Apartments in Mid-America: 2024 Will Be Tough, but Things Should Get Better From There (NYSE:MAA)

Alexey Iatsenko

Dear readers,

Apartment communities in Central America (New York Stock Exchange: MAA) is a high-quality apartment REIT that owns mostly Grade A acreage in the Sunbelt, has no exposure to California, and has a strong A- balance sheet rating. The REIT has a long history (13 years). Increasing dividends, CAGR of 8.8% for 5 years, yield of 4.5%. As such, it could represent an interesting way for income investors to gain a reasonably high return and exposure to a traditional asset class (i.e. residential real estate) that could benefit from a downward movement in interest rates, which seems likely. For details on my thesis on low interest rates, check out This article.

I’ve covered the MAA before, most recently in March in an article titled Lower rents coming. I discussed full-year 2023 results, which were impressive with net income growing 15% year over year – the third year in a row. With double-digit growth. But despite the good performance in the past, I downgraded the stock to Hold, because… (1) The NOI’s growth was already showing signs of slowing on a quarterly basis, and (2) The Sunbelt residential market appears likely to face significant pressure from oversupply in 2024 and 2025 that has already manifested itself in rising vacancies and declining market rents. Management even guided for an overall decline in NOI in 2024, primarily due to higher operating expenses, clearly showing that they are anticipating several tough quarters ahead.

Since my last article, the stock has performed well, returning 5.5% in about 3 months, which is somewhat higher than the 3.2% for the S&P 500 (SPX) over the same period. But recent data points (Q1 2024 results and fundamentals in the MAA market) still point to potentially disappointing results in the short and medium term. Today, I want to try to look through the hype at the stock’s long-term prospects, once the market works through the excess supply that has been delivered to the market this year.

Searching for Alpha – David Short

Short to medium term prospects (2024-2025)

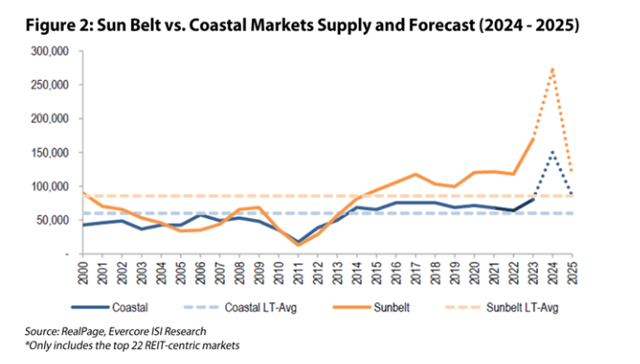

Due to the high rate of tenant turnover, MAA’s performance is closely linked to the performance of the market in which it operates. It is now known that the supply of new Class A apartment space in the Sunbelt will be high this year and next, especially compared to coastal markets. To put some numbers behind this claim, new deliveries in the Sunbelt are expected to reach 5.5% of existing inventory in 2024 alone, while the number in coastal markets is just 2.1% – in line with the (healthy) historical average.

Some markets in which MAA operates will see particularly high levels of new inventory. In particular, Austin (6.4% of ABR), Phoenix (2.9% of ABR), and Charlotte (6.2% of ABR) will see their stocks grow by approximately 15% over the next two years.

RealPage

This high supply has already impacted rents and vacancies in a meaningful way. Nationally, apartment vacancy rose to 6.7%, and some markets in the Sunbelt saw higher levels of unoccupied space. Atlanta, for example, which happens to be MAA’s largest market, has seen average vacancies rise to a 12-year high of more than 8%, and in Austin, Texas, vacancies for newly built properties are attacking the 10% mark.

All of this has translated, understandably, into additional pressure on rents that have already begun to fall. In particular, Austin was the worst performer with rents down 5.7% YoY, followed by several other MAA-exposed markets with ~2-3% declines YoY.

