Invesco Mortgage Capital (IVR): An interesting play in the mREIT sector that yields 17.5%

microstockhub

Invesco Mortgage Capital (New York Stock Exchange: Autoresponder) has a high dividend yield covered by profits and its business benefits from potentially lower interest rates in the future, thus providing an interesting mix of income and upside potential over the coming months.

Business overview

Invesco Mortgage Capital is a mortgage real estate investment trust (mREIT), which invests primarily in residential and commercial mortgage-backed securities and mortgage loans. Invesco Mortgage is managed and advised by Invesco Institutional, a subsidiary of Invesco Mortgage Invesco (IVZ), which I recently covered.

With a market cap of about $450 million, Invesco Mortgage is a small REIT by that measure, and its closest competitors are other REITs, including Analy Capital Management (Indigo) or ANC Investment Company (AGNC).

The fund’s primary business is investing in mortgage-backed securities (agency MBS), both residential and commercial, which are guaranteed by a U.S. government agency, such as Ginnie Mae. Like the other mREITs, Invesco Mortgage’s primary objective is to provide attractive risk-adjusted returns to its shareholders, primarily through dividends and secondarily through capital appreciation.

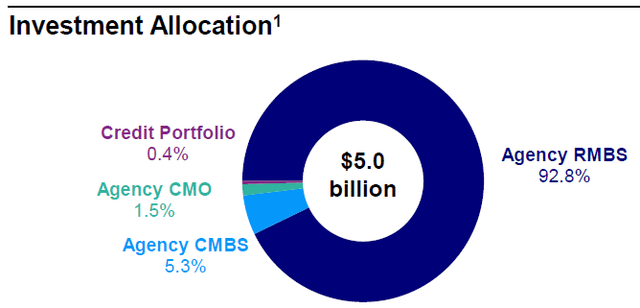

At the end of last quarter, about 92% of its assets, about $5 billion, were invested in residential mortgage-backed securities (RMBS), which are quite safe, while commercial mortgage-backed securities (CMBS) and credit exposure were less heavily weighted. Much in its origins.

Investment portfolio (Invesco Mortgage Capital)

Despite the high interest rates and inflationary environment over the past two years, resilient economic growth and low unemployment have been important factors supporting the residential real estate sector. While new loan origination has declined somewhat, credit delinquencies have remained very low and the prepayment rate has declined, which is generally positive for mortgage loans. In fact, mortgage delinquency rates have remained quite stable at around 3% since the end of 2021, and have shown no significant deterioration from the high rates of the past two years.

Given that the Fed is expected to begin lowering interest rates in the coming months, this backdrop is not expected to change much in the near future, although prepayments may increase depending on how quickly the Fed may lower interest rates. Interest rates, being generally a positive outlook for the Federal Reserve. RMBS.

Interest rate risk

Like its peers, Invesco Mortgage invests in securities that typically have a longer duration, and to fund these purchases it borrows in the repo market. This means that there is a duration mismatch, which makes its balance sheet exposed to interest rate risk, since its assets typically have a much longer interest rate duration than its liabilities.

In general, this is similar to banking, which profits from the interest rate differential between long-term and short-term interest rates. The goal is to make a profit between interest received and interest paid, netted as net interest income, a business model that usually works well when the interest rate curve is upward sloping.

This occurs when long-term interest rates (for example, 30-year interest rates) are higher than short-term rates (two-year interest rates, for example), resulting in positive net interest income if market conditions remain that way. However, market prices are constantly changing, and to manage this risk, the Fund uses financial derivatives to reduce interest rate risk on the balance sheet.

While this business model works well most of the time, since the beginning of 2022, this has changed significantly, when the Fed began its fast-paced hiking campaign. Due to abnormally high levels of inflation, the central bank raised the federal funds rate several times, but this move was not completely followed by long-term interest rates.

Since the market has viewed the increase in inflation as somewhat temporary, long-term interest rates have remained consistently lower than short-term interest rates over the past few quarters, an unfavorable market environment for mobile REITs. Invesco Mortgage is no exception, as rising short-term interest rates represent a headwind to its funding costs, while its asset yields have not risen to the same level, resulting in business margins being significantly lower.

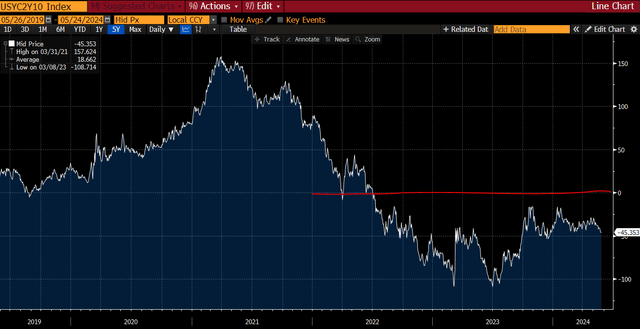

As shown in the following chart, the spread between 10-year and 2-year US government bond yields has been negative since mid-2022 and is currently negative by about 45 basis points. While this has recovered from a negative spread of around 100 basis points in July 2023, it still represents a negative backdrop for mREITs.

US 10-2Y spread (Bloomberg)

This shows that the investment environment has been negative for Invesco Mortgage and its peers over the past two years, resulting in increased uncertainty about agency MBS cash flows and lower overall valuations. Not surprisingly, the mobile REIT sector underperformed the stock market and REIT industry during this period, a trend that may reverse in the coming quarters.

