JHVEphoto

Result summary

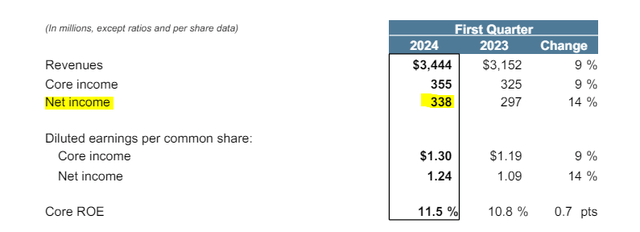

CNA Financial (New York Stock Exchange: CNA) released its first-quarter financial results in May, reporting flat net income of $338 million.

CNA Financial’s Q1 2024 presentation

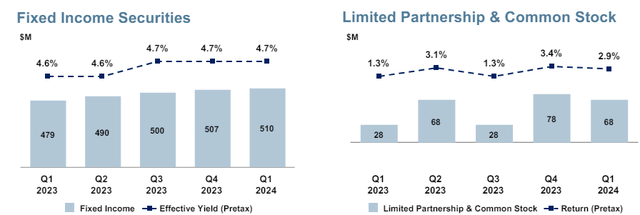

During the quarter, CNA Financial achieved positive earnings due to investment income rising 16% year over year during the year. The effective income yield on fixed income rose to 4.7% from 4.6% year-on-year, driven by the continued impact of higher reinvestment rates. In addition, underwriting performance remained strong, reaching $126 million.

Despite concerns about inflation and catastrophe losses, which led to a slight deterioration in the combined ratio from a year-over-year perspective, CNA Financial was able to maintain steady financial results. CNA Financial has started 2024 well, with a renewal premium change of +6% and a flat retention rate of 85%.

While the current valuation may not be particularly attractive For investors looking for strong returns, the insurance company has consistently delivered consistent results, enabling it to deliver regular dividends to shareholders.

CNA Financial’s Underwriting Performance: Consistently Reliable

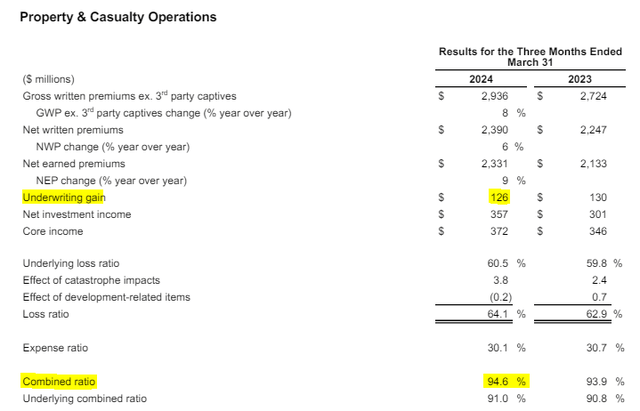

The Property & Casualty segments posted quarterly underwriting gains of $126 million, resulting from a combined ratio of 94.6%.

CNA Financial Report for the first quarter of 2024

This positive quarterly performance of the insurance portfolio can be attributed to the steady, if somewhat deteriorating, underwriting performance of the specialty insurance business and improved margins for third-party insurers.

However, the combined YTD ratio was 94.6%, representing a deterioration of 0.7 points compared to the same period last year. This decrease in the combined ratio year-to-date was impacted by negative liquidation losses and an increase in catastrophe losses, which represented a negative impact of 4.0 points on the combined ratio in total.

Specialized Business Overview:

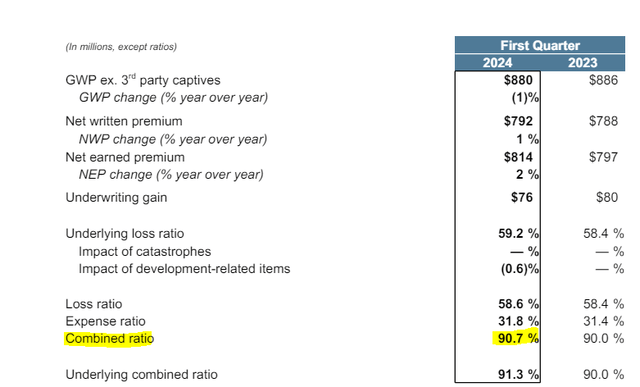

The specialized business, an important component of the insurance portfolio, maintained a stable combined ratio of 90.7% compared to 90% in the same period of the previous year.

