Diverse photography

ABT Stock: Wall Street loves it

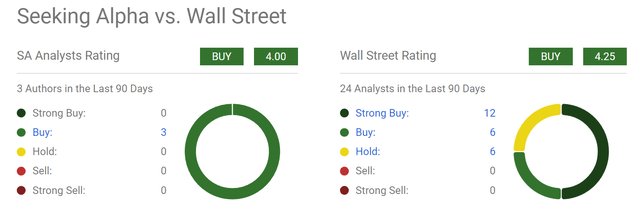

Readers who follow our writing know that we are contrarian investors and typically bet against Wall Street’s ratings. However, in the case of Abbott Laboratories (New York Stock Exchange: APT) stocks, we found ourselves in agreement With Wall Street. More specifically, the chart below summarizes the current sentiment toward ABT stock from Wall Street analysts (and Seeking Alpha writers as well). As we’ve seen, Wall Street analysts have a “Strong Buy” rating on the stock, with 12 out of 24 analysts giving it that rating in the last 90 days. Overall rating is 4.25. The search for Alpha Book ratings is a bit less enthusiastic, but the overall score is 4.0 and indicates a strong buy as well.

Seeking alpha

In the rest of this article, you’ll see why we rate the stock a buy as well. Admittedly, the stock It faces some risks and earnings headwinds (detailed in the last section), but we would argue that a) these risks are relatively minor compared to the positives and b) are already well offset by the stock’s discounted valuation.

ABT Stock: Great business at a discount

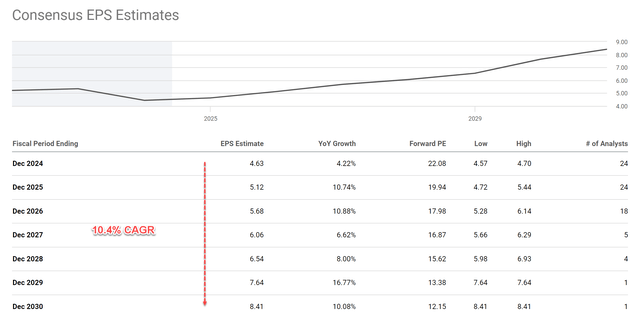

Let me start with growth forecasts and growth drivers. The chart below shows consensus EPS estimates for ABT stock in the next six years. As we’ve seen, analysts expect ABT’s earnings per share to grow at a compound annual growth rate (“CAGR”) of 10.4% over the next six years. This translates to EPS growth from $4.63 in fiscal 2024 to approximately $8.41 by fiscal 2030.

Seeking alpha

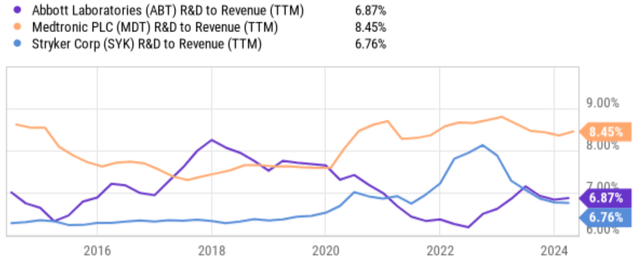

Given the unique strength of ABT’s business model, I am very optimistic about this growth outlook. Two key factors that set ABT apart from other healthcare product companies in my view are its diverse product portfolio and focus on innovation. Unlike many of its peers who focus on specific areas such as pharmaceuticals or medical devices, ABT boasts a diversified portfolio across diagnostics, medical devices, pharmaceuticals and nutritionals. This spread mitigates risk by reducing reliance on the success of any one product or therapeutic area. ABT also continually invests heavily in R&D (see the following chart below). This enables a steady pipeline of new products and technologies, allowing ABT to stay ahead of the curve in a rapidly evolving healthcare landscape.

With this combination of a strong current lineup and pipeline, ABT is well positioned for long-term growth and there are plenty of profit drivers afoot. Notable examples in our opinion are products in the diabetes care, electrophysiology, neuromodulation, and structural heart segments.

The company has also launched quite a few new products, including Amplatzer, Amulet, Navitor, TriClip, and AVEIR. We are optimistic about the success of these new products given the company’s past track record. Last but not least, we see FreeStyle Libre as a strong driver of its long-term growth curve. The popular glucose monitoring system is one of the most successful assets in diabetes care in our view. It is also ABT’s most profitable product, accounting for about 15% of the company’s total profits. FreeStyle Libre has enjoyed strong growth (Sales during the first quarter of 2024 grew more than 22% year over year). We expect the momentum to continue given its user base and unique features.

Seeking alpha

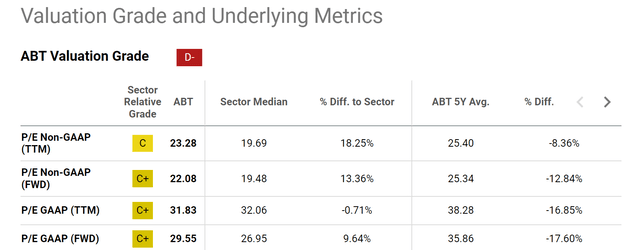

Despite the strong growth outlook, the stock is priced at a discount in our view. If you recall from the chart above, ABT’s forward P/E ratio is around 22x and is expected to decline rapidly as EPS grows (to just 12.15x by 2030). Admittedly, the current front-wheel drive of 22x may feel a little underwhelming when compared to the sector average (about 19.5x). But we believe the premium is well justified given the strength of the business. Given the various factors just mentioned, our view is that it makes sense to compare its current P/E with its historical average, which suggests a significant discount of around 13% in terms of non-GAAP FWD.

