porcorex

It certainly doesn’t hurt to own quality stocks like Dell Technologies Inc. (DELL) and NVIDIA Corporation (NVDA) these days, as the capital appreciation on these stocks over the past year was equivalent to several years of investment. Market-level performance.

However, holding these stocks can present a dilemma for some investors, because it would be unrealistic for any stock, no matter how great the business, to sustain the types of rallies it has seen recently over the long term.

This means that investors could see years of underperformance after the first years of huge rises. This is because the market trades based on future sentiment and expectations, much of which is already built into its soaring stock prices.

That’s why I prefer to buy undervalued stocks that are expected to give consistent market-wide or market-outperformance over the long term, allowing me to dollar-cost average. Dividends to get more shares at affordable prices.

This brings me to the next two stocks, which are far from overvalued and what I consider to be undervalued with high dividends, offering investors the potential for consistent long-term growth due to their income streams and capital appreciation, so let’s get started!

#1: TC Energy – 7.3% Yield

TC Energy Corporation (TRP) is a large midstream energy company headquartered in Calgary, Canada, with grid pipelines, power generation and storage assets in the United States, Canada and Mexico. It transports about a quarter of North America’s natural gas and a fifth of Western Canada’s crude oil.

(ENB), like its Canadian counterpart Enbridge Inc. (ENB), TRP derives the majority of its earnings (95%) from highly regulated or contractual cash flows, resulting in stable earnings during economic fluctuations.

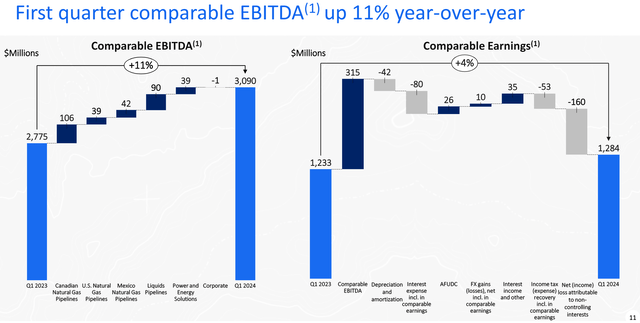

This is reflected in recent results, with EBITDA growing an impressive 11% year over year during the first quarter of 2024, driven by records across multiple natural gas systems including NGTL, Columbia Gas and Columbia Gulf. As shown below, liquids and natural gas pipelines made significant contributions to TRP’s EBITDA growth.

Investor presentation

Furthermore, TRP put nearly $1 billion worth of projects into service during the first quarter. This includes various projects on the NGTL (a system linking natural gas production in Western Canada to domestic and export markets) as well as the $300 million Gillis Access project which will contribute to cash flows this year.

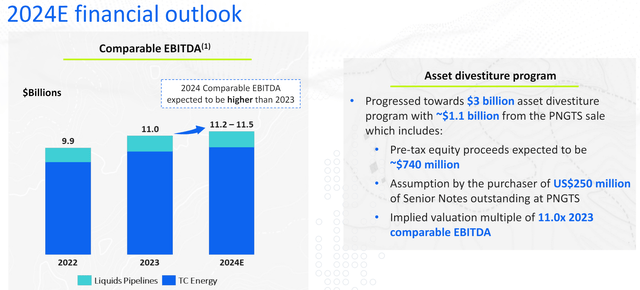

In total, TRP has $7 billion worth of new projects expected to be put into service this year. This includes TRP’s long-awaited Coastal GasLink project, which was completed last year and is currently undergoing post-construction reclamation activities.

Coastal GasLink is expected to be put into commercial service later this year and could be a material driver of TRP’s cash flows. This supports management’s guidance of achieving similar EBITDA growth of 2% to 5% this year, after seeing 11% growth in 2023, as shown below.

Investor presentation

Meanwhile, TRP maintains a healthy balance sheet with a BBB+ credit rating from S&P. The average debt term is 17 years, with 92% of that held at fixed interest rates. Management reiterated its commitment to lower its debt-to-EBITDA ratio to 4.75 times, putting it on par with Canadian peer Enbridge’s 4.6 times debt-to-EBITDA ratio.

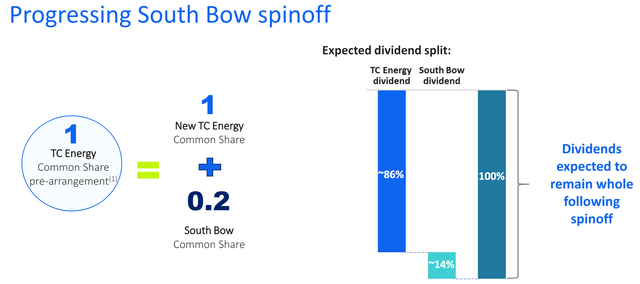

More importantly for income investors, TRP currently yields an attractive 7.3%, and the dividend is covered with a payout ratio of 82%. TRP has also increased its dividend annually for 23 consecutive years, and management is targeting 3-5% annual dividend growth over the medium term. It should be noted that with the upcoming spin-off of South Bow (TRP’s liquids pipeline business), shareholders are expected to be made whole in terms of dividends, with 86% of the dividend share coming from RemainCo (TC Energy) and 14% from SpinCo ( South arch), as shown below.

