JHVEphoto

Ameriprise Financial (New York Stock Exchange: Amp) has an interesting profile in the financial services sector, with its growth strategy focused on the advisory and wealth management sector. This has supported its recent growth, but it appears this is already being reflected in its valuation.

Ameriprise business profile

Ameriprise Financial is a financial services company that offers many products in the industry, including mutual funds, savings, annuities, insurance, and others. It operates under a multi-brand approach, which includes Ameriprise Financial, Columbia Threadneedle Investments and RiverSource.

The company has a long history, but has only been an independent entity since 2005, when it was spun off American Express (Earn). Its current market value is about $44 billion, and its shares are traded on the New York Stock Exchange.

Its core business is wealth management and investment advisory, and operates primarily as a planning and financial services firm. the product The group is designed to meet the needs of its clients across the investment lifecycle, including cash and liquidity solutions, asset accumulation, income, protection and wealth management. It also owns a bank that provides traditional banking services to wealth management clients.

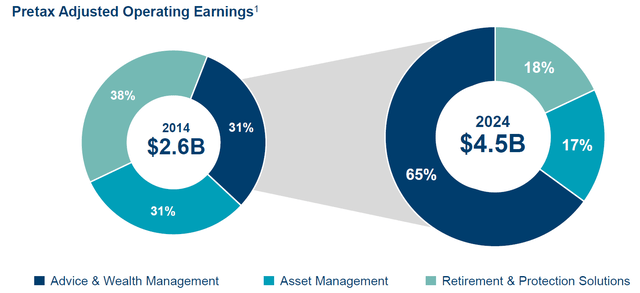

At the end of last March, it had approximately $1.4 trillion in assets under management (“AUM”) and management, and by this measure is one of the largest companies in the US financial services industry. About 86% of Ameriprise’s revenue is generated from wealth management, while asset management is responsible for the rest. Its business is divided into three main units: consulting and wealth management, which is the largest and constitutes about half of the company’s revenues, followed by retirement and protection solutions, and asset management.

Over the past few years, the company’s growth strategy has focused mainly on its wealth management business, which explains why the weight of this sector has increased significantly within the group.

Business mix (Ameriprise)

Given that wealth management has a more repetitive nature than other activities, this bodes well for a less cyclical business and better predictability of its earnings and level of profitability in the long term. This sector is mainly fee-based, accounting for about 80% of the revenue generated in this sector, which represents a positive picture for the sustainability of its business model in the long term.

In this sector, it has more than $960 billion in client assets under management or management, and has an advisor network of more than 10,000 financial advisors, who build long-term client relationships with individuals who have $100,000 or more in investable assets.

Compared to other companies in the financial services industry I’ve covered in the past, e.g T. Rowe Price (True) or Invesco (IVZ), I believe Ameriprise has a better business profile because it is less dependent on investment performance and has a more recurring revenue and earnings profile than its peers over the long term.

While the wealth and asset management industry is highly competitive and Ameriprise has no specific competitive advantage over its larger or smaller peers, its relatively large exposure to advisory and wealth management gives it an interest profile and good growth prospects for the future.

In addition, compared to its prior business mix in which Ameriprise had more exposure to insurance-related activities, its current business mix also requires less capital and has less earnings volatility, providing a more attractive investment proposition to shareholders than some years ago.

Going forward, Ameriprise’s growth strategy is not expected to change much, as it is largely focused on growing its wealth management business on an organic basis, targeting high-net-worth individuals and institutional investors. Its primary target is individuals with $0.5-5 million in investable assets and a responsible mindset, a segment that has good growth prospects and allows Ameriprise to focus on a specific type of client where it may face less competition from larger players in the wealth management industry.

This means that Ameriprise is trying to differentiate itself from other players by providing a more personalized service to a segment of the market that other players may neglect, which seems like a reasonable strategy for its long-term business sustainability and growth.

Client (Ameriprise)

This strategy has been very successful, considering that Ameriprise’s growth in the wealth management sector has been very strong over the past three years, growing client assets by 26% during this period and recording positive inflows during a difficult period for the capital markets, which is a good thing. . A very good result considering the fierce competition it faces in the industry.

Ameriprise Financial Overview

In terms of its financial performance, Ameriprise has had a positive track record, achieving revenue and earnings growth in recent years, demonstrating that its business is less tied to capital markets than some of its wealth and asset management peers.

In 2023, Ameriprise revenues rose 8% year-over-year to $15.5 billion, supported by higher assets under management, particularly in the wealth management segment, and a strong increase in net investment income related to higher interest rates. In fact, Ameriprise Bank holds securities for liquidity purposes and in the insurance sector it also has an investment portfolio, so the rising interest rate environment was positive for its net investment income, which rose to $3.2 billion in 2023 (vs. $1.4 billion in 2023). . in the previous year).

In terms of operating expenses, despite the inflationary environment, Ameriprise demonstrated good cost control with general and administrative expenses increasing 4% year over year to $3.8 billion, but there were other expenses that hurt its operating profits. The company reported expenses of $608 million related to market impact on long-term unconventional products as well as higher claims and settlement costs, which impacted reported operating results and led to an 18% year-over-year decline to $3.2 billion.

However, after adjusting for market movements and other one-time impacts, the company’s adjusted operating income rose 8% year over year to $3.1 billion, a better indicator of the strength of its underlying earnings going forward. By sector, Consulting and Wealth Management was the main driver of earnings growth as its adjusted operating profits in this sector rose to more than $2.8 billion in 2023 (vs. $2.1 billion in 2022), while other business segments recorded lower adjusted operating profits, influenced by Decreased revenues (asset management) and increased claims costs (insurance) over the past year.

During the first quarter of 2024, Ameriprise maintained positive operating momentum, reporting revenue of $4.15 billion, up 11% year-over-year supported by higher management fees and net investment income, and a 10% year-over-year decrease in total expenses. This combination of higher revenues and lower costs resulted in net income of $990 million in the quarter, nearly double the first quarter of 2023, and return on equity (excluding accumulated other comprehensive income – AOCI) was 48.1%, an improvement of 290%. Basically. Point compared to the first quarter of 2023.

By sector, advisory services and wealth management remained the main growth driver, posting adjusted operating profits of more than $2.5 billion last quarter (up 13% year-over-year), while other sectors also recorded some growth but at more modest rates.

In terms of its balance sheet, Ameriprise had a very comfortable position at the end of last quarter, given that it had excess capital of about $1.5 billion and had more than $1.9 billion in liquidity at the holding level. Given that its business is currently more exposed to recurring advisory and wealth management operations, this means that it does not need to retain much of its profits and can therefore distribute a significant portion of its organic cash flow to shareholders.

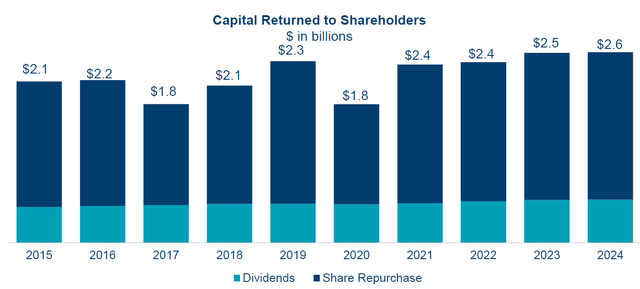

In fact, its capital return strategy has been to buy back shares and deliver increased dividends to shareholders, returning about $22 billion of capital over the past decade.

Returns on capital (Ameriprise)

As shown in the previous chart, the majority of its capital returns have been generated through share buybacks, while its dividends represent a much smaller portion of its cash outflows.

Its current quarterly dividend is $1.48 per share, or $5.92 annually, which at the current stock price yields a forward dividend yield of about 1.4%. This is a relatively low yield compared to other alternatives in the financial services sector, so Ameriprise’s income appeal is not great. However, its dividend payout ratio is only around 18%, which is very low, so its dividend is clearly sustainable and should continue on an increasing trajectory in the coming years.

In addition to dividends, over the past 12 months, the company has also bought back about $2 billion of its own stock, meaning the total dividend was about 80% of its earnings, a capital return strategy it is likely to maintain next year. . A few years.

Evaluation and risks

In terms of its valuation, Ameriprise currently trades at more than 12x forward earnings, at a premium to its historical valuation over the past five years (10.2x), which may be a sign of overvaluation.

Compared to its closest peers, Ameriprise also trades at a slight premium, considering that its relatively large peer group of asset and wealth management firms trades at about 11.7 times earnings. Consider peers who have a stronger focus for their operations in the wealth management sector, e.g Julius Baer (OTCPK:JBAXY) or Stifel Financial Company (SF), its shares also look a little overvalued, given that Julius Baer trades at just 10x earnings and Stifel at 11x.

Given that Ameriprise’s growth and profitability prospects aren’t that different from its peers, this means its shares aren’t particularly cheap right now.

In terms of risk, one important factor is competition in the industry and the potential for further concentration through mergers and acquisitions, which may create larger players that may eventually compete on pricing and lead to some future margin pressures across the industry.

Another potential risk is lower interest rates in the coming quarters, which could negatively impact its revenue growth. Ameriprise’s net investment income has risen significantly in recent quarters, but that could change if the Federal Reserve decides to start lowering interest rates in the near future, representing a potential headwind to revenue and earnings growth in the next few quarters.

Conclusion

Ameriprise’s strategy to gradually shift its business toward advisory and wealth management has been successful and gives it relatively good long-term growth prospects. However, competition in this sector is strong and Ameriprise does not appear to have any specific competitive advantage in the industry, hence growth may slow in the coming years. Its valuation is also not particularly cheap at the moment, so Ameriprise doesn’t appear to offer much value to long-term investors at the moment.