CNA Financial Report for the first quarter of 2024

The deterioration in the combined ratio was driven by a deterioration in the underlying combined ratio, which increased by 1.3 points, partially offset by the positive impact of claims development in prior years which improved the loss ratio by 0.6 points, compared to no net development in the prior period in the prior year quarter.

Business overview:

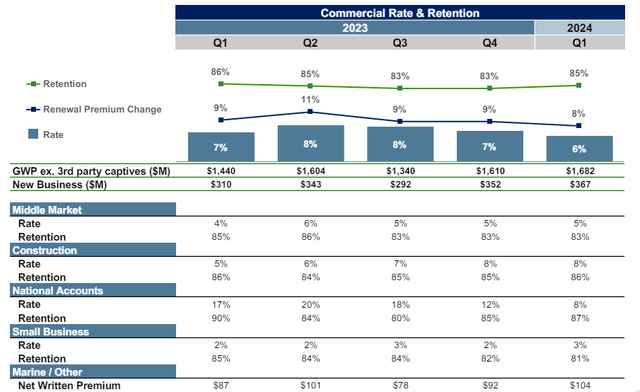

During the first quarter of 2024, CNA Financial’s business demonstrated strong performance, seeing premium growth of 15% on a net basis after reinsurance. This growth was driven by a rate change of 8% and a retention rate of 85%.

CNA Financial Report for the first quarter of 2024

Within this segment, there was a positive underwriting gain of $29 million, or a decrease of $12 million year over year. The decrease in underwriting gains was primarily due to a deterioration in the combined ratio, with a 3.1-point increase in the loss ratio. The commercial insurance portfolio was affected by an increase in catastrophe losses, which amounted to $82 million, or 6.8 loss percentage points, in the quarter compared to $44 million, or 4.2 loss percentage points, in the previous quarter.

Despite lower underwriting gains, the insurer pushed up rates on commercial casualty insurance lines in the United States. In the first quarter, commercial vehicle price increases were up 14%, excess casualties were up 11%, initial overhead liabilities were up mid-single digits with renewal premiums changing by high single digits due to higher revenue and payroll. These price increases are double what they were 6 quarters ago.

International Business Overview:

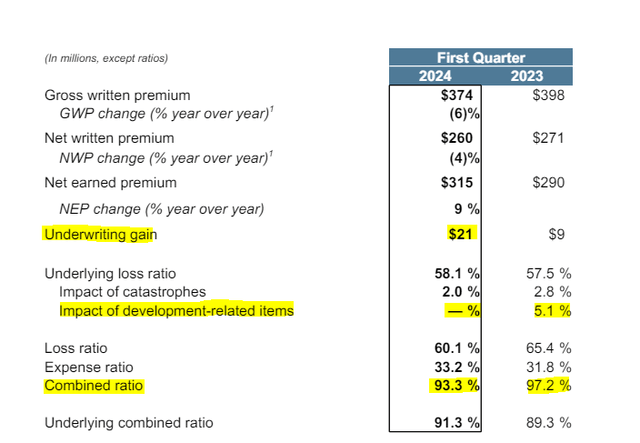

In the first quarter of 2024, pre-tax underwriting gains for CNA Financial’s international activities more than doubled, to $21 million, despite a decline in new business, resulting in lower gross written premiums.

However, underwriting performance improved, with the combined ratio falling from 97.2% to 93.3%. Most of the improvement in underwriting performance was driven by the absence of unfavorable prior claims.

CNA Financial’s Q1 2024 presentation

Given the cumulative rate increases and extensive reunderwriting actions taken by the insurer over the past several years, CNA Financial’s management expects international operations to be an increasingly consistent contributor to the company’s overall profitable growth.

Non-fixed income performance feeds investment income

CNA Financial, like other insurance companies, has benefited from higher average returns on fixed income investments over recent years. However, returns have reached a plateau, with the year-over-year interest rate return being roughly stable at 4.6% to 4.7%. However, net investment income increased by $84 million for the first quarter of 2024 compared to the previous quarter.

CNA Financial’s Q1 2024 presentation

This increase was driven by favorable limited partnership and common stock returns and higher income from fixed income securities as a result of favorable reinvestment rates.

