Lorado/E+ via Getty Images

Thesis summary

When it comes to AI and GPUs, Nvidia company (NVDA) continues to dominate the market. However, its peers in the sector continue to try to update their own products to compete with Nvidia and participate in Narrating the exponential growth of artificial intelligence.

Nvidia’s closest competitor is… Advanced Micro Devices Company (Nasdaq: AMD), which also offers GPUs for data centers.

A close second point, although this may be a moot point, is Intel Corporation (INTC), which is not only looking to expand its AI footprint, but is also pursuing another revenue avenue, namely chip manufacturing.

In today’s article, I take a look at how these two tech giants compare to each other. What is better to counter Nvidia? And perhaps more importantly, what is the best investment today?

Business overview

Both AMD and Intel have diverse sources of income. here Breakdown of AMD’s revenue sources:

AMD Revenue Breakdown (Statista)

As we can see, a large portion of revenue comes from data centers, but the fastest-growing segment in recent quarters has actually been client, which refers to revenue from CPUs, desktop components, and electronic devices.

INTC Revenue Distribution (Statista)

Intel changed the way it segments its revenue in 2021. Most of its revenue comes from client, data center, AI, network, and edge.

In this regard, AMD and INTC are competing very directly with each other for the CPU market, while both are trying to capture more of the growing data center market.

Intel has just released a new processor, the Intel Xeon 6, which it announced will be priced much lower than its peers.

Meanwhile, AMD has now released the X870(E) chipset and MI325X accelerator, as well as several other updates and a very robust product roadmap.

AMD Roadmap (AMD)

On the other hand, Intel is also trying to enter the AM market, with plans to open manufacturing plants in the US and Europe. The company just signed an $11 billion deal to establish a fab factory in Ireland.

In terms of investing, betting on AMD is a much more direct bet against Nvidia. AMD’s technology stack is much closer to Nvidia’s, while Intel is clearly lagging behind.

Intel actually has a much different strategy. First, it is trying to expand into the cool market, and in particular, it now appears to be trying to make up the difference in AI chips by undercutting its counterparts.

Profitability

Next, let’s compare the past, current and potential future profitability of these two chip stocks.

AMD Profit Margins (Macrotrends)

As we can see, AMD has struggled to turn a profit in the past, although it has seen a significantly better trend since 2016, especially if we look at gross profit margin.

INTC profit margins (Macrotrends)

Meanwhile, Intel is on the other side of the spectrum. It has always been very profitable, but that has changed in the last few years and there has been a general downward trend since 2012 in gross margin.

Intel’s move into manufacturers changes things dramatically. However, I recently analyzed Intel and concluded that a 30% operating margin is possible.

I also expect AMD’s margins to improve from here as they capture some of the high-end GPU market. However, it is clear in my opinion that Intel has a huge role to play in profitability.

growth

Now let’s take a quick look at the growth estimates.

AMD Analyst Estimates (SA)

Starting with AMD, we can see that analysts have fairly strong growth forecasts. Revenue is expected to grow more than 27% in 2025. Meanwhile, earnings per share are expected to double in the next two years.

INTC Analyst Estimates (SA)

Meanwhile, Intel is looking to hit the bottom in terms of EPS this year, thus giving us some very strong growth. More than double by 2026. We must understand this in the context of the fact that Intel’s profits have declined significantly in the past three years.

Meanwhile, revenue growth is not stellar, but is expected to average more than 10% in 2025 and 2026.

Both stocks are expected to perform well in the next two years. AMD, as it is taking market share from NVDA, and Intel, as it is also trying to gain market share and launch its own amazing business.

Now, I will say that although the EPS growth is greater for Intel, I think analyst estimates are less reliable here. There is a lot unknown when it comes to Intel’s future path.