Costar

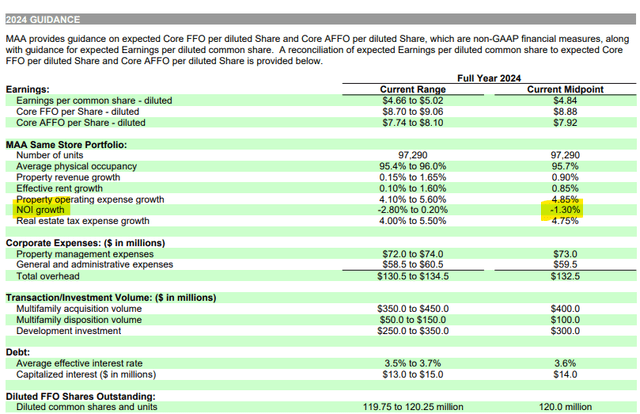

As a result of these weak fundamentals, management has been cautious in NOI guidance and is on target for negative NOI growth in 2024 of -1.3%, in line with guidance issued last quarter.

MAA Air

There’s no doubt that 2024 will be a tough year for Sunbelt REITs, especially those focused solely on the Class A space that is under much greater threat from the underbuilt Class B space. However, as long-term investors, our job is to look to the future and try to determine what might happen in 2025 and beyond. Here MAA’s prospects look much better.

Long-term forecasts (2025 and beyond)

In the long term, there is a light at the end of the tunnel for MAA and its Sunbelt peers, because… Supply will decline sharply after 2025.

We know this, because building permits, which lead deliveries by two to three years, have already declined significantly from their peak in 2021 as a result of higher construction, energy and financing costs. The truth is that developing new residential spaces is not a good business at the moment, which is why very few developers start new projects and this is unlikely to change in the near future.

Consider this example, which comes from an actual community being developed by MAA’s close counterpart, Camden Property Trust (CPT). The community will contain 410 units and is expected to cost $147 million, or $359,000 per unit. To make the project interesting to any investor, it would likely generate a return on NOI of at least 5.5% (100 basis points spread across long-term Treasuries to compensate for the risk), or an annual NOI of $19,745. With an average NOI margin of 65%, which is typical in the residential REIT space, the annual revenue required to generate this return is $30,300 or $2,530 per month. But that’s well above market rents for such properties, which average only about $2,000 a month. As a result, the project is not really worth implementing unless rents rise by at least 20-25% from current levels.

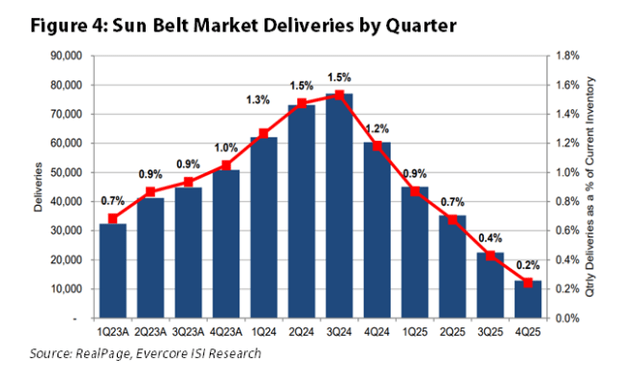

For this reason, I expect development activity to continue to decline, perhaps more so than is already evident from the building permits already issued which involve delivering just 0.2% of inventory each quarter by Q4 2025. This represents just 1% annually, and way down. From 5%+ this year.

RealPage

Moreover, besides the decrease in supply, there is also Reasons to be optimistic about future demand.

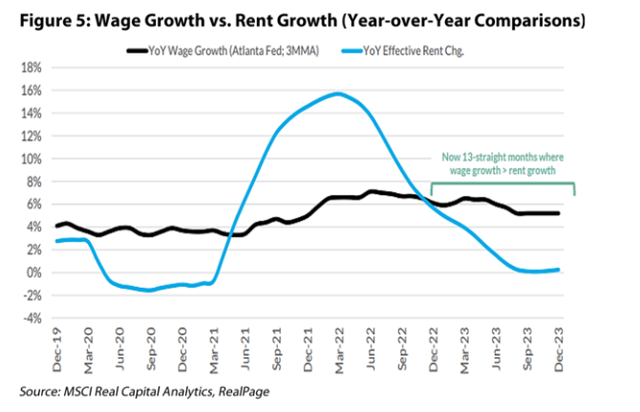

FirstlyDemand has been and is likely to continue to be supported by wage growth, which exceeds rent growth.