CNA Financial’s Q1 2024 presentation

Going forward, investment returns should continue to grow, the invested asset base should continue to grow and benefit from an interest return of more than 4%. Hence, the investment portfolio will continue to constitute an important source of profits.

For the full year of 2024, current shareholders could expect approximately $2.175 billion or a 5% increase over the full year of 2023, which would result in an effective total portfolio return of close to 4.8% by the end of 2024.

2024 forecast

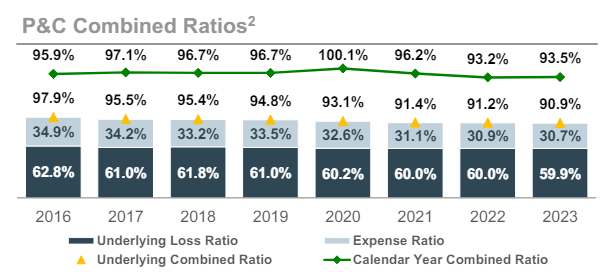

Over the past eight years, the average combined ratio has ranged from 93% to 97%, with the exception of 2020 performance, which was impacted by the COVID-19 pandemic.

CNA Financial Investor Presentation

Although 2022 and 2023 were much better in terms of underwriting performance than previous years, it would be unwise to forecast fiscal 2024 earnings based solely on those years.

CNA Financial’s management has made steady efforts to improve the performance of its insurance portfolio over the past few years. Hence, it is possible that the combined ratio could reach around 93%, but it should be viewed as an optimistic scenario if the underwriting measures in the international and commercial insurance sectors bear fruit.

The base case scenario will see an underwriting margin of 3 to 5 points, meaning a combined ratio that fluctuates between 95% and 97%. In terms of premium volume, the earned premium target of $10 billion remains achievable for 2024.

Therefore, pre-tax underwriting gains for the property and casualty operations could reach $300 to $500 million in 2024. Additionally, pre-tax losses from the ongoing long-term care portfolio are expected to be approximately $1 billion.

With an expected investment income of US$2.175 billion from the life and non-life sectors, total pre-tax earnings will range from US$1.5 to US$1.7 billion. Assuming a corporate tax rate of 21%, this would result in after-tax income of about $1.19 to $1.34 billion.

Therefore, the company appears well positioned to continue delivering steady results and distribute excess capital to shareholders through dividends, without compromising its financial health, despite carrying a debt load of $3 billion.

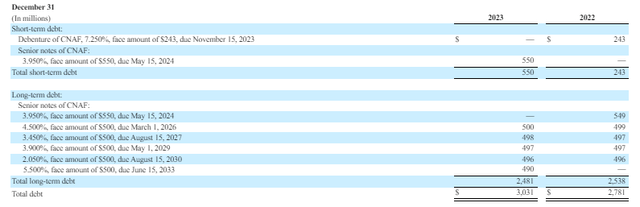

Debt situation: The debt burden is more than manageable

As of December 2023, the debt consists of fixed rate instruments, with 85% of the total debt maturing between 2026 and 2033.

CNA Financial 2023 Annual Report

In 2024, the company issued $500 million of 5.125% unsecured notes due February 15, 2034 to repay the 3.95% notes due May 2024. Although the cost of debt increased slightly, impacting operating profit by about $1 million annually, However, it remains more than acceptable. Simply put, an increased debt burden is manageable and is likely to be offset by higher investment income.

Current rating

CNA Financial’s book value per share is currently $35.62, indicating a price-to-book valuation of around 1.25.

This valuation suggests that the company’s pricing may be relatively attractive compared to other property and casualty insurers, as it typically trades at 1.5 times its book value or higher.

However, CNA’s valuation is heavily influenced by its significant ownership by Loews (L), which owns about 90% of the company. Thus, CNA’s prospects are closely linked to Loews’ management and capital allocation decisions.

Concluding thoughts

As we mentioned in previous articles, CNA Financial may not be a fast-growing stock or be significantly undervalued. However, they offer access to consistent cash flows due to their stable positions in niche markets. Investors should keep in mind that CNA is largely owned by Loews, making it dependent on Loews’ decisions regarding capital allocation.

Investors should remember that CNA is largely owned by Loews, making it dependent on Loews’ decisions regarding capital allocation.

While the upside potential may be somewhat limited, the company’s consistent performance makes it an attractive option for retirees or dividend-focused investors seeking reliable returns. For these investors, purchasing the stock at about 1.0 times book value can provide a margin of safety.