-term earnings estimates could be more difficult to achieve.

Evaluation analysis

With shares closing the trading week at just over $96, Cardinal Health is trading at a forward price-earnings ratio of 13.1. This represents a significant discount to the healthcare sector as a whole, but the stock is trading at a premium compared to its medium-term historical average of 11.4. High growth is likely while the market pays an above-average multiple for the name.

I usually set a valuation range of what I’m willing to pay for the stock. I think this helps account for positive and negative developments that can affect the multiples the market assigns to the stock.

Cardinal Health has established itself as a leader in the pharmaceutical distribution industry. The company has a strong history of earnings growth as well.

However, the earnings growth the company is set to see this fiscal year could just be a one-time story and could be affected by the loss of a large contract. While the dividend is likely safe, the lack of dividend growth over the past five years is concerning, with the recent increase being of the nominal type. The lower yield does not adequately compensate for the lack of earnings growth rate, in my view.

I have set an earnings per share target of 10 to 11 times earnings per share estimates. Therefore, Cardinal Health’s target price range is $73.50 to $80.85. Using my price range, the company’s shares are somewhere between 16% to 23% overvalued at present.

Final thoughts

Cardinal Health has some attractive qualities, including being a leader in its industry and having a nearly four-decade earnings growth streak.

However, there are some issues with the name, namely small margins, low earnings growth, and a higher than usual valuation for the stock. Shares would need to decline by at least a mid-teens percentage for me to find Cardinal Health’s price attractive, which leads me to rate the stock as a Sell at current levels.