Justin Baggett

summary

Following my coverage of Altus Power (New York Stock Exchange: Amp) on Sep 23, for which I recommended a Buy rating given my expectation that AMPS can easily meet its 2H23 guidance, this post is intended to provide an update on My thoughts on business and stocks. After my post on September 23, the stock price rose to a high of $7.28 (close to my previous stock price target of $8.21), but fell horribly to $4.06. At the current valuation, I believe there is another opportunity for investors to achieve upside returns. I still recommend a Buy rating for AMPS, as I expect the company to continue to benefit from this challenging macro situation and rising electricity demand in the coming decades.

Investment thesis

On 09/05/2024, AMPS released its Q1 2024 earnings, which saw revenue of $40.7 million and pro forma EBITDA of $19.7 million (which means EBITDA margin of 48.5%. The low EBITDA margin compared to the typical AMPS range of up to 50% should not be a concern, as the first quarter saw a decline in revenue due to seasonality. In terms of assets, AMPS’ operating asset portfolio reached 981 MW at the end of the first quarter, an increase of 85 MW sequentially and 303 MW during the first quarter of 2023, implying 45% growth year-on-year. The 85 MW increase is driven by contributions from Vitol acquisition (which contributed 84 MW).

The market does not seem to appreciate that AMPS strongly benefits from the current macro-environmental dynamism in two ways. First, rising interest rates and the inflationary environment put significant pressure on consumers’ purchasing power. As such, every dollar of savings they can make becomes more important, and this is where AMPS shines. AMPS’s business model leverages underutilized rooftop solar space to access the community solar market, benefiting customers by reducing their utility bills. AMPS’s strategy is to sell the additional energy it generates from the rooftop solar panels of its commercial and industrial customers to customers residing in surrounding areas. For example, an AMPS customer’s energy consumption may only require a 5-MW system, even though the customer’s rooftop area is sufficient to support a 10-MW solar array. By building the additional 5 MW of capacity, AMPS will be able to sell surplus electricity to residents of the neighboring community at a cheaper price than the residents would pay (i.e., cheaper than the prevailing price). As such, I expect AMPS to continue to see a strong adoption rate, as the value proposition to consumers is huge. To give an idea of how strong demand is, in the first quarter of 2024, AMPS increased the number of community solar customers by 20%, from 20,000 to 24,000.

We also now serve more than 24,000 community solar customers, an increase of 4,000 residential customers during the first quarter who now sign up for our solar utilities and receive the benefits of discounts on their local utility bills. First quarter 2024 earnings results call

Second, the high interest rate environment has depressed asset prices, making it cheaper to acquire AMPS. As a result of high capital costs, which limit their ability to build, many developers are withdrawing from the market, and asset owners are selling their investment portfolios, as management indicated during the last investor day. This benefits AMPS in two ways: (1) it provides more opportunities for AMPS to acquire assets, and (2) since asset owners are “forced” out due to the rising price environment, AMPS has strong negotiating power to demand a cheaper price. evaluation. Most importantly, I believe AMPS has become a preferred buyer because it is aware of practically every possible portfolio transaction in this space. This means that all vendors have searched for AMPS. Most importantly, I believe AMPS has become a preferred buyer because it is aware of practically every possible portfolio transaction in this space. This means that all vendors have searched for AMPS.

The reason AMPS has a strong position in the M&A arena is because of its important partners, Blackstone and CBRE, who have a long history with AMPS. This partnership has strong strategic benefits. CBRE helps “distribute” AMPS products to a large client base by integrating AMPS into CBRE’s client base and broader offerings. Essentially, AMPS does not need to worry about acquiring clients because CBRE has a massive presence in commercial markets. The main question is whether AMPS has sufficient financial capacity to undertake these mergers and acquisitions, and the answer is yes. The other partner, Blackstone, anchors AMPS’s balance sheet. Blackstone has invested nearly $1 billion in AMPS to date and plans to continue to fund future growth, they said at their investor day. As such, I see the continued backing and support of CBRE and Blackstone as a strong competitive advantage that AMPS has over its smaller scale peers.

