American Eagle Outfitters Q1: Visible margin headwinds with unattractive risk/reward (AEO)

Tony Anderson/DigitalVision via Getty Images

summary

Following my coverage of American Eagle Outfitters (New York Stock Exchange: AEO) on March 24, which I downgraded to a Hold rating Since the valuation is no longer attractive and AEO is unlikely to meet FY26 guidance, this post is to provide An update on my thoughts on business and stocks. I remain neutral on AEO despite the positive surprise in headline performance, as I am concerned about upcoming overall headwinds and increased per-store operating costs. Also the risk/reward at the current price is not attractive enough.

Investment thesis

On 05/29/2024, AEO released its Q1 2024 earnings, which saw revenue of $1.144 billion, just below consensus expectations of $1.153 billion. On a growth basis, revenue increased 5.8%, 90 basis points below expectations, driven mainly by 7% growth in same-store sales. Gross profit was seen at $464 million (40.6% gross margin), which beat consensus on an absolute ($456 million) and margin basis (39.6%). As a result, the EBIT margin also increases It beat expectations by 50 basis points at 6.8% versus 6.3%. Overall, EPS was seen at $0.34, $0.06 higher than the consensus.

Private account

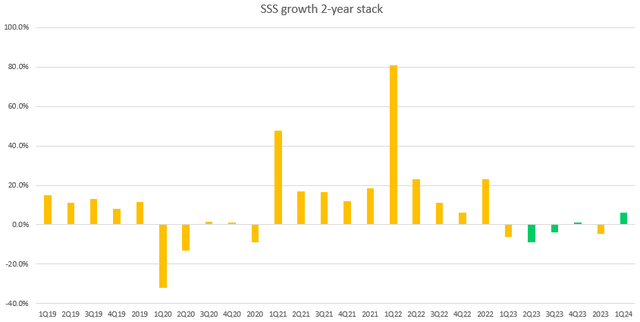

I view AEO’s Q1 2024 results as a mix of positives and negatives. On the positive side, SSS’s performance surprised me on the upside. Specifically, SSS accelerated on a two-year stack basis for the fourth consecutive quarter, and Q1 2024 saw 500 basis points of sequential acceleration. This was a really strong performance when we take into account the weak macroeconomic environment. Most importantly, power was driven by both flags.

The American Eagle (AE) brand saw SSS growth in 1Q24 of 7%, an acceleration from 6% in 4Q23. On a two-year stack basis, SSS growth accelerated significantly sequentially by 600 basis points to 3% (from -3% in Q4 2023). Execution has been on point for this brand as consumers have responded very well to AE’s launch of: (1) new social casual wear; and (2) the AE 24/7 Activewear collection.

Aerie Brand saw SSS growth of 6% in Q1 2024. While this was a deceleration compared to Q4 2023’s 13%, actual SSS performance excluding the impact of weather would have been 11%. Which means that SSS growth over the 2-year cohort would have remained in the low teens range; In fact, that would have been an acceleration from the 2023 Q4 total of 11%, and I would consider this a very positive performance given the inflationary environment. Similar to AE, management continues to get it right when identifying consumer preferences, with Aerie seeing strong customer response to new styles in softwear and activewear, continued traction with new fabrics in underwear, and strength in offline sports bras and leggings.

At this rate of SSS growth momentum, it is increasingly likely that AEO will be able to achieve at least mid-single digit aggregate growth if macro conditions do not worsen (my bullish case previously predicted 5% growth).

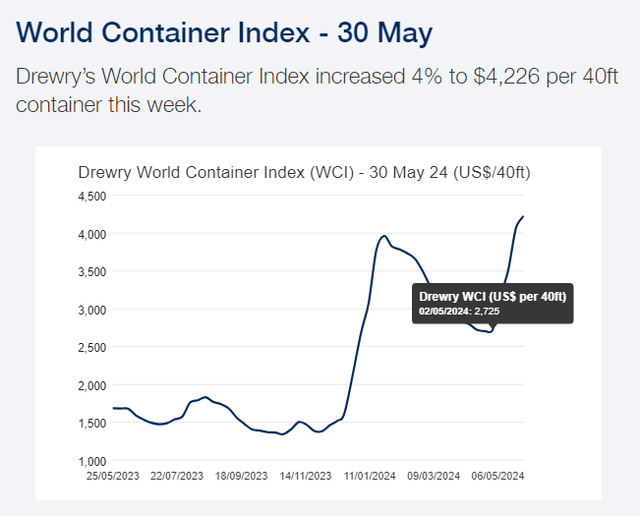

On the negative side, 1Q24 results make me feel more uncertain about the likelihood of AEO achieving EBIT margin in FY24. Remember, this was a 3-year target set by management in FY21 (to be achieved in FY24) but was delayed by 3 years (now expected to be achieved by FY26). Although I give management credit for getting gross margin back over 40% (a level it has barely surpassed over the past 12 years; the other times were in 3Q23 and 1Q-3Q21), I still find it hard to believe that they can maintain a gross margin of over 40% given that the cost of shipping is so high (the last price recorded on May 30 was almost 30% higher than the Q1 2024 average) that is well above levels 2023. Remember in my previous post, I noted that a large portion of the EBIT margin improvement between FY20 and FY24 was due to the sharp increase in gross margin, and if we remove the coronavirus lockdown and the period of pent-up demand post-coronavirus in the year FY21, the most significant gross margin gain was in FY23 (FY22 gross margin: 35% vs. FY2023 of 38.7%), which saw freight costs rise to more than half of current run rate levels.

