Image source/DigitalVision via Getty Images

apple (Nasdaq: Apple) He has come a long way in a short time.

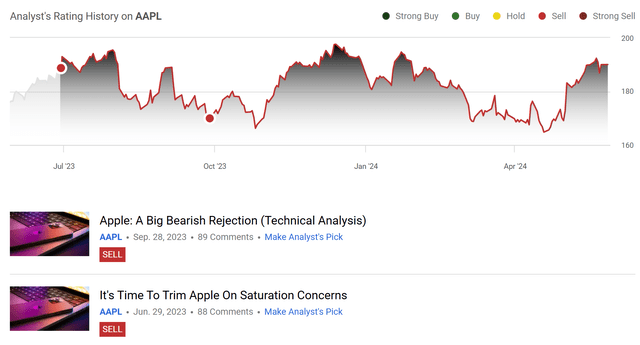

We first covered AAPL in June of last year, when we rated the stock a “sell” due to concerns about the company’s expensive valuation and weak growth. Prospects:

Seeking alpha

We then restated this view when the stock refused to break out of the high prices in the fall of last year.

Although the stock did not fall meaningfully in that time, AAPL stock significantly underperformed the market, rising 0.7% versus the S&P’s 20%+ performance.

However, as time passed and ChatGPT and genAI started to make their impact on the market, today, we are starting to see the stock in a different light.

In our view, AAPL is now no longer a legacy technology company that is falling behind, but rather a company with an incredible moat. It should be relatively immune to disruption at the hands of new AI tools and applications. Additionally, with services continuing to grow and a potential upgrade cycle with the iPhone 16, we believe the stock may be ready to move higher in the coming months and quarters.

Today, we’ll dive in and take a closer look at AAPL’s bulletproof business model, the company’s attractive valuation, and why the stock is a better option for those who want to remove the risk of AI disruption from their investment portfolio.

looks good? Let’s jump.

What changes?

Since the release of ChatGPT in November 2022, the world of technology has changed radically in some ways.

Companies from across the spectrum have begun to look for AI use cases to improve business processes, and many of the largest technology companies, including Google (GOOGL), Meta (META), Amazon (AMZN), and Microsoft (MSFT) have turned to their direct focus. On securing computing for the next generation of AI applications and developers.

This gold rush has sent Nvidia (NVDA) worth several trillion dollars and transformed public expectations when it comes to content, media, and the technological capabilities of modern-day applications and experiences.

One company that has been virtually silent on the subject? apple.

While the company has a number of products that could be affected by changes in the AI landscape, such as Siri, the company’s business is not directly affected by the introduction of on-demand knowledge applications such as ChatGPT. Demand for AAPL devices remains high, and the company’s unbeatable physical network means its premium services and content offerings will be little affected by the changes.

In other words, for us, it is still not clear from There will be ultimate winners and losers when it comes to the genAI opportunity. However, we’d bet money that users will do this even a decade from now Access These applications are through AAPL devices and devices. This stability represents a very attractive opportunity.

Apple Finance

As you know, AAPL’s core business is designing and selling personal computing devices, including the iPhone, iPad, Mac, Apple TV, Apple Watch, and most recently the Vision Pro. These devices cover the gamut of touchpoints between human experience and technology, whether that’s everyday comfort (iPhone), relaxation and entertainment (Apple TV), exercise and activity (Apple Watch), or productivity (Mac, Vision Pro).

Apple then built a secondary services business on top of this hardware ecosystem, providing access to the app marketplace, along with financial services, content offerings, productivity apps, and more.

