Editorial by Robert Way/iStock via Getty Images

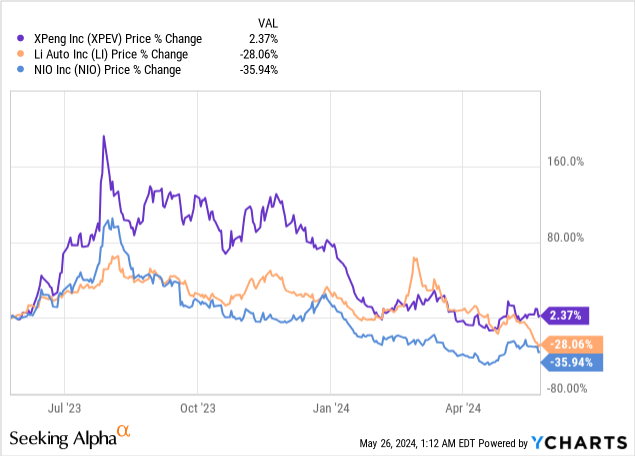

XPeng Shares (NYSE:XPEV) has been sharply rerated this year, even though the electric car maker’s shares rose 26% after the company reported first-quarter 2024 results last week. XPeng’s delivery growth in the first quarter continued to slow because of this Headwinds in the sector include declining demand for electric vehicles as well as increased competition on pricing between a growing number of industry players vying for market share. While XPeng’s delivery milestones weren’t the best, the electric car maker saw an improvement in its margin picture…which was a positive takeaway from the earnings report. Since the stock is still expensive compared to other EV startups in China, I think the best rating for XPeng remains up in the air!

Previous evaluation

I have rated XPeng shares as Hold for February – Sitting On the fence for now The company was lagging behind NIO and Li Auto in terms of delivery growth. Li Auto in particular shattered expectations by delivering triple-digit delivery growth rates as well as strong margins in its electric vehicle business that left competition, including XPeng, in the dust. XPeng is seeing a slight improvement in margins, but I still have concerns about the valuation as Li Auto offers a stronger value proposition, in my opinion.

XPeng beats Q1 2024 estimates

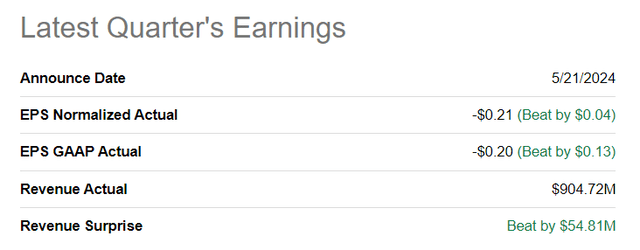

Although XPeng only saw 20% year-over-year delivery growth in its fiscal first quarter, the electric vehicle maker managed to beat consensus expectations: The electric vehicle company generated ($0.21) per share in adjusted earnings On revenue of $904.7. Both the bottom line and the top line exceeded consensus expectations.

Seeking alpha

Decline in 1Q 2024 deliveries, margin trend looks better

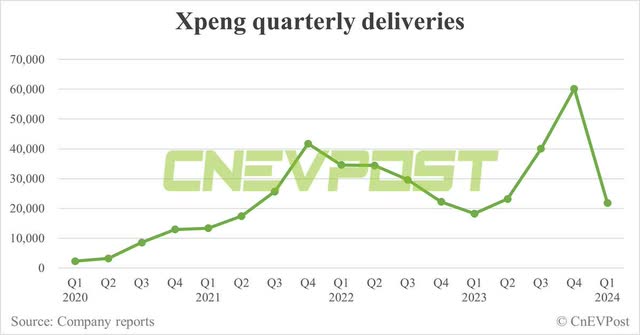

Delivery growth at XPeng is slowing, which was one takeaway from the company’s fiscal first-quarter earnings call last week. XPeng delivered 21,821 electric vehicles in the first quarter of 2024, showing a growth of 19.7% year-on-year. In the previous quarter, XPeng’s deliveries rose 170.9% year-on-year. The decline in deliveries was linked to the Chinese New Year period, which traditionally results in factory closures and lower sales. I expect a rebound in deliveries and revenues as the year progresses, however, the view is supported by XPeng’s upbeat outlook for the fiscal second quarter.

CNEVPOST

Despite seasonal headwinds to the company’s delivery growth in the first quarter, XPeng was able to increase its vehicle-related revenue by 57.8% year-on-year to CNY5.54 billion ($0.77 billion). More importantly, XPeng also experienced a sequential margin improvement and a radical reversal in margin trend compared to the same period of the previous year: In the first quarter of 2024, XPeng’s compound margin reached 5.5%, showing a swing of 8 basis points year-on-year.

