Evening pictures

At the beginning of February of this year, I wrote an extensive article on this topic Altria Group, Inc (New York Stock Exchange: MO) – “Altria: The demise of this dividend king is overstated, and I’m betting big now.”

As the title suggests, provided There are several reasons why I bought MO, making it one of the biggest bargains in my portfolio. The basic essence of the buying thesis boils down to a combination of the following factors:

- Juicy dividend yield, which at the time amounted to ~9.1%

- Low valuations where the P/CF multiple was just under 9x.

- Consistent EBITDA growth since 2022.

- Very strong capital structure – for example, interest coverage ratio above 10x and net debt to EBITDA below 1.9x.

- The cash flow payout ratio is around 60%, leaving huge amounts of cash on the books enabling MO to de-risk further balance sheet, buy back shares, or continue to increase dividends.

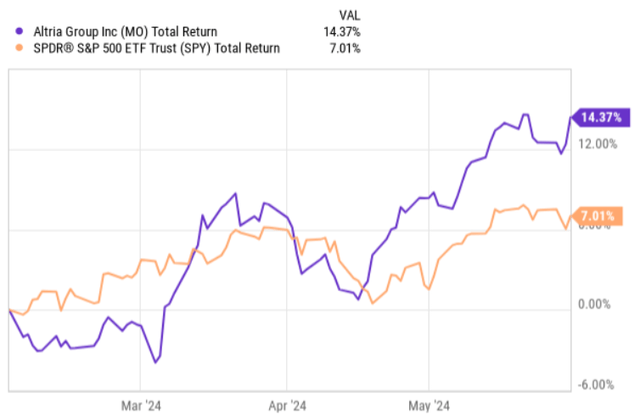

So far, after publishing my bullish thesis, Altria has clearly outperformed the market, posting strong total return performance.

YCharts

One consequence of this kind of stock price rally is a decline in the dividend yield of about 150 basis points, and in theory, one could question whether there is still good upside for MO to achieve.

Let me know why, in my opinion, Altria remains a strong buy and why I continue to reinvest and add more capital to the current position.

Dissertation review

The answer to why MO should continue to be a buy lies in the details of its Q1 2024 earnings report. In short, the new data points emerging from this report fully justify the recent increase in MO’s stock price.

The key sector that is set to drive MO growth and offset the structural decline in the traditional cigarette business going forward is NJOY. In the first quarter, MO continued to record new distribution channels, which have now crossed the 80,000 store mark. Management expects to end 2024 with 100,000 stores.

There are two nuances that are worth putting in the context of the growing number of stores:

- Over 70% of contract shops chose to select NJOY Premium Site, with the majority of required fixture resets not yet performed. These investments are expected to be implemented during the first half of 2024, thus boosting sales (by enhancing product visibility) further than the levels achieved so far.

- MO is still in the process of rolling out NJOY’s first large-scale retail visibility/commerce program, which should provide additional incentive for NJOY.

On top of these positive dynamics, which clearly support the growth potential here, MO has already made decent progress on the current score. NJOY’s retail share has continued to advance for several consecutive quarters. For example, NJOY’s retail stake was 4.3%, which translates to an increase of 0.6% (which is a meaningful rate of change considering the underlying value/share level).

Another positive factor to emphasize is some encouraging signs on the broader side of the policy-making process. And in a recent earnings call, Baillie Gifford – the CEO – gave some nice color in this context

We still have a lot of work to do as we saw some encouraging action in the first quarter. In the first quarter alone, the U.S. Food and Drug Administration, in cooperation with U.S. Customs and Border Protection, issued more than 450 vaping-related import denials, up from 348 during all of last year. The agency also continued to impose civil monetary penalties and send warning letters to manufacturers, retailers, and wholesalers of illicit products.

Besides NJOY’s excellent growth trajectory, the other two segments of MO have also performed fairly well. The oral tobacco category grew by 4.6% in terms of UBI generation. Adjusted OCI margin also came in slightly better than in the previous quarter – expanding by 0.2%. However, the cigarette category, as expected, continued to record a decline in volumes (for example, adjusted cigarette volumes decreased by 10% in the first quarter). However, what helped offset the negative impact of the sharp decline in volumes sold was MO’s pricing policy, achieving a net price of 8.5%, much higher than the Q4 2023 statistics of 5.5%. Therefore, the net effect of the decline in the smokables category was not significant and in the context of strong performances in the NJOY and the oral tobacco end, overall results were at strong levels (i.e. a slight decline, which is explained by the seasonality factor). .

As a result of strong momentum in growth sectors in member countries, management has revised guidance by increasing the bottom line for 2024 by 1%.

If we look at the capital allocation front, the balance sheet remains strong at a debt-to-EBITDA ratio of 2.1x. In addition, since MO was able to monetize a portion of its stake in ABI, stock buybacks were very noticeable during the quarter. Additionally, MO expanded its stock repurchase program to $3.4 billion from $2.4 billion already implemented under the accelerated stock repurchase program. Also, because its cash payout ratio is so conservative, MO was able to use a portion of the retained cash on further debt reduction activities, as it retired $1.1 billion of notes that matured in the first quarter.

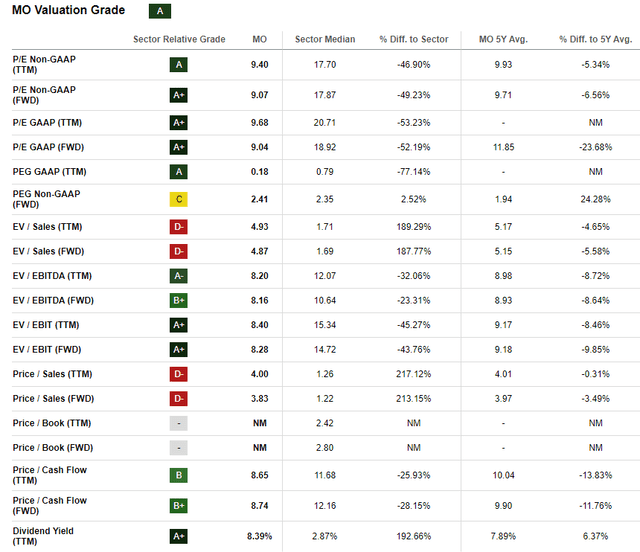

Finally, despite the stock’s recent rally, MO’s valuations still look attractive across the board, with FWD P/CF remaining at 8.7x.

Seeking alpha

Bottom line

The results of the first quarter of 2024 clearly confirm the attractiveness of MO’s investment case. Based on current fundamentals and financial performance, in my opinion, there is a sufficient data basis to conclude that MO is not only about high yield, but also about a strong upside as well.

From a net dividend investor’s perspective, the stock is very attractive as the current yield is still attractive enough at around 8.4% and is backed by a strong balance sheet and stable cash flows.

However, the growth aspect of MO is also present as we can infer from the fact that MO retains around 40% of its cash generation, which can be directed towards increased share buybacks, debt reduction or organic growth opportunities. It is also encouraging to see that NJOY is gaining the right momentum and that its cash flow profile remains strong despite the multiple, which at these levels is typically associated with either highly speculative businesses or companies, experiencing lower cash generation.

As a result, Altria remains one of my favorite dividend stocks.