In fact, there are expectations that the Fed will start lowering its target federal funds rate in the second half of 2024, which could serve as a positive tailwind for MBS. Monetary policy normalization is expected to lead to lower interest rate volatility and potentially a steeper yield curve, which is positive for agency MBS ratings and the Trust’s income in the near future.

Financial evaluation

Regarding its financial performance, its record over the past two years has been naturally negative due to the difficult market environment for REITs, which has led to a sharp decline in the book value of the fund, and in fact, the net book value per share has decreased by about 56%. From its peak of nearly $29 per share at the end of 2021.

In 2023, its performance was more stable, but the book value of the stock nevertheless fell by 22% year-on-year to $10 per share, showing that the challenging market environment during the year was still quite negative for its value.

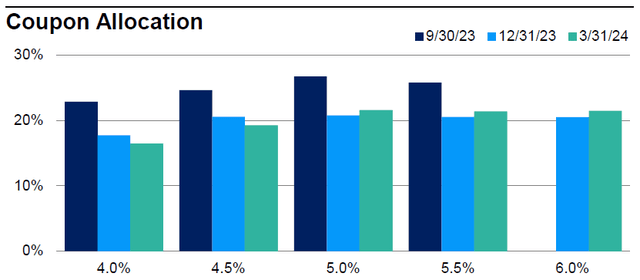

Despite this, Invesco Mortgage has undertaken significant transactions to better prepare its asset portfolio for a low interest rate environment. In fact, during the year Invesco Mortgage sold $5.2 billion and bought $5.9 billion of agency MBS, ending the year with holdings of 30-year fixed-rate agency MBS representing 98% of its total assets.

Through the coupon rate, its agency focused its purchases of mortgage securities on securities with coupons greater than 4%, and on specific groups with attractive prepayment profiles. This strategy was maintained through the first quarter of 2024, as the fund was selling lower coupon holdings and buying higher coupon securities, which should benefit from a potential decline in volatility over the coming months.

Customize the coupon (Invesco Mortgage Capital)

Despite these measures to improve interest rate sensitivity, this has not actually happened in recent quarters, as inflation remains relatively high and the market has put off interest rate cuts. Therefore, market prices have not fallen much in the recent past, as they have been negative for the fund’s income.

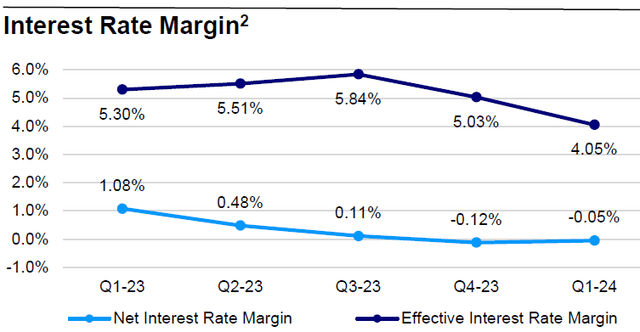

Due to this challenging pricing environment, Invesco Mortgage’s net interest margin has declined continuously over the past two years, reaching a negative level in the past two quarters, as shown in the following chart.

Interest rate margin (Invesco Mortgage Capital)

This means that the fund is currently reporting a net loss on the difference between its asset returns and its funding cost, a very worrying profile given that net interest income is the most important income line. However, last quarter, Invesco Mortgage reported income of $45 million related to interest rate swaps, which was more than enough to cover its operating expenses of just $4.7 million, resulting in net income of nearly $42 million in the first quarter of In 2024, its dividends available for distribution amounted to $0.86 per share.

Somewhat surprisingly, given the cyclical downturn in its business, Invesco Mortgage’s earnings cover by a good margin its dividend, given that its quarterly dividend is $0.40 per share and represents a payout ratio of less than 50%. This means that its current high dividend yield of about 17.5% is sustainable in the short term, even though its long-term sustainability has become more questionable. This occurs because Invesco Mortgage’s business is cyclical and can report high volatility due to market movements; Therefore, investors should treat high dividend yields with some caution.

However, the high dividend yield is not limited to Invesco Mortgage as other REITs, such as Annaly and AGNC, also offer double-digit dividend yields, although with lower yields than Invesco Mortgage. Another supportive factor for the dividend is its relatively conservative leverage position compared to its peers, considering that at the end of last March, its debt-to-equity ratio was 5.6x, a lower level compared to its closest peers.

In terms of valuation, mREITs typically trade close to book value since they hold low-risk, liquid securities that are relatively easy to liquidate. However, Invesco Mortgage also owns certain credit assets and mortgage-backed securities, which may be difficult to liquidate in the current market environment. Therefore, I see its shares trading at 0.9x book value as fair, considering that a small discount to book value seems justified. Historically, the average book value valuation has also been 0.9x book value; Thus Invesco Mortgage appears to be highly valued at the moment.

Conclusion

Invesco Mortgage Capital is an mREIT that invests significantly in secured agency mortgage securities and therefore has very low exposure to credit risk, so interest rate risk is the most important driver of its investment performance. Like other REITs, its business is performing well in a low interest rate environment, and the trust has taken some measures to better take advantage of these tailwinds expected in the second half of the year.

On top of this upside potential, it also offers a very high dividend yield of 17.5%, which appears to be sustainable in the short term, making it an interesting play in the REIT sector at the moment from an income perspective and also as a play. On potentially lower interest rates in the future.