HJBC

Shares of French asset manager Amundi ( OTCPK:AMDUF ) have performed well since my editorial last September, returning more than 30% with gains in local currency terms. At the time, I claimed that its P/E ratio of about 10x was more than fair Share price. While Amundi faced idiosyncratic and industry risks, the implied high single-digit dividend yield only requires complementary low-single-digit annual growth on top, which the company should be able to achieve over time based on organically increasing assets under management (“ Ohm”).

Source: Morningstar

Amundi has started 2024 well, with buoyant markets lifting assets under management, management fees and profits. While the stock has performed strongly since initial coverage, Amundi still trades on a prior-year P/E of less than 12, implying a dividend yield of more than 6% on a well-covered payout ratio. With Amundi’s growth potential capable of achieving mid-range numbers annually, I continue to see The rating is attractive. I’m keeping my “Buy” rating in place.

Amundi Buying Status Recap

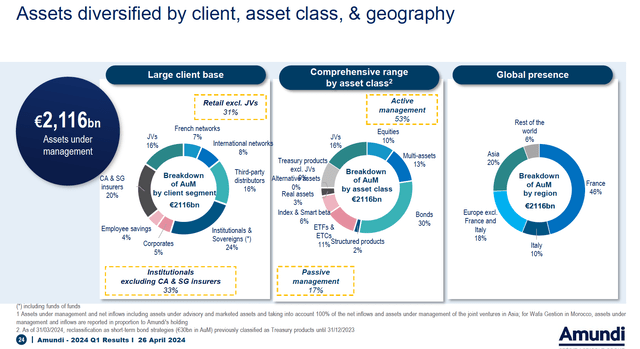

To quickly summarize, asset managers can be very good companies, since assets under management have an internal tendency to increase over time due to rising capital markets. With costs largely constant, this can translate into good long-term income growth. Amundi is one of the largest asset managers in Europe, with more than €2.1 trillion in assets under management at the end of the first quarter of 2024.

Source: Amundi results presentation for the first quarter of 2024

In addition, Amundi has some startup advantages from its relationship with some major European banking partners. This essentially means distributing its investment products, such as mutual funds, to retail clients on either exclusive or preferred terms (i.e. where the minimum volume in Amundi products must be). Note that in countries like France, the distribution of funds is largely linked to banks. This differs from the United States, for example, where customers typically purchase such products via third-party platforms such as Charles Schwab (SCHW).

Amundi has a number of distribution agreements, including with Crédit Agricole (OTCPK:CRARY)(OTCPK:CRARF), one of the largest banks in France and a majority owner of Amundi shares. As the majority owner, Crédit Agricole seems unlikely to terminate this distribution agreement, although Amundi’s agreements with other banks such as UniCredit (OTCPK:UNCRY) and Société Générale (OTCPK:SCGLY) appear more likely to be disrupted.

These retail distribution agreements represent approximately €300 billion of Amundi’s assets under management. While this may seem small relative to total assets under management of over €2 trillion, note the significant contribution of Amundi’s retail sector to the group’s revenues compared to assets under management. While the retail segment represents only about 30% of Amundi’s total assets under management, retail management fees represent about 67% of the group’s total revenue.

Source: Amundi 2023 Global Registration Document

In addition to the implied higher level of profitability, these distribution agreements represent a good source of new money flows over time. Clearly, rising assets under management is important to asset managers because of its direct correlation to fee income and therefore profits. While assets under management can naturally rise over time along with capital markets, positive net flows are also an important source of growth. Having what essentially amounts to a captive retail customer base is an advantage for Amundi in this regard.

While Amundi faces certain risks (more on that later), those risks were already reflected in its valuation last time around, with the stock trading on a P/E of around 10x. With management targeting a dividend payout ratio of at least 65%, this implies a return exceeding 6.5%, which requires only an additional 3% to 4% in long-term annual growth to achieve annual returns of more than 10% for investors. This can be achieved over time through a combination of rising assets under management and increasing cost.

good performance

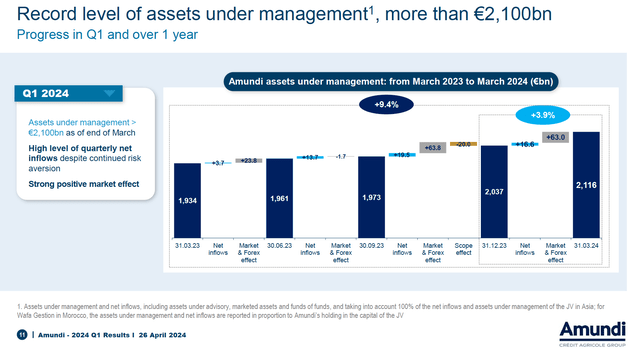

Amundi started the year well, with buoyant markets lifting assets under management, fees and profits. Assets under management amounted to €2,116 billion at the end of the first quarter, up 9.4% year-on-year and approximately 4% sequentially. While higher markets contributed the bulk of AUM growth, Amundi still recorded positive inflows, with net inflows of more than EUR 53 billion year-on-year and EUR 16.4 billion sequentially.

Source: Amundi results presentation for the first quarter of 2024

As interest rates rise, products such as money market funds have become more attractive recently. This resulted in a net inflow of €8.7 billion into treasury products in the first quarter, although Amundi also saw positive flows into both active management (€1.3 billion) and passive management (€2.5 billion). While there are other moving parts to take into account, it’s clear that management fees are closely tied to assets under management, and these fees accounted for more than 90% of Amundi’s revenue of €824 million last quarter. As assets under management rose, management fees also rose by 4% year-on-year to €766 million. Growth in assets under management has lagged, as the increase in assets under management has skewed away from riskier (and therefore higher margin) products such as equities.

Source: Amundi results presentation for the first quarter of 2024

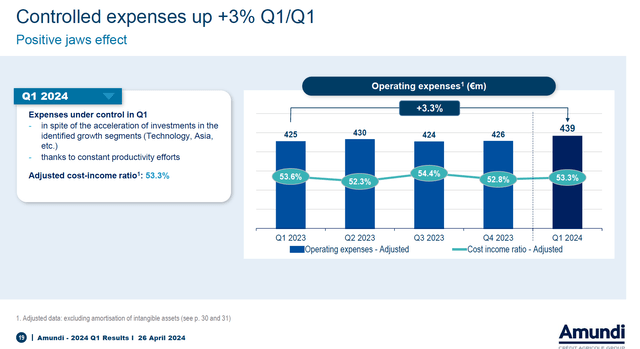

Cost leverage is a feature of asset managers. Despite the backdrop of high inflation, Amundi reported good cost control in the first quarter, with operating expenses increasing 3.3% year-on-year. This was lower than revenue growth of 3.8% year-on-year, so Amundi’s cost-to-income ratio fell by 30 basis points to 53.3%. This, in turn, has helped drive annual growth of just under 6% in net income (€318m) and earnings per share (€1.55) – which is higher than revenue growth and roughly in line with the level at which I believe the company can grow. at the long term.

Valuation remains supported by growth potential

As an industry, it is clear that asset management is quite cyclical since assets under management are closely linked to market levels. Amundi is relatively more defensively biased with equities representing less than 30% of assets under management excluding joint ventures, although cyclicality remains a feature of its business.

With this in mind, AUM growth in the first quarter fell above the level that Amundi is likely to average over the course of the cycle. Broken down into its component parts, net inflows accounted for about 3 percentage points of the year-on-year growth figure in the first quarter (9.4%, as above), with market and FX levels accounting for about 7.5 percentage points (sell note) from Lyxor’s US calculations For teams). I would suggest that net inflows were roughly in line with a reasonable estimate of their long-term growth potential (i.e. low single digits annually), while the contribution from higher markets was about 5 points higher than a reasonable estimate of their long-term trend.

All that said, I believe ~5% annual growth in assets under management and revenue is achievable for Amundi, which can be leveraged into slightly higher EPS growth due to the operating leverage inherent in the business. Amundi’s 2023 dividend per share was €4.10, representing a payout ratio of approximately 72% on its 2023 EPS of €5.71. Management policy is to pay out at least 65%, so I expect dividend growth to lag slightly behind EPS growth over the next few years as the payout ratio heads toward the 65% mark. However, with shares reaching €66.15 in Paris trading, medium-term DPS growth of 5% on a 6.2% yield implies returns of more than 11% on a fixed multiple, providing investors with double-digit annual returns.

Risks to consider

Investors in Amundi are exposed to market risk due to the inherent nature of asset management, where assets under management are intrinsically linked to capital market levels. In addition, asset managers face structural headwinds from fee margin compression, driven by a shift from active to passive investment strategies. Last year, for example, Amundi estimated that the global market share of active management fell by two points to 65%, continuing its long-term trend. Amundi has negative exposure (~21% of previous joint ventures under asset management), so it can capture a share of these flows, although this shift in the mix will still represent a headwind to margins.

In terms of unique risk, my main near-term interest is in the UniCredit distribution agreement, which runs through 2027. UniCredit is an Italian bank with pan-European operations, and is particularly sensitive to net interest income. For this reason, it is looking to boost fee income, especially now with interest rates in the eurozone falling. UniCredit also has significant levels of surplus capital, meaning it is in a position to undertake mergers and acquisitions as an acquirer. I think there’s a good chance it will choose to strengthen its asset management capabilities in this way, which could represent a headwind for Amundi. While existing UniCredit customers who own Amundi products would not become forced sellers in this scenario, this could nonetheless represent a headwind to net inflows given the potential negative impact on future growth.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.