JHVEPhoto/iStock Editorial via Getty Images

Investment thesis

Air products and chemicals (New York Stock Exchange: ABD) is a good choice for investors looking for low volatility and strong earnings growth. As a leading player in its industry, the company is poised to capitalize Favorable secular trends. The company’s long-term performance is exceptional, as is management’s approach to capital allocation. The company consistently achieves a strong return on invested capital and has several multi-billion dollar projects in the pipeline with a high target internal rate of return. The compound annual growth rate of earnings for the past decade has been 10%, which is another reason to buy the stock. My valuation analysis indicates that the stock is undervalued by about 10%, making it a ‘buy’.

APD’s latest earnings presentation

company information

Air Products and Chemicals Inc. It is the world’s leading producer of industrial gases. In addition, APD is the world’s leading supplier of LNG processing technology And equipment.

APD’s latest earnings presentation

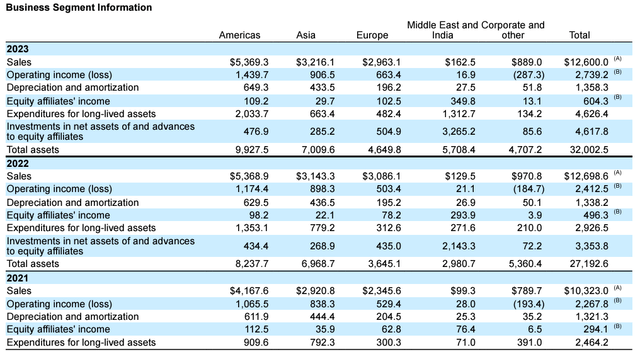

The company’s fiscal year ends on September 30. APD’s sectors are divided by geographic regions: Americas, Asia, Europe, Middle East, India and Corporate. The Americas represent 42% of total revenues for fiscal 2023.

APD’s latest 10-K report

Finance

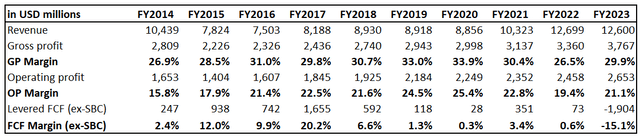

APD is a new company to me. Therefore, I start by looking at long-term trends in financial performance. Revenues have grown at a compound annual growth rate of 2.1% over the past decade, in line with long-term average inflation. Despite modest revenue growth, APD showed strong improvement in operating margin, from 15.8% in FY14 to 21.1% in FY2023.

Author’s calculations

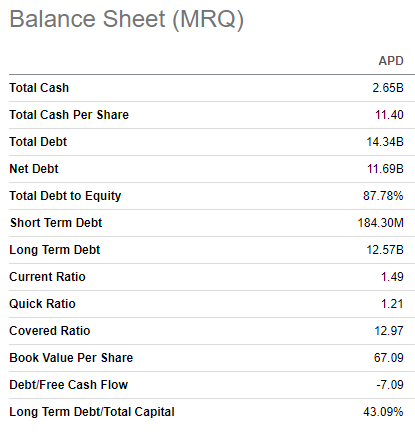

The free cash flow (FCF) margin has been consistently positive, except for fiscal 2023 when the company boosted capital expenditures. Despite the capital-intensive nature of the business with shallow and slow revenue growth, APD has an excellent record of dividend consistency. Overall, I consider management’s approach to capital allocation to be sound because it successfully balances investing in capital projects, paying dividends, and maintaining a healthy balance sheet. APD has an “A” credit rating from S&P Global Ratings.

Seeking alpha

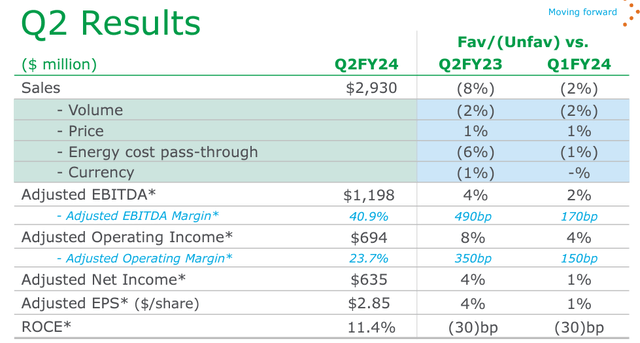

The most recent quarterly earnings were released on April 30, when APD missed revenue and EPS consensus estimates. Although revenue declined 8.4% year-over-year, adjusted EPS expanded from $2.74 to $2.85. This is because the revenue decline is mostly explained by the 12% decline in energy costs across the Americas. The company reiterated its full-year guidance during the earnings call.