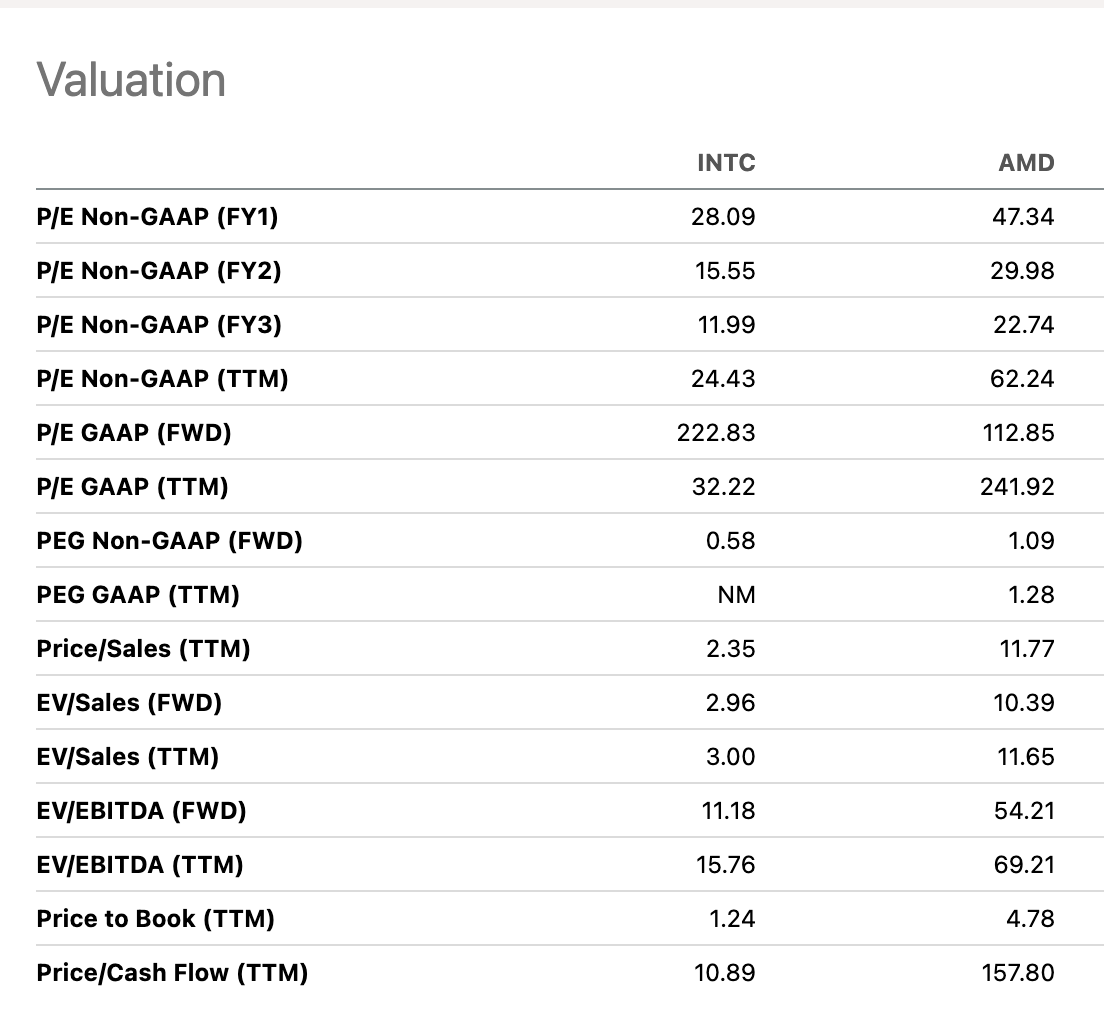

evaluation

Speaking of pricing, look at the valuation.

INTC vs AMD(SA) Evaluation

For obvious reasons, Intel’s price is much cheaper than AMD’s. But is this huge discount justified?

Even if we take into account future growth, Intel is trading at a much better price. For example, it has a forward PEG of 0.58, which is half that of AMD. The stock is also trading at half its FY1 P/E. The highlight for me is that Intel actually has a very reasonable cash flow of 10.89x.

I realize that the market seems to favor growth over value these days, but this seems like too extreme a mismatch in my view given Intel’s superior rather than inferior profitability, even though the growth outlook is more uncertain.

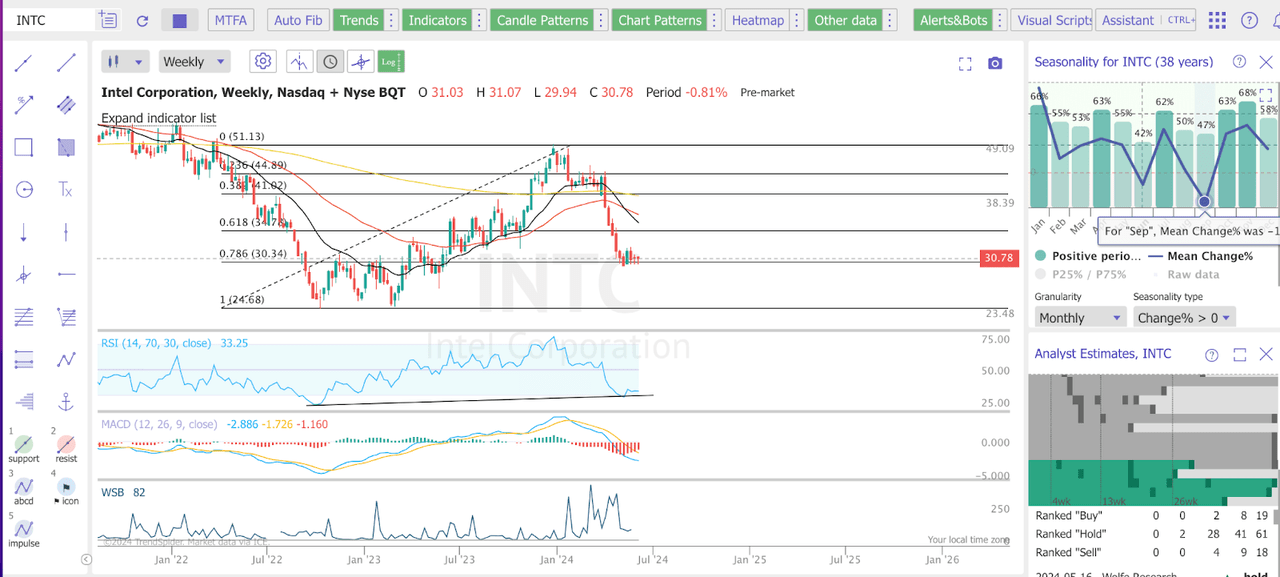

Technical Analysis

Finally, look at the charts for each stock.

INTC Chart (TrendSpider)

Intel has clear bearish momentum, with the 10-day EMA crossing below the 50-day EMA after the earnings sell-off. We are forming a base at the 78.6% retracement level, and the RSI has formed a bullish divergence.

Looking at the parts on the right, we can see that June is not a seasonally great month, with an average reversal of 0.7%, although July sees an average change of 2.6%.

Regarding analyst estimates, we have an overwhelming consensus, while the buy and sell camps are evenly split.

This chart certainly doesn’t look great, but what encourages me is the base we are forming at this major fiber level.

AMD Chart (TrendSpider)

AMD is showing significant momentum, as it is bouncing off the 50-day moving average. The RSI is neutral, and the weekly MACD is trending higher.

Seasonal data shows that June and July are generally bad months for AMD, with the average change in the stock being around negative 1%.

Finally, the analyst consensus is overwhelmingly a buy for this stock.

While we could get a retest of the 50 day EMA, this has some clear bullish momentum, and I would not be surprised to see new highs soon.

What is the best buy?

Ultimately, determining which purchase is best depends on an individual’s risk profile and investment style. Intel certainly offers a more reasonable valuation, and the potential turnaround could really surprise the market if executed well, something that, to be fair, Intel has not been able to manage in the past 10 years.

However, AMD has a much clearer growth-driven story and momentum will push this thing higher.

AMD certainly looks better for short-term trading, while I think Intel is better suited for a more conservative, long-term investment approach. At this point, though, I would rate both as Buy.