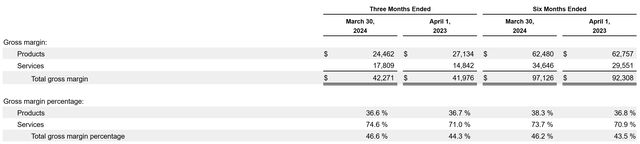

The hardware business is large, but its growth is lower and its margin is lower. In contrast, the services business is growing quickly, and the margins are better:

10 s 10 s

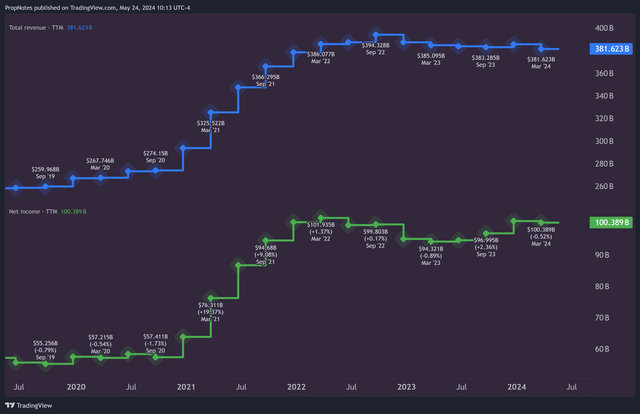

This combined profile results in a relatively high margin and moderate growth profile:

TradingView

It’s true that growth has slowed over the past few years, largely due to the slow upgrade cycle with the iPhone. Many recent iPhone updates have been very incremental, but many expect next year’s update to be even more significant, including much longer battery life, as well as spatial video support, thinner bezels, a better display, and more.

In our opinion, this should be enough to convince many iPhone 10s, 11, 12 or 13 users to upgrade to the iPhone 16.

Additionally, as the computing demands of applications increase, newer devices will be able to run these experiences better, which will also increase demand for upgrades.

Therefore, between the potential for iPhone 16 outperformance and continued organic growth in services, we believe revenue and net income should continue to trend up and to the right over the medium term.

Apple’s isolated market position

Competitively, here are the main reasons we like AAPL’s position in the market.

1.) User experience advantages

As we mentioned at the beginning, AAPL products are front and center in the user experience, which is a huge built-in advantage that is bound to continue.

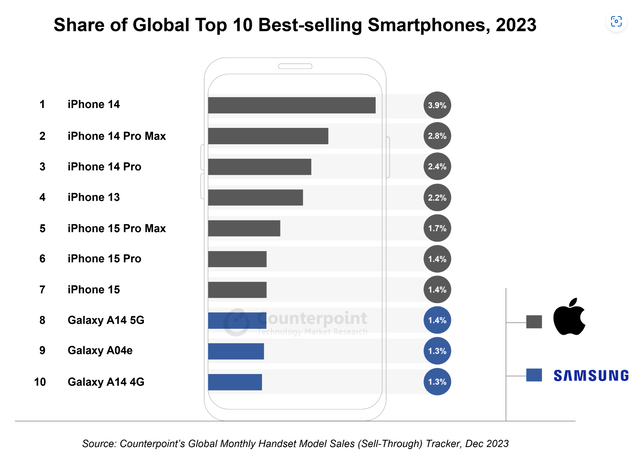

In the field of phones and computers, there are a number of competitors, including Acer and Samsung, but the iPhone and Mac remain dominant:

Counterpoint Research

In spatial computing, the Meta is really the only competitor, and while the Meta is expected to sell more than 3 times as much as the Meta Quest 3 in 2024 versus the Vision Pro, the Vision pro is 7 times the price, resulting in a revenue advantage for AAPL in this category.

Everywhere you look, AAPL has a strong position in consumer hardware. Looking to the future, this is important for one main reason – User experience stack.

When it comes to competition in the genAI space, it’s not clear who the winner will be, as we mentioned before. Maybe GOOG’s huge search business will be disrupted. MSFT’s investment in OpenAI probably won’t pan out.

With the technology landscape moving so quickly, it’s not clear how things will turn out, in terms of profits, for big and massive tech companies focused on apps and services.

However, we expect that no matter where things go in the digital world, users will continue to use these services On AAPL devices.

AMZN, GOOG and others play chess – AAPL is the chessboard.