APD’s latest earnings presentation

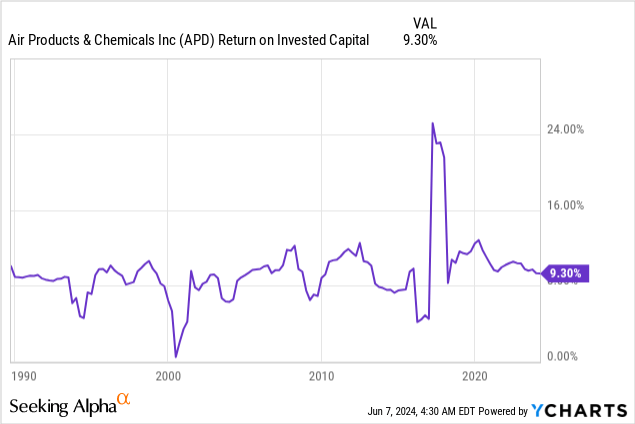

In my opinion, APD’s first core strength is its track record of consistently delivering a strong return on invested capital (ROIC). To finance new capital projects, the company relies mostly on debt financing. The company’s interest expenses in fiscal year 2023 were approximately $178 million, while the total debt balance at the beginning of the year was $8.4 billion. This means that on average a company’s cost of debt is about 2.2%. This is several times lower than APD’s ROI, meaning the difference creates value for shareholders.

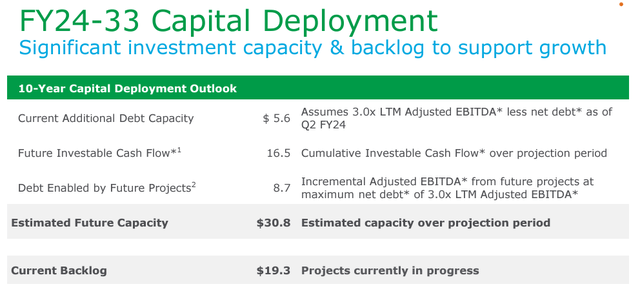

Therefore, the strong accumulation of the APD project appears to be a bullish signal. The company’s deployment capital capacity for FY 2024-2033 is US$30.8 billion, and there are projects currently underway worth US$19.3 billion.

APD’s latest earnings presentation

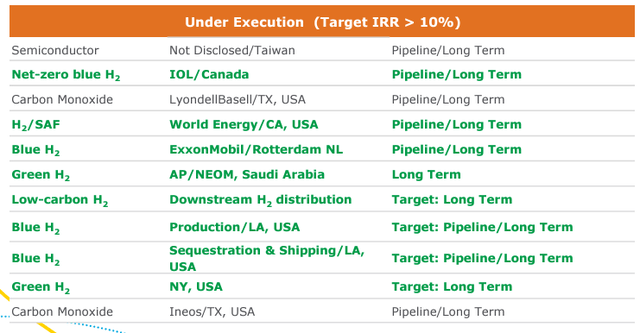

The targeted IRR for these projects exceeds 10%, an aggressive target that appears achievable given APD’s continued strong ROI. All projects are long-term contracts with world-class counterparties. The largest project is the Jazan project in Saudi Arabia, a $12 billion air separation unit.

APD’s latest earnings presentation

Another reason for optimism is that industry trends are expected to be positive for APD. Polaris Market Research report indicates that the global industrial gases market will witness a CAGR of 7.1%. These are strong tailwinds behind APD’s back, which also increases my optimism.