Ampere Ampere

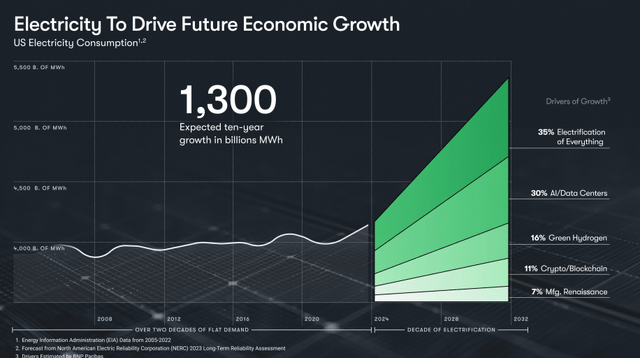

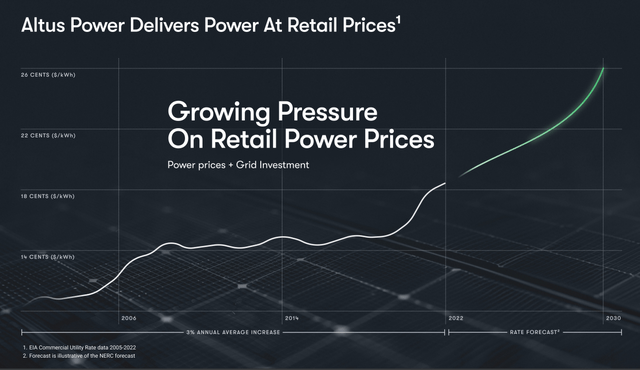

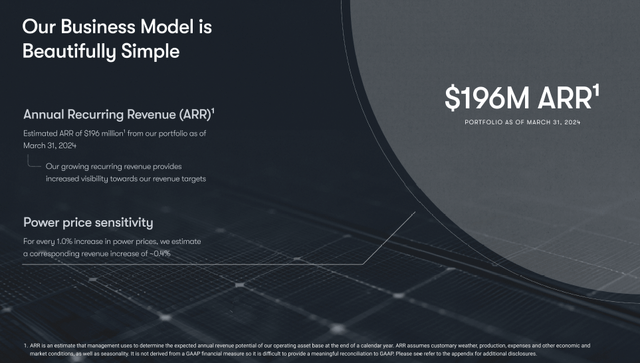

Finally, I believe we have reached an inflection point where electricity consumption will rise significantly in the coming years or decades due to factors such as adoption of artificial intelligence, demand for clean energy, etc. AMPS benefits from the increase in long-term electricity demand And Increase in utility rates in the near to medium term, as I expect demand for electricity to outpace the increase in supply. Due to the high fixed cost nature of AMPS, increases in utility rates have a high additional margin for AMP. According to AMPS, every 1% increase in energy prices results in a 0.4% increase in revenue, and I believe that 0.4% flows almost 100% to the bottom line as there is almost no additional cost associated.

Ampere

evaluation

Using AMPS’ 3-year (FY26) financial projections, I believe AMPS is worth much more than it is trading for today.

FY26 forecasts expect AMPS to generate $288 million in revenue and $170 million in earnings before interest, taxes, depreciation and amortization (EBITDA). While this guidance was lower than my previous model forecast (I expected FY25 to generate $392 million in revenue and $239 million in EBITDA), I think the growth rate is still impressive (23% growth rate CAGR) compared to other peers in the power generation industry. For example, Clearway Energy is expected to grow at low-single-digit percentages, Constellation Energy’s growth is very weak, and FirstEnergy Corp. is expected to grow at mid-single-digit percentages.

The growth in EBITDA should translate into higher EPS growth, as AMPS has a lot of leverage due to the debt it has. As of Q1 2024, AMPS’s net debt is approximately $1.13 billion (or 12 times net debt to LTM adj EBITDA).

As for valuation, I think AMPS is worth trading at a premium to these peers (on average, the three peers I mentioned above trade at ~13x EBITDA). Assuming AMPS trades at a 1x premium, at 14x forward EBITDA (AMPS traded at this level 3 months ago), the business has an enterprise value of ~$2.38B, which translates to a share price of $7.75 (vs current price) of $4.06 ).

risk

A further increase in interest rates may cause investors to assign a higher discount rate to AMPS, negatively impacting the stock’s valuation. Also, while AMPS has the backing of Blackstone, there may be times when AMPS needs to raise capital (say Blackstone decides to limit its funding), and this may negatively impact AMPS’s ability to grow, or existing investors may be diluted by raises New capital.

Conclusion

In conclusion, my rating for AMPS is a Buy rating. AMPS benefits from strong tailwinds such as rising electricity demand, and also offers a strong value proposition to consumers against the current macro backdrop. Notably, AMPS’s strategic partnerships with Blackstone and CBRE position it for future growth through accretive acquisitions. While FY26 guidance is lower than my initial expectations, the projected growth is much better than the industry’s expected growth. Therefore, at the current valuation, I see great opportunity for upside.