Right now, this advantage stack can be clearly seen in GOOG paying AAPL over $20 billion a year to be the default search engine in Safari. Going forward, we expect AAPL to push this leverage further. At the very least, we don’t think they’ll face a material downside from being a decliner, in terms of AI.

2.) Insulation services

AAPL’s high-margin, high-growth services sector shouldn’t see much disruption from recent advances in artificial intelligence, either.

Apple’s content suite, which includes Apple TV+, Apple Music, Apple News+, and other apps, has significant distribution advantages, making it protected from infringement. AAPL content heavy The approach here is smart, as the company isn’t competing in any cognitive or functional applications — just content creation and curation:

Apple.com

Additionally, AAPL’s financial services sector, with Apple Card and Apple BNPL, doesn’t face much disruption from genAI.

Finally, AAPL is too Well placed to take the cut New entrants to the AI market who will monetize their apps through the AAPL App Store.

As new entrants to the market want to expand their apps and bring them to a large audience, the Apple App Store remains one of the best ways for them to do so. And with AAPL’s monetization model, they are ideally positioned to charge for this access. As AI applications are monetized and scaled, this can fuel service revenue growth

These network advantages mean that the company’s service segments are incredibly robust due to AAPL’s distribution and extreme leverage.

3.) Vision Pro

Finally, Apple’s recent Vision Pro launch shows that the company is still looking to the future of computing.

With the categories of phone, tablet, laptop, desktop, watch and headset saturated, AAPL’s advancement into a new frontier, XR (mixed reality), is exciting.

While the new device is key to AAPL’s mid-range consumer computing hardware ambitions and market presence, more importantly it shows that the company is keen to keep the crown when it comes to… being Top of the funnel for the technology industry. The Vision Pro line will not only keep AAPL at the forefront of consumer devices for the foreseeable future, but also shows that the company continues to innovate in the areas that matter most.

A strong hardware presence is critical to the aforementioned network advantages and service segment profitability, which is why AAPL’s continued innovation on this front is encouraging.

Apple company evaluation

But what is AAPL worth? All of this wouldn’t matter much if the stock was expensive.

Fortunately, we think the company’s valuation is reasonable.

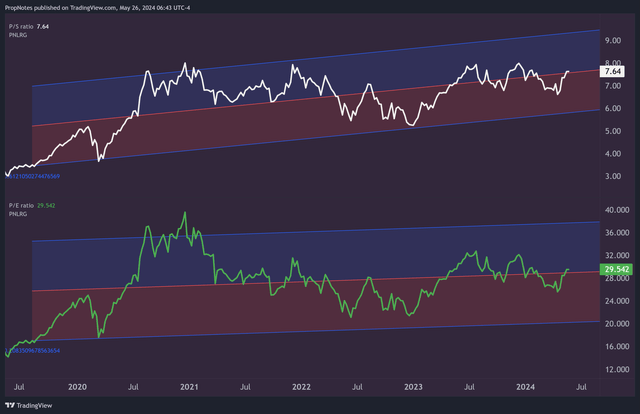

Trading at a 7.6x sales multiple and a 29x earnings multiple, the company is by no means “cheap,” especially when nominally compared to the broader S&P 500 index:

TradingView

However, on a historical basis, the stock appears to be trading at a “midpoint” of sorts, hovering around the point of a 5-year linear regression trend.

Being in the middle, that’s not a great Price, but it is also far from overvalued, or near the top of the standard deviation ranges shown above.

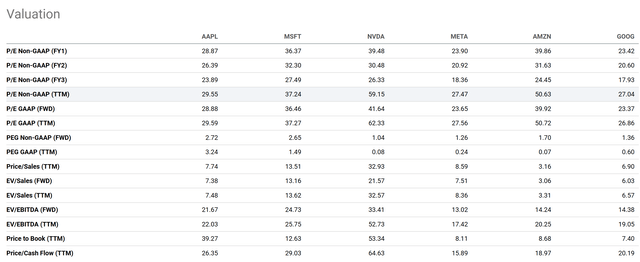

Additionally, when viewed in the context of other large technology companies at the time, AAPL’s valuation appears modest, appearing at the mid-to-lower end of the pack on most earnings and sales multiples:

Seeking alpha

This is undoubtedly due to AAPL’s lower level of expected growth, but given the potential durability of AAPL’s earnings, this is a price we are willing to pay.