For XPeng in particular, it cited the negative margin trend as a key operational risk for the electric vehicle maker as well as a top investment risk for investors in May 2023. The improvement in margin trend was certainly a positive development for the electric vehicle maker in its first fiscal quarter.

XPeng also achieved a profit margin improvement of 1.4 points compared to the previous quarter, indicating that although delivery and revenue growth have slowed, actual operations have become more cost-effective. XPeng has been focusing on lasers in the past year to improve operational efficiency. XPeng even entered into a cooperation and investment partnership with German automaker Volkswagen last year in an attempt to share the risks and costs of developing electric vehicle technology.

XPeng

Forecast for the second quarter of 2024

XPeng’s forecast for deliveries in the fiscal second quarter was the reason the company’s shares rose as much as 26% immediately after the company reported earnings results (although those gains were not sustained).

XPeng expects to deliver between 29,000 and 32,000 electric vehicles in the second quarter, indicating a growth rate of up to 38% year-on-year. In other words, XPeng expects an acceleration in quarterly delivery volume growth in Q2 2024, which may also support the company’s drive to improve its margin profile. In terms of revenue, XPeng expects between CNY7.5-8.3 billion ($1.05-1.17 billion), which means a growth rate of 64% year-on-year.

XPeng Evaluation

The main reason I’m sticking with my assessment of XPeng, despite the EV maker making progress on the thorny issue of vehicle margins, is that the company is still fairly expensive compared to its EV competitors. In my opinion, Li Auto continues to represent the best value for EV investors, largely due to its impressive delivery growth as well as stronger vehicle margins (Li Auto achieved a vehicle margin of 19.3% in Q1 2024 which was 3.5 times higher than XPeng margin).

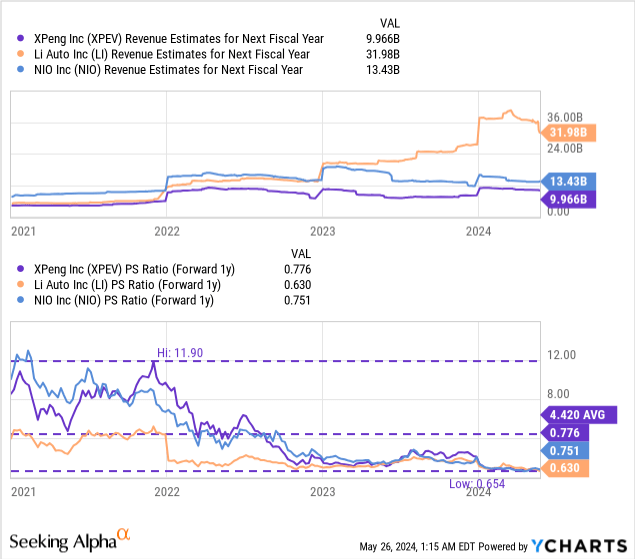

Both Li Auto and NIO trade at lower revenue multiples than XPeng, which is not guaranteed, in my opinion, given Li Auto’s leading margin profile. XPeng is currently priced at a price-to-earnings ratio of 0.78X, which is well below its 3-year average price-to-earnings ratio of 4.4X. In my recent work on XPeng, I mentioned that I see a fair value of $9.50 per share for XPeng (based on the industry group’s average P/E ratio of 0.8X). XPeng shares are currently trading at $8.20, so they are trading just below my fair value estimate. However, I’m staying with my current rating here because XPeng has much lower vehicle margins and because I believe Li Auto continues to offer the deepest value to EV investors in the industry group.

Risks with XPeng

The margin trend is worth following because only EV makers that generate positive vehicle margins for mass production of EVs have a chance of actually making a profit on the bottom line. Obviously a return to negative vehicle margins would be a worst-case scenario for me, but also lower margins in successive quarters (likely driven by more aggressive promotions in the electric vehicle segment) would be a negative development.

Final thoughts

XPeng delivered a strong earnings note for the first quarter of 2024 and beat consensus expectations at the bottom and top. Delivery growth slowed, which was expected due to seasonal effects, but I think margin improvement was the main takeaway from the electric car maker’s earnings release. XPeng still has plenty of potential to expand its production scale in the future, and forecasts for the fiscal second quarter point to a typical second-quarter rebound in deliveries. The only thing I don’t like about XPeng is that the electric car maker is relatively expensive compared to its competitors in the Chinese electric car startup sector. As a result, I will remain at my hold rating after XPeng’s Q1 2024 earnings report!