HJBC

Dear readers/followers,

I have been following ArcelorMittal (New York Stock Exchange: metric tons) for a few years now, and have been investing for a little over a year, and I haven’t really gotten much “value for my money” – at least not yet. However, there is a lot to like The company, and a lot of upside is expected depending on where the company can go from here. ArcelorMittal is one of the most important global companies in the cyclic steel sector. I’ve previously described At The Right Price as a must-have type of investment – and I’m following my own advice.

In today’s tech-heavy, bloated market, as I see it, we don’t find many investors or analysts embracing the positives of these legacy players, despite the reality of what kind of market they need to be in.

There is no problem with me. I know that in In the short term, the market is a “voting machine.” I think the way the market is moving and the trends we are seeing today make that very clear – but in the long run, the market is a ‘value machine’. Whether it takes 1 year, 5 years, or even longer – eventually the company’s value and positives are recognized and priced in the market where I consider them to be more “correct” overall.

Let’s see what ArcelorMittal has done since my last article, which you can find here, and where it can go from here.

ArcelorMittal – Let’s find and work on the positive side in steel

With approximately 100 million tons of annual steel production, ArcelorMittal is a specialist in a world of specialists. In the automotive sector alone, MT works with over 200 grades of steel – and you can imagine the kind of overall specialization this brings to the table in other sectors too. The move from commoditization to specialization has been a big one for MT.

Arcelor was a Western European steel company, and Mittal was an Indian steel company. ArcelorMittal is a combination of those, and I’m grateful for the fact that the merger went this way, rather than the then-proposed merger between Arcelor and the geographically closer Russian company Severstal – and considering the kind of nightmare scenario that could have played out today, given the Russian invasion of Ukraine, Since it seems likely that Russia will end up in the EU-Russia economic contacts in the next few years, this could have derailed the whole business.

MT has spent the last decade or so improving the fundamentals and working “smarter and better” – more efficiently, rather than just working “bigger”.

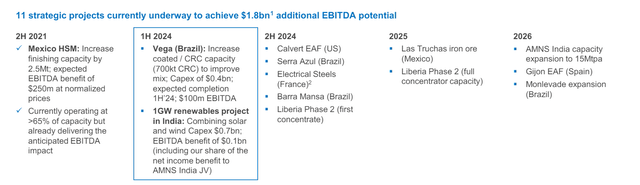

The first quarter of 2024 for the company is what we have to work with here, and ArcelorMittal shows a strong continuation of the previous trends that led me to invest here in the first place. We are seeing strong organic EBITDA growth, with a potential increase of $1.8 billion by the end of 2026E. The company is disposing of non-core and sub-standard assets that do not fit the company’s portfolio, such as Erdemir, after selling KAZ in Q4 2023, while at the same time buying niche players.

This quarter marked the purchase of Vallourec, 28% of its shares, for approximately $1.1 billion – a clear sign of the company’s strategy of Higher value, better margin, cash generating companies.

ArcelorMittal has a stronger, consistent return process, including additional repurchases of more than 22 million shares in the first quarter for up to $600 million, bringing the total shares repurchased in the year Less than 4 years, 35%.

This exceeds most levels I have seen, and is one of the reasons for the strong returns we are seeing here.

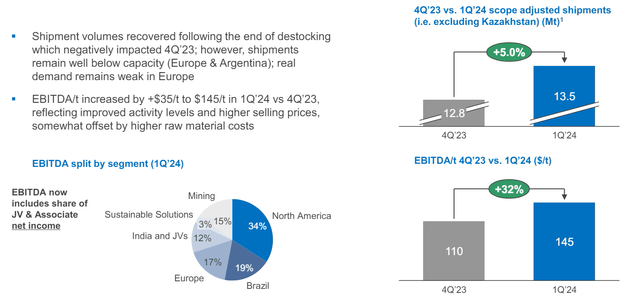

Results are improving slowly Here — that’s the keyword, although it may seem fast when you see EBITDA improving 32% sequentially.

ArcelorMittal IR (ArcelorMittal IR)

There are several reasons for this, as you can see. There is an ongoing destruction of inventory, which has almost ended as of this last quarter. the Clear Demand is improving, but for those of you following industry commentary and journals, this reflects a generally lackluster economic environment – Because customers haven’t restocked it yet.

A big part of this is China. It would not be wrong, I see, to call these domestic margins “awful” – they are so low that they are priced well below domestic and European levels in the US, resulting in unfair Chinese advantages in exports that are still at their extremes. . At the very least, Europe is moving against providing fair competition to the global steel industry. Meanwhile, EU and North American spreads are slowly stabilizing – again, the key word here is slowly.

The industry’s EBITDA improvements reflect cost and price expansions as well as an uptick in freight volumes. Mining has actually gone down due to ore prices, and of course shipping costs have gone up due to logistics and inflation in general which has pushed things up.

Fundamentally and fundamentally, there is nothing at risk with ArcelorMittal. With net debt of about US$4.8 billion, the company’s price has been below US$5 billion for more than a year now – much higher than it was during 2023, but that was due to buybacks and investments.

It is important to remember that MT’s working capital needs vary greatly in nature, which means that seasonality must be taken into account.

Also a good measure is liquidity – the company had roughly $11 billion of cash at the end of last year, and I don’t see any problem for the company to finance anything in the near term.

The company is moving forward with its

MT’s plan is for continued growth in the form of organic investments to support EBITDA growth of $1.8 billion by end-26, as we mentioned. This includes a 11 complete strategic projects To achieve this.

ArcelorMittal IR (ArcelorMittal IR)

Vallourec’s stake to increase exposure to VAP in the Americas is a key play here as well – among other things, given the very attractive price at which the stake was purchased – i.e. a zero premium to the market, given current market conditions. MT is skilled at “buying cheap” here.

Additional strategic approaches to allocating capital include spending more than 30% of CAPEX on strategic growth, and shareholder returns will likely continue to focus on buybacks here. The $0.5 per share dividend rule is a nice little bonus but doesn’t do much to move the needle overall. I’m happy to be part of the buyback program here – although I think once the stock price gets to a certain level, we don’t necessarily want to see a lot of that.

Going forward, I expect a sharp change in profitability metrics, and with the large number of projects now scheduled to start in early 2024, I expect the company to trend further to the upside – we can also see this in the current set of estimates, which actually extend out to 2020. 2026E. The company’s sustainable solutions segment is a big part of this.

ArcelorMittal IR (ArcelorMittal IR)

Let’s take a look at the evaluation.

ArcelorMittal Valuation – Lots of long-term upside

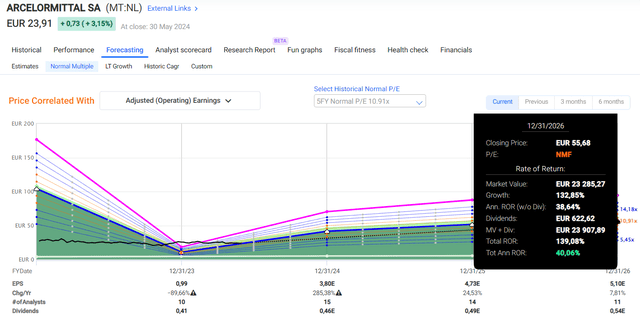

Depending on how you view the company’s future outlook, there are a wide range of potential positives at this time. I choose to forecast ArcelorMittal at around 10-12x P/E, which is at the lower end of its 20-year average, and is closer to 14-15x P/E (link to paid quick charts).

Even at this relatively low overall valuation, this company still has triple-digit upside in current forecasts – mostly due to those forecasts.

ArcelorMittal Fast Charts Forecast (ArcelorMittal Fast Charts Forecast)

If you make these forecasts, you are relying on the future accuracy of those forecasts. Historically, this has not been accurate. But that’s why I’m applying Discounts To evaluate the company – to make up for it. That’s why I don’t expect ArcelorMittal to be priced at the original €55 per share, but at the previously announced $37 per share – a significant discount to the company’s US-based ticker, bringing that price down to less than an 8.5x P/E even With these growth estimates.

The main issues with the company are really related to revenue and cyclicality. Fundamentals are mediocre, even if the company’s rating is just BBB – now despite having long-term debt of just 12.95% of capital.

The company isn’t spending a lot of money on its dividend right now — the sub-1.6% yield means that dividend isn’t really an issue here, but you’re also getting about half of what you would get from even a risk-free savings account.

If you accept the risks of cyclicality, ups and downs, ArcelorMittal is in a very good entry position here. In the long term, if you “know your goals”, this is a company to look at. If I regret anything about MT, it’s not buying it sooner when it was really in the doldrums.

However, it’s more than a good enough buy here. Even in a very conservative scenario, where the company wouldn’t be able to manage any kind of massive outperformance, the massive EPS growth as expected from more than 10 new strategic growth projects provides enough upside potential to maintain my interest and keep me invested here.

Looking at the other analysts covering the company, and the current stock price of around €23 per share, I can clearly say that most analysts think the company is worth much more here. We’re talking here about 10 out of 13 analysts who consider this company a ‘buy’, with an average price target of €35 per share, with the low at around €21 and the high of around €45 per share. Since we are at €23 per share, this gives us a very large margin of safety for the average price target here.

Overall, I expect ArcelorMittal to outperform – over time, at least. Given its combination of low debt, growth projects, and focus on specialization rather than commoditization, it is something I firmly believe will eventually pay off. Although a low return is a high price to pay in this environment, I am willing to pay it for eventual upside in the triple digits for a business that I consider to be potential despite everything.

For this reason, I offer the company the following thesis for the US-based index here.

thesis

- This messaging for ArcelorMittal is currently a positive thing for one of the world’s leading steel companies. I consider the company investable based on its low debt, sector-leading coverage, and decent upside. There are “better” investments out there, meaning higher upside with decent security, but if you want exposure in this sector, there aren’t many companies that can live up to ArcelorMittal.

- Accordingly, I have joined the company with a “Buