com. bjdlzx

(Note: ARC Resources is a Canadian company and advertises the use of the Canadian dollar unless otherwise stated.)

Overshadowed the usually good quarterly reports ARC resources (OTCPK:AETUF) is the company’s guidance that an unusually large amount of production will occur Access to the Internet at the beginning of the fiscal year 2025. Appendix Stage 1 Oil will be sourced for the first time at the end of the year, with full production expected in the first quarter of 2025. Management expects a roughly 10% increase in production over the current fiscal year as a result. This news may dominate stock price movement in the second half of the year unless another, more significant event occurs that affects the company.

Appendix Stage 1

A previous article mentioned the extraordinary profitability of these wells due to the large quantities of condensate produced. Canada often has to import capacitors To meet her needs. Therefore, condensate is often sold at a higher price than light oil. The management is now launching a major project with the production of more important capacitors. Profits are likely to see a big jump in the next financial year.

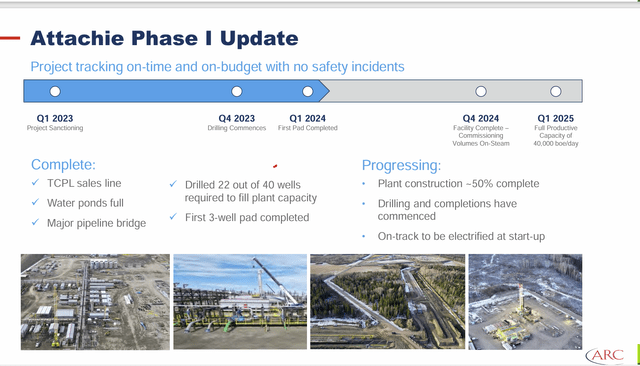

ARC Resource Supplement Phase 1 Update (ARC Resource Update May 18, 2024)

Upon completion, the project is expected to produce approximately 40,000 barrels of oil equivalent. The wells themselves have a fairly large production rate, as shown below.

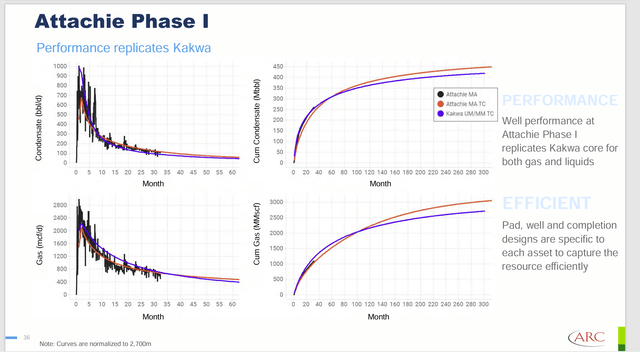

ARC Resources Summary of Accessory Well Performance Characteristics (ARC Resources Presentation May 18, 2024)

Perhaps the most important figure is the total condensate production in 20 months. In very rough terms, production exceeds 200,000 barrels of condensate. Under many industry pricing conditions, that would be a very profitable well.

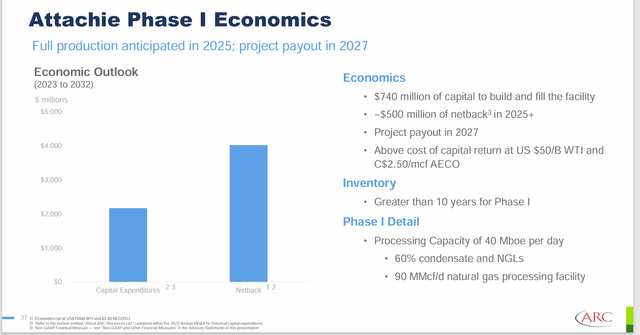

Initially, this project will help what has had a proven track record with above-average project profitability.

ARC Resources Project Profitability Performance Guidance (ARC Resources Presentation May 18, 2024)

The payback period is very attractive for such a large project. The previous slide shows that these wells will produce well beyond that payback period. Naturally, management focuses on the first 9 years or so, with production in about 8 of those years.

After that, the “everything” will likely have to be paid several times over and the project will likely be run for cash flow or sold if the selling price includes enough future returns. ARC Resources is generally not a company that keeps projects going “to the end.”

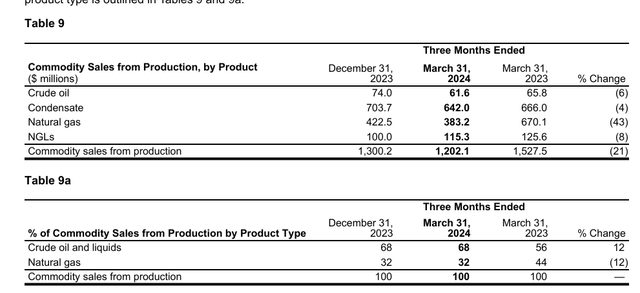

Sales amounts

Although the crude oil and condensate share of production represents approximately one-quarter of production, sales of the more valuable condensate and light oil account for the majority of sales dollars. This mitigates the impact of lower natural gas prices.

ARC Resources Q1 sales by product (ARC Resources Q1 reports filed with Sedar)

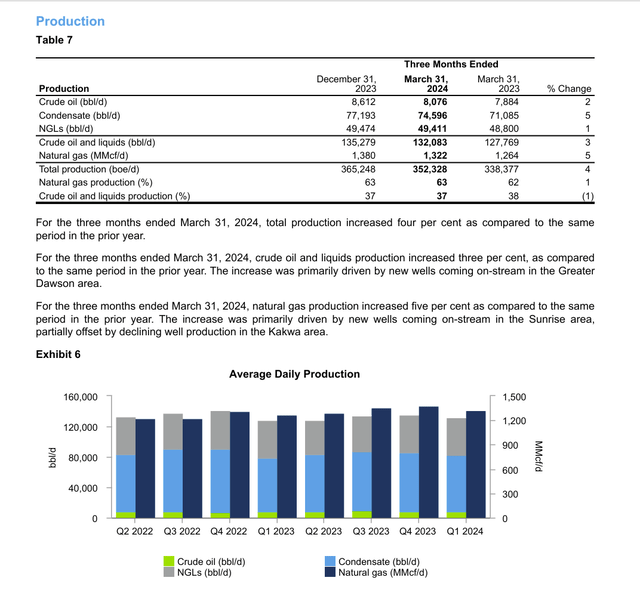

Note that this company, like many natural gas producers, will produce natural gas in the fourth quarter to take advantage of the prices available during the important heating season.

Therefore, lower production in the first quarter compared to the fourth quarter is not unexpected. Sometimes, Canadian winters exacerbate this decline by presenting some unexpected challenges.

Likewise, the second quarter is often a good time for turnaround projects due to spring break. Spring Breakup often limits the operating options available until sometime in the summer. Spring break is often followed by a (usually) short fire season that also causes operational challenges. Last year’s first season was unusually long.

ARC Resources production trend (ARC Resources first quarter reports filed with Sedar)

Many drilled wells have acceptable flow rates for only the natural gas portion of production. Light oil and condensates are the “icing on the cake” which at worst turns a marginal situation into a very profitable one. Some of these wells appear to be highly profitable from natural gas production alone.

Aside from that, ARC is another company that achieved a premium price of almost 50% for its AECO benchmark for natural gas. The natural gas sales strategy also contributes to this company’s relatively strong profitability performance compared to competitors.

It’s an example of how this administration is going the extra mile. Management is already getting good results from the relatively large amount of capacitors in the sales mix. But they do more by getting a premium price for natural gas.

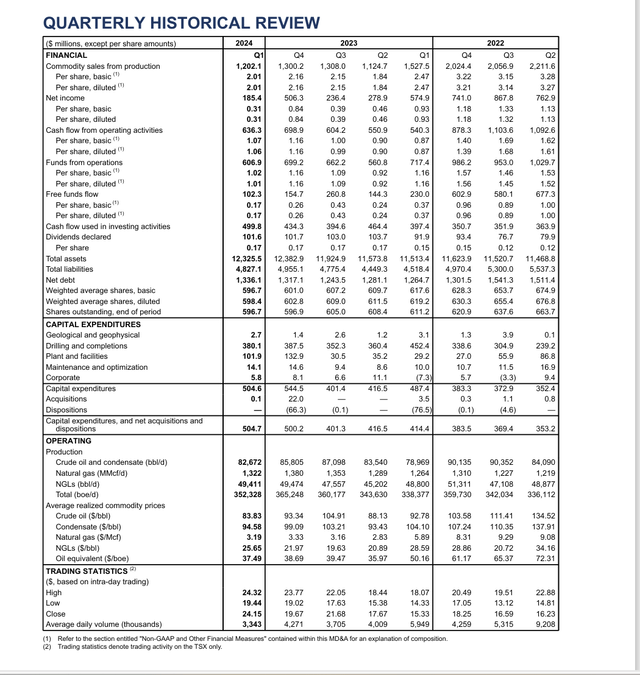

Earnings trend

Net operating revenue was relatively unchanged, despite relatively weak pricing compared to the previous quarter and the fourth quarter of 2023. This is because the average selling price remained relatively unchanged.

ARC Resources Earnings Trend (ARC Resources Q1 reports filed with Sedar)

As the trend clearly shows, much of the growth expenditure is coming with increased production in the second half of the fiscal year.

Now it may appear that Project Attachie is changing that with full production scheduled to impact the first quarter. But this is only due to the size of the project and thus to the time required to produce the entire project. If the project consists only of wells, commissioning will likely occur only in the second half of the fiscal year.

The other thing to note is how well cash flow persists despite the collapse in earnings in the first quarter. This is a company that merged with Seven Generations in FY 2021 with the hope that the increased percentage of oil and condensate production would allow it to perform much better in a situation like FY 2020. Personally, I hope we don’t have to find out.

summary

ARC Resources is bringing a large project online that will produce approximately 10% production growth in fiscal 2025. The project itself could have a significant impact on earnings if the production mix is more valuable than the company’s current production mix to result in a significant upside. Enhancing the company’s profitability.

ARC Resources is Canada’s largest condensate producer. This is important because condensate commands a premium over light oil prices in Canada. ARC is therefore in a position to produce and sell large quantities of a product that commands a higher price than light oil.

Since its costs per barrel are very similar to many natural gas producers, this has made it a very profitable company.

ARC is a company that has been growing through share buybacks with occasional opportunistic acquisitions (such as Seven Generations in fiscal 2021), and the periodic addition of major projects. When this strategy is combined with a dividend, the total return for this investment-grade company is in the teens.

This makes this investment idea a strong consideration to buy because a lot of larger companies don’t offer this great a return with an investment grade rating. Also, many companies do not enjoy the profitability that capacitor production brings to the company.

Risks

Any upstream product is subject to volatility and low visibility of commodity prices. Here there is the additional risk that the premium obtained by selling capacitors could tighten (or worse) in a cyclical downturn when commodity prices are weak. This is especially true if there is a recession or worse affecting the North American economy.

Financially, the debt ratio is usually one of the lowest I follow, and the company has an investment grade rating. This reduces much of the upfront financial risk that typically accompanies smaller or financially weaker competitors. Here, the availability of debt flotation does not constitute a problem.

Another consideration is that companies with low debt rarely get into serious trouble. Therefore, long-term capital loss does not pose a major problem. Instead, these companies often get as many opportunities as they need to succeed and grow over the long term.

This natural gas producer is expected to benefit from North America’s increasing ability to export natural gas. As a result, North America can join the typically much stronger global pricing market. This would greatly benefit this low-cost product. However, the timing of all this is uncertain. Because the industry has low visibility. Unexpected events can delay all those great things beyond the expected time frame. Rather, the market could continue to decline in commodity prices, which could change the entire future outlook.

The loss of key employees is likely to have a material impact on the future of the company.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.