MSCI Real Capital Analytics

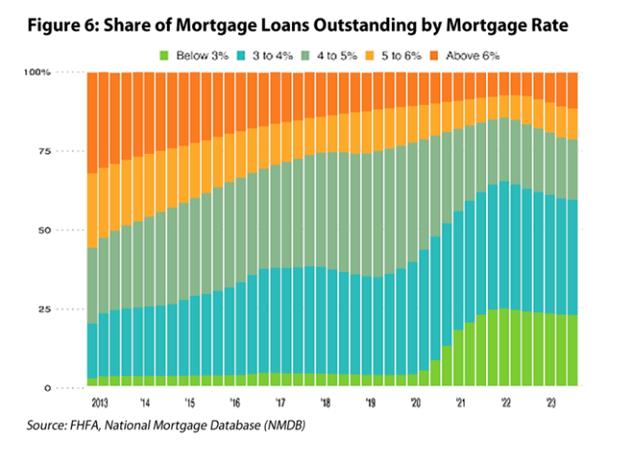

And secondlyMore and more people are likely to choose to rent due to the rising affordability of home ownership due to rising interest and mortgage rates. I estimate that the average new mortgage payment is currently more than 50% higher than the rent for a similar apartment.

The thing is, home ownership is unlikely to get cheaper anytime soon, especially because… Locking effect Of existing homeowners who have little incentive to sell their current home, wiping out their low-interest mortgages in the process, only to buy a new home at a more expensive mortgage rate.

FHHA, National Home Mortgage Database

Because of these factors, which are likely to lead to a significant reduction in supply and continued strong demand, I expect significant 5%+ rental growth to return to the Sunbelt after 2025.

Risks

Given the fact that deliveries lag behind building permits by two to three years, the supply until 2026 will be quite visible and constant. Thus the only danger to the above thesis lies on the demand side. In particular, any type of demographic shift away from the Sunbelt and back into older markets would likely have a significant negative impact on demand for rental housing. So is the housing crisis, which may once again make homeownership a mathematically interesting alternative to renting. But these risks seem very remote and unlikely at the moment.

Is MAA a buy, sell or hold?

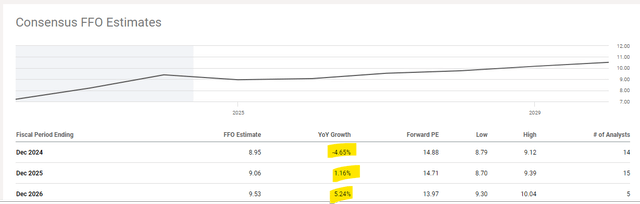

I believe the current consensus calling for a 4.6% decline in FFO in 2024, followed by 1.1% and 5.2% growth in 2025 and 2026, respectively, is likely to be correct and may prove too conservative after 2025.

Sa

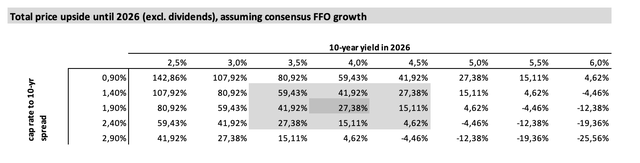

The current implied cap rate is 6.7% and will likely fall from the current 230 basis points to the 10-year Treasury to at least 180-200 basis points which is still a significant premium for a company with an A- rating. , especially when you consider that coastal peers like AvalonBay Communities (AVB) are trading at a spread of up to 110 basis points. Such a spread reduction, combined with consensus NOI growth and a drop in 10-year Treasury yields to 4.0%, would see prices rise 27% over the next three years, or 9% annually.

Seeking alpha

Add to that a dividend of about 4.5%, and you can easily make 13-15% per year under relatively conservative assumptions, and perhaps more if interest rates fall further over the next three years. This isn’t bad at all and brings me to that Upgrade MAA To buy here at $133 per share.