Overall, while AAPL looks fairly expensive on a nominal basis, when compared to historical multiples and peer valuations, the stock actually looks reasonable at this point.

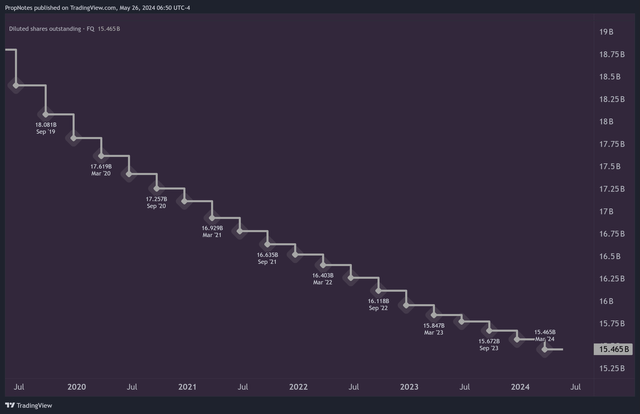

Additionally, with an additional $110 billion allocated to buybacks, this is a strong value proposition for both demand and demand And Supply side of stocks:

TradingView

Risks

There are some risks that come with investing in AAPL, despite the company’s risk-free market status.

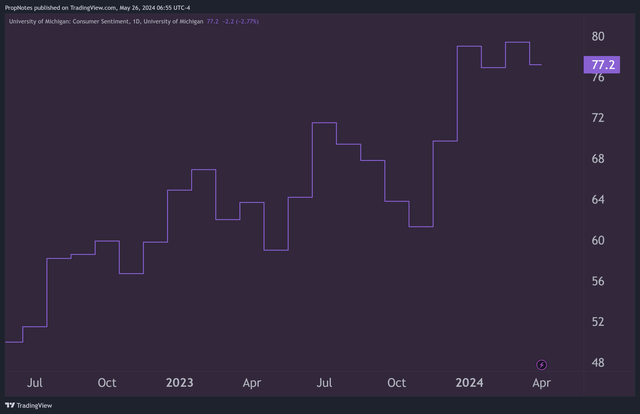

First, AAPL may see continued decline in sales growth for iPhone and other devices, which could result in lower-than-expected profitability. We believe this risk has been reduced somewhat due to the recent increase in consumer sentiment over the past year, which may boost spending on personal devices:

TradingView

However, there is still a risk you should be aware of.

Apple’s overall growth is also at risk due to macro factors that drive broad market demand and supply, including interest rates. If prices continue to rise, this could slow business spending, which could slow the economy, which would have an impact on business and individual spending on AAPL devices.

Additionally, interest rates can also determine market multiples, so if interest rates move higher, it could hurt the AAPL on both base currencies. And Multiple fronts. This is a major risk that you should be aware of.

Finally, there is a risk that AAPL (and the rest of the market as a whole) is simply “too expensive” right now. Comparing to historical valuations and peers can only do so much, and even a historically decent “buy” price would have undergone a significant drawdown in 2022, when technology multiples emerge and interest rates rise.

It appears as though AAPL’s higher multiple is here to stay due to services offering a structurally higher level of profitability, but buying AAPL at roughly 30x earnings and a moderate growth profile could cause problems in the future if the multiple is priced back lower.

summary

However, despite the risks, we believe AAPL is a unique opportunity in today’s market. With its strong position in personal computing and a strong leverage point at the top of the funnel, it’s hard to see the company losing business as a result of the genAI gold rush.

With a risk-free business model, a strong services business that will boost growth and margins, and a new XR product on shelves, we believe AAPL is positioned to weather the changing technology landscape better than almost anyone else.

Therefore, we are upgrading our AAPL rating to ‘buy’.

Good luck there!