Next, we’ll put the valuation into better context compared to the broader market.

Seeking alpha

ABT Stock: Evaluate Valuation and Expected Returns

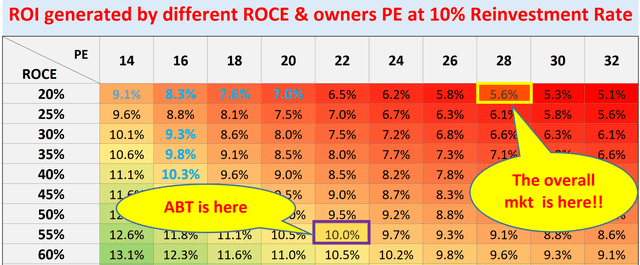

The following chart demonstrates its valuation (as well as expected return) under current conditions versus the overall market. The concepts behind this chart are detailed in our free blog article. The key concepts involved here are ROCE (Return on Capital Employed) and Owner’s Earnings Yield (“OEY”) as explained below:

- A business owner’s long-term ROI is determined simply by two things: a) the price paid to purchase the company and b) the company’s growth rate (which reflects its quality and moat).

- More specifically, Part A is determined by the owner’s earnings yield (“OEY”) when we purchased the company. Part B is determined by the ROCE and RR (Reinvestment Rate) over the long term.

- That is, long-term ROI = OEY + growth rate = OEY + ROCE*reinvestment rate

- For ABT, we approach OEY with the dividend yield being on the conservative side. At the current FY1 P/E of 22x, ABT offers an average lifetime yield of approximately 5%.

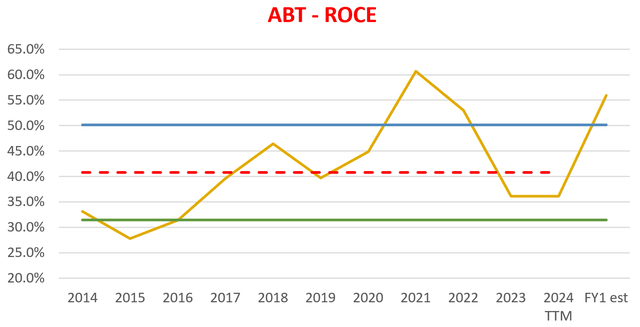

Meanwhile, ABT has maintained an average return on equity (ROCE) of ~41% (see second chart below) over the long term, in contrast to the ~20% level of the overall market. Meanwhile, the overall market is also priced at a higher P/E (the SP500 is priced at around 28 times P/E as of this writing). Given its superior ROCE and low P/E, we expect ABT’s annualized total return potential to be close to double digits, compared to the mid-single digits from the overall market.

author author

Other risks and final thoughts

In terms of downside risks, ABT shares many risks in common with its healthcare peers. First, ABT and its competitors face the challenge of navigating the ever-evolving regulatory landscape for drugs and medical devices. Regulatory hurdles can delay product approvals and hinder revenue growth (e.g., FDA regulations). In addition, both ABT and its peers must contend with continued pressure on healthcare costs, which is not only a business issue but also often viewed as a sensitive political issue. Such pressure can lead to price controls and reduced reimbursements.

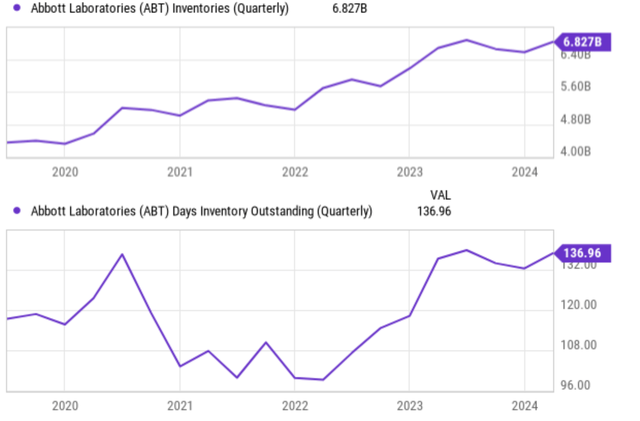

Although we see some risks more specific to ABT. The first involves continued weakness in the diagnostics sector, where sales continue to be hurt by declining demand for Abbott’s COVID-19 test kits. Longer term, we view this as only a temporary headwind and something to expect. We assume that no investors seriously expected demand to continue at the levels seen during the pandemic. Inventories are another sign of concern as you can see from the chart below both in terms of dollar amount and also days of inventory outstanding. Such high inventory can add cost pressure and balance sheet risk in the near term.

Seeking alpha

Finally, our verdict is that the pros outweigh the cons. We view ABT as a compelling opportunity for investors looking for long-term total returns. Analysts expect a steady rise in earnings per share at a CAGR of more than 10% for the coming years. We agree with this strong forecast, considering its diversified business model and strong pipeline of new products. Furthermore, ABT’s current P/E ratio is below its historical average by a good margin, suggesting that the stock may be undervalued. This combination of strong growth potential, high return on equity (ROCE), and discounted valuation positions ABT well for market-beating returns.