ryasick

N.N. Group (OTCPK:NNGPF) (OTCPK:NNGRY) currently offers a high dividend yield that is sustainable over the long term and has a discounted valuation in the European insurance sector.

As I covered in a previous article, I see NN Group As a good income choice in the European insurance sector, due to its high dividend yield and attractive valuation.

Since then, its shares have risen more than 25%, including dividends, so after the strong rise in share prices, I think now is a good time to reconsider its investment case, to see whether or not it will remain an attractive income option in Europe. Insurance sector.

Business overview

Nationale Nerderlanden (NN Group) is a Dutch insurance company, offering life and non-life insurance to its customers, as well as some banking products. It is present in many European countries and Japan, although its domestic market remains the same Big stone. Its shares are traded in the United States on the over-the-counter market, and its current market value is approximately $14 billion.

The company operates in eleven countries, has approximately 19 million customers, and operates on a multi-brand approach. NN Group was also active in asset management, but sold this business segment to… Goldman Sachs (GS) in 2022 by about 1.7 billion euros.

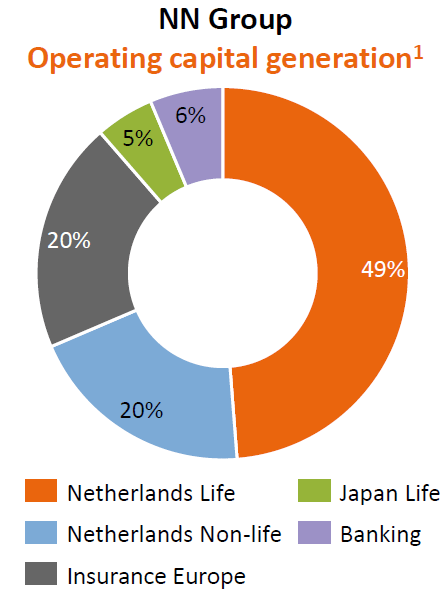

Following this asset sale, NN Group’s business has become more concentrated in domestic insurance operations, which were responsible for about 69% of organic capital generation last year, followed by insurance in other European countries, while Japan and banking have much smaller contributions. . .

Organic capital (NN Group)

This indicates that its core business is life insurance, while it also offers complementary non-life products, in addition to banking products (primarily mortgages and savings). Given this business directed at the life sector, NN Group’s closest peers are other European insurers with significant operations in the life sector, e.g. AXA SA (otqqqx:aksahi), ageas (OTCPK:AGESY), or ASR Netherlands (Otkbk: Show me).

In the Dutch life insurance market it has a leading position, with a market share of about 40% in pensions, while in the non-life sector it is the second largest company with a market share of about 27%. In the Netherlands, it has bancassurance partnerships with four of the country’s five largest banks, with Rabobank being the only exception. In other European countries, it holds the top three positions in several countries, but overall it is not a leading company.

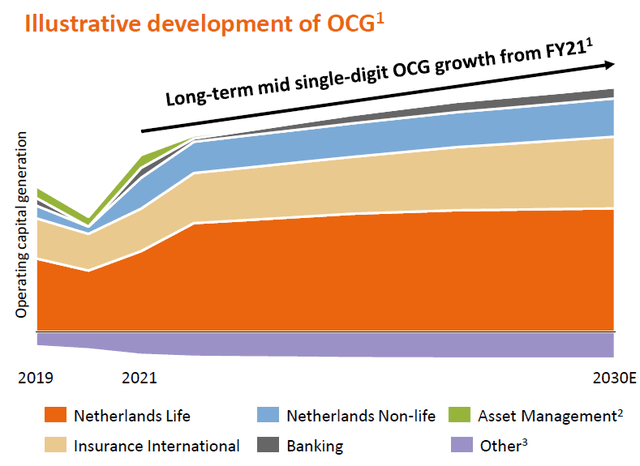

With its strong market presence in the Netherlands and insurance being a mature industry in Europe and Japan, NN Group’s long-term growth prospects are relatively weak. In fact, one of its key operational metrics is operating capital generation (OCG), which reached €1.9 billion in 2023, which is already in line with its new target by 2025 (recently revised from €1.8 billion). In the long term, its ambition is to grow OCG by mid-single digits, which indicates that its business growth over the coming years is expected to be relatively low.

Long-term growth (NN Group)

This means that its growth strategy is expected to remain primarily focused on organic growth initiatives, with the aim of improving its efficiency and profitability over the next few years, but its business profile is not expected to change much compared to its current profile in the near future.

Financial evaluation

Regarding its financial performance, the NN Group reported relatively positive results last year, as insurance income rose 1.8% year-on-year to nearly €10.5 billion, and its operating results improved to more than €2.5 billion in 2023. Asset Management Business The group’s operating results increased by 7.6% year-on-year.

The improvement was mainly supported by its European insurance and banking operations, while its domestic segment (both life and non-life) reported slightly lower operating results last year. In the life sector, this was justified by lower risk adjustment issues and in the non-life sector due to higher claims costs in the disability business line. Net result from continuing operations was approximately €1.2 billion, nearly double the prior year, when adjusted for the sale of NN Investment Partners and other one-time impacts.