Investor presentation

The TRP is attractive at the current price of $38.39 with a price-to-cash flow of just 7.45x, which is at the lower end of its 3-year range of 6-11x. Additionally, TRP is competitively priced compared to Enbridge’s peer 7.74x P/CF, as shown below.

TRP vs ENB Price to Cash Flow (Seeking Alpha)

With a yield of 7.3% and management guidance for an EBITDA CAGR in the 3-5% range, TRP can produce market-beating returns even without reference to a median P/E valuation in the 8-10x range. .

#2: VICI Characteristics – 5.9% Yield

VICI Properties Inc. (VICI) is the largest U.S. REIT focused on experiential properties, with a property base that includes irreplaceable assets along the Las Vegas Strip and beyond, and a growing presence in non-gaming family entertainment destinations.

What makes VICI stand out from its net lease peers is the very long leases ranging from 30 to 55 years among its 13 largest tenants. This is much longer than the 10-year average of net lease operators like Realty Income Corporation (O), NNN REIT, Inc. (NNN), and Agree Realty Corporation (ADC).

VICI also benefits from significant exposure to tenants included in the S&P 500 Index (SPY), from which it derives 75% of its rental portfolio. Additionally, 81% of VICI’s rental listing comes with master leases, meaning a tenant who has multiple leases with VICI will still need to pay rent on a vacated property.

VICI has been able to achieve higher AFFO per share growth compared to its peers due to its new opportunities, deal making and business scale. This is reflected in AFFO per share growth of 6.1% year-over-year through the first quarter of 2024, which is higher than the low-to-mid-single-digit AFFO growth of its net-lease peers over the same time.

Notably, VICI’s recent growth is supported by non-gaming properties, including a market-leading athletic training complex called Homefield in Kansas City, Missouri. This complex will soon include the Margaritaville Resort and builds on VICI’s entry into the sports and entertainment sector late last year through the acquisition of a lease interest in Chelsea Piers (an entertainment destination along the Hudson River in New York City).

Management is guiding for a respectable 4.2% growth in AFFO per share this year to $2.15 at the midpoint of the range. This is supported by annual rental lifts and value-enhancing projects, including those at The Venetian Resort in Las Vegas, as management explained during a recent conference call:

Our focus on trust in finding mutually beneficial solutions with our partners multiplies the beneficial impact of each relationship and we believe lays the foundation for future growth through good and bad market environments. One of the best examples of this is our relationship with Apollo and the team in Venice.

Since the acquisition, the Venetian team has exceeded all expectations as Las Vegas continues to establish itself as the entertainment center of the world. We are pleased to expand our close relationship with Apollo further and announced our opportunity to invest up to $700 million in The Venetian through VICI’s Partner Property Growth Fund. This capital investment will fund several projects that seek to improve the overall guest experience and enhance the value of the property.

VICI’s outlook is supported by a strong balance sheet with a BBB- credit rating from S&P and $3.5 billion in total liquidity. It also had a Q1 annualized net debt to EBITDA ratio of 5.4x, falling within management’s target of 5.1x to 5.5x, and below the 6.0x mark generally considered safe by rating agencies.

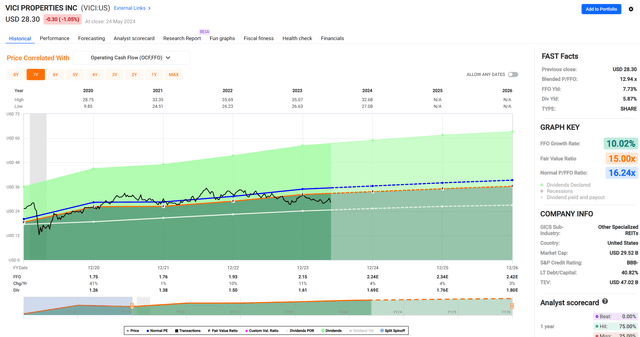

More importantly for income investors, VICI currently yields an attractive 5.9%. The dividend is well covered with a payout ratio of 66% and comes with a 5-year CAGR of 7.8%. VICI stock is also attractive at the current price of $28.30 with a forward P/FFO of 11.1, which is lower than Realty Income’s 12.3, NNN REIT’s 12.5, and Agree Realty’s 14.8.

As shown below, it also falls below the historical P/FFO level of 16.2. With a yield of 5.9%, VICI can be viewed as much more than just a “bond proxy” given its strong balance sheet and future growth prospects. With expectations for AFFO/share growth of at least 4% this year, VICI can deliver market-level performance along with earnings even without a return to its average valuation.

Quick charts

Investor takeaways

Both TC Energy and VICI Properties offer attractive investment opportunities for those seeking consistent long-term growth and reliable sources of income. TC Energy, with its extensive and strategically located energy infrastructure, provides a consistent dividend yield of 7.3% supported by regulated and contracted cash flows.

VICI Properties generates a 5.9% yield supported by long-term leases and strategic investments in high-value assets such as the Venetian Hotel in Las Vegas. Together, these companies embody strong dividend growth, strong balance sheets, and strategic expansion that make them attractive options for income-focused investors looking for quality at discount prices.