Since APD is the world’s leading supplier of LNG processing technology and equipment, we should also know what experts predict about growth in global LNG projects. According to Shell LNG Forecast 2024, global demand for LNG is expected to rise by more than 50% by 2040. This means that global LNG capacity will need to expand, and experts expect capacity to grow by 40% by 2030. This is another strong secular tailwind for APD.

evaluation

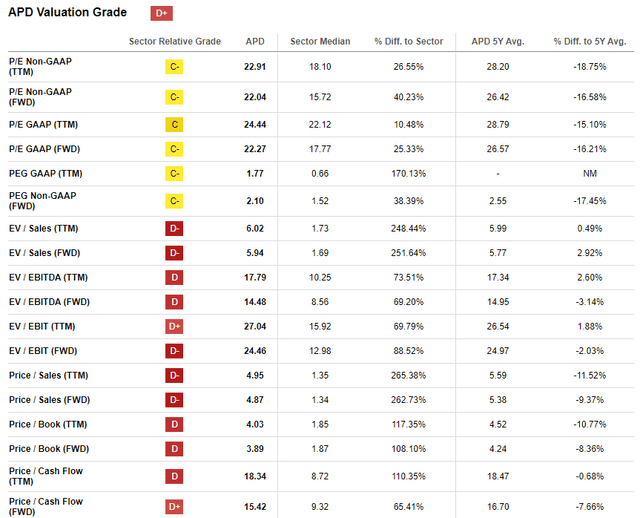

The share price is down 3% over the past 12 months and 1.5% since the beginning of the year. Seeking Alpha Quant assigns APD a low rating grade of “D+” because its multiples are higher than the sector average across the board. On the other hand, APD is the industry leader and is likely worth the premium. Therefore, it is best to evaluate valuation by comparing current multiples to the company’s historical averages. From this perspective, APD looks attractively valuable.

Seeking alpha

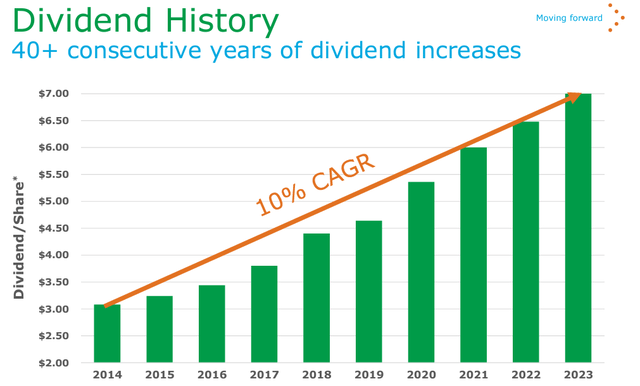

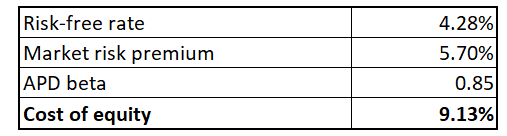

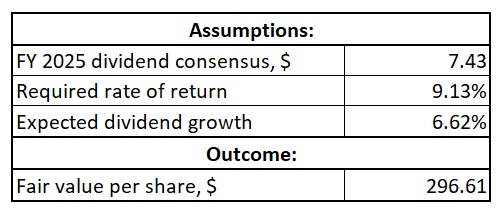

APD has raised its dividend every year for over 40 years, which means valuing the stock using the dividend discount model (DDM) is a reliable option. The cost of equity is the required discount rate for this approach, which is 9.13%. I calculated this number using the CAPM approach and all input data are publicly available.

Author’s calculations

I calculate a target price for the next twelve months. Therefore, using the next fiscal year’s expected dividend of $7.43 would be correct. APD’s earnings growth over the past five years is higher than the discount rate, which would not make sense for the DDM formula. I have to use another growth rate and the average growth of the sector over the past five years seems like a sound choice to me.

Author’s calculations

With a slight upside, the fair price for APD stock is $300. This represents 10% upside potential, which is attractive in my opinion.

Risks to consider

APD is not a good investment option for investors looking for rapid growth. The stock has had a price increase of 140% over the past 10 years, an annual return of 9.2%. This is slower than the 10.5% annualized return of the S&P 500 (SPX) over the same period. It is a good investment for those looking for a low volatility option with ever-increasing profits. But it will likely be boring for someone seeking solid growth.

From a business perspective, demand for industrial gases is highly dependent on global economic activity. Although the near-term outlook for the global economy is positive, changes in macroeconomic cycles are inevitable. On the other hand, downside risks are limited by the terms of receipt or payment and pass-through of the cost.

Operating production facilities also involves significant environmental and operational risks.

minimum

In conclusion, APD is a “buy” for investors seeking consistent growth and limited volatility. The forward dividend yield of 2.6% isn’t high, but the company has a track record of earnings growth, which is another strong reason to buy for long-term investors.