Investors should note that in the fourth quarter of 2023, NN Group booked a provision of €362 million related to the unit interconnection litigation case, in which clients were complaining about some cost reductions and a Dutch court ruled contrary to NN.

The company was able to reach a settlement with the interest groups in January, resulting in a provision of €300 million, while clients who were not part of the interest groups accounted for a small portion of the potential lawsuits and the company decided to provide an additional €60 million. Designed to cover these cases. NN considers that the residual risk is not material taking into account measures taken to compensate policyholders over time; Therefore, additional costs related to this issue are unlikely to occur in the future.

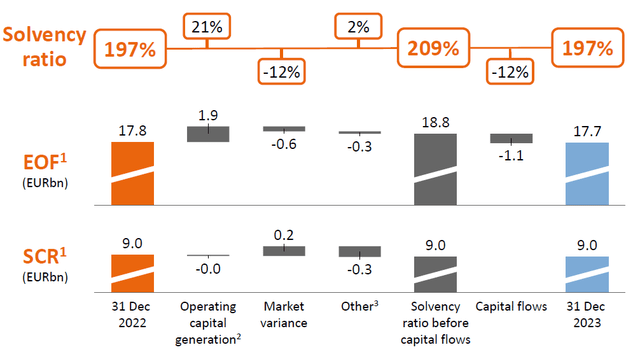

Another positive step taken by NN to reduce risks on its balance sheet was its decision to enter into reinsurance contracts in the Dutch life sector, which reduced the longevity risk in its pension products relating to approximately €13 billion of pension liabilities. By reducing this risk on its balance sheet, its solvency ratio improved by about 8 percentage points, which is also positive for a lower interest rate sensitivity of its solvency ratio going forward.

Despite this, NN Group’s solvency ratio stood at 197% at the end of 2023, relatively unchanged from the previous year, as the benefit of its strong organic capital generation and long-term transactions was offset by market movements and capital returns to shareholders.

Solvency ratio (NN Group)

The solvency ratio is very good and broadly in line with the European insurance sector average, and NN Group is therefore able to return most of its annual capital to shareholders.

In fact, the company has had a very good history of capital returns over the past few years, whether through dividends or share buybacks. The latest annual dividend was €3.20 per share, driven by an interim dividend of €1.12 per share and a final dividend of €2.08 per share, representing an annual increase of 14.7% year-on-year. At its current share price, NN Group offers a dividend yield of about 7.1%, which is very attractive to income investors.

On top of these dividends, the company also made a share buyback of €250 million, resulting in a total capital return of around €1.05 billion in 2023. For 2024, its guidance is to increase its dividend by about 12.5% compared to the previous year. year and implemented a share buyback program worth €300 million, increasing total capital returns to €1.2 billion.

While a high dividend yield can sometimes be a sign of poor dividend sustainability, this is not the case for NN Group. Its dividend is covered by organic free cash flow generation, which amounted to around €1.4 billion in 2023 and is expected to grow to around €1.6 billion by 2025. This means that NN Group generates enough cash to fund its dividend policy. and share repurchase programmes, as well as keeping some cash at the holding level due to the conservative approach.

Therefore, its dividend is clearly sustainable and it has good growth prospects over the coming years, a profile that the Street also seems to acknowledge. In fact, according to analyst estimates, NN Group’s earnings are expected to grow over the next few years, to around €3.88 per share by 2026, which could improve its dividend yield further in the medium term.

Evaluation and risks

In terms of its valuation, NN Group currently trades at a book value of just 0.65 times, which is a modest valuation compared to its closest peers, but in line with its historical average over the past couple of years, although its profitability has improved somewhat in recent years. .

On a relative basis, I see ASR Nederland and Ageas as better peers given their focus on the Benelux insurance market. Both competitors are currently trading at around 1.2 times book value, which could show that NN Group is undervalued.

However, NN Group’s profitability has historically been significantly lower than its peers (ROE averaging around 6-7% versus double-digit levels of peers); Hence I think it is also necessary to make an absolute assessment as to whether NN is truly undervalued or not.

Using the Gordon growth model, and assuming a cost of equity of about 7%, based on a historical beta of 0.7x over the past two years and a risk-free rate of 2.86% (the 10-year Dutch government interest rate), the fair value is close to Book value. This shows that its shares are currently undervalued, although some discount to its peers is still justified by the lower level of profitability.

In terms of risk, investors should note that life insurance companies typically have a longer duration on the liability side than on the asset side, resulting in a duration mismatch. This is negative for solvency ratios during periods of declining rates if insurers do not hedge interest rate risks. NN Group recognizes this and is hedging its interest rate risk to some extent, but this may not be a perfect hedge and upcoming lower rates may have some negative impact on its solvency ratio and therefore its ability to pay dividends and make share repurchases in the future.

Another potential risk that should not be overlooked is wider credit spreads given that current spreads are relatively narrow compared to historical levels, and therefore widening credit spreads could lead to some investment losses in its bond portfolio and also negatively affect the solvency ratio.

Conclusion

NN Group has significant exposure to mature insurance markets and therefore its growth prospects are very low, making its investment case highly vulnerable to capital returns. In fact, it offers a high dividend yield and also buys back its own shares, which is the most attractive feature for shareholders. In addition, its valuation also appears to be lenient on a relative and absolute basis, making NN Group an interesting income option in the European insurance market.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.