Drewry

Based on the above, AEO is in a position where:

- The demand trend remains positive, but my fear is that the macro situation is still negative, and AEO is a company that is at the mercy of macro cycles. As prices remain higher for longer and are likely to rise again, discretionary spending is sure to be affected, and the AEO is likely to see a decline in demand.

- Gross margin faces significant freight cost headwinds (this was not reflected in Q1 2024 results, as it only really started to reflect in May).

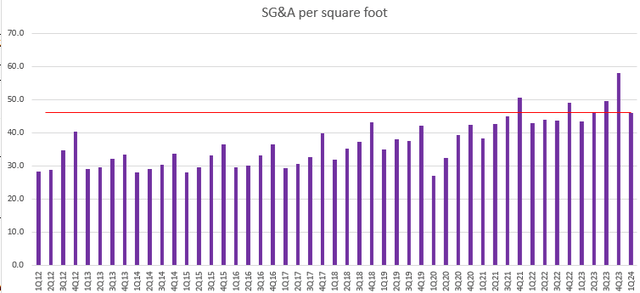

Adding the two together paints a somewhat negative outlook for gross profit performance. This, coupled with the fact that SG&A per square foot continues to rise, with Q1 2024 marking the highest Q1 level over the past decade (with SG&A expected to continue to grow in mid-single digits in Q2 2024), makes It’s hard to believe that AEO can achieve FY2024 EBITDA margin of 8.5% at the midpoint (140 basis points expansion versus FY2023).

Private account

evaluation

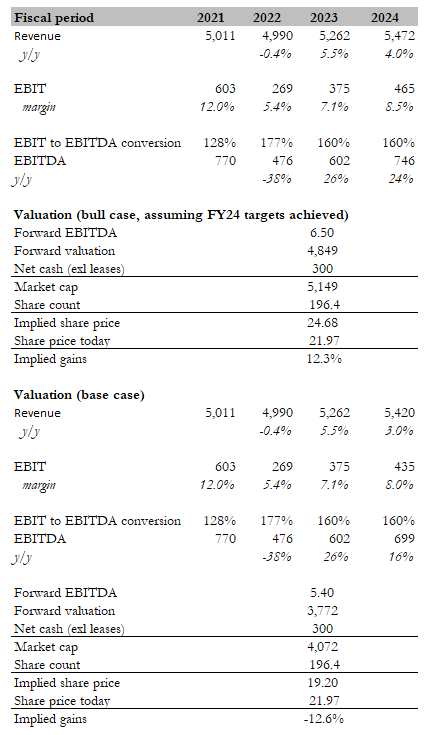

In my previous post, I discussed different scenarios for AEO in the medium term, with a focus on whether it can achieve FY2026 targets. I won’t repeat everything here. Instead, I’m shifting focus to the near term (FY2024), where I see the possibility that AEO will miss its EBIT target in FY2024.

Private account

My base case target price for AEO is $19.20 and around $25 in the bull case. My bullish case assumes that everything is going well when AEO achieves the high end of its FY24 growth and EBITDA guidance, and that the stock is trading at the upper end (+1 standard deviation) of its historical EBITDA range. All of this translates to a 12% upside.

However, as I mentioned above, I think this is too optimistic. I agree that TSR growth has a high chance of meeting the midpoint of FY24 guidance, given that 1Q24 was very strong, and the next series of marketing campaigns should support at least lower TSR growth. But I am more pessimistic about the EBIT margin expansion outlook. I believe total margin headwinds and increases in SG&A per square foot will hurt AEO’s ability to expand margins. Also, the FY2024 EBIT margin target assumes another year meaning that FY2024 will be the second year of consecutive EBIT margin expansion, a phenomenon that has occurred only once over the past decade, in FY15 and FY2024. Fiscal 2016, which averaged about 130 basis points on average per year. year. Assuming the same thing happens again (FY23 and FY24 expansion will average about 130 basis points per year), this would imply FY24 margin expansion of about 90 basis points, and FY24 EBIT margin of 8%. . In the base case, AEO should trade at its historical EBITDA multiple, which translates into a target share price of $19.20, or roughly 13% downside.

Given that the risk/reward ratio is 1:1 and that headwinds are more visible and easier to track than tailwinds (i.e. improved sales from marketing campaigns), I don’t think the risk/reward situation is attractive enough.

Conclusion

In conclusion, my review of AEO remains outstanding. While the strong growth of the social security system is commendable, I am not confident enough to believe that macro conditions will not worsen, impacting demand. Furthermore, coupled with the potential increase in shipping costs and the expected increase in SG&A, there is a chance for AEO to miss its EBIT targets for FY 2024. Overall, I don’t think the current risk/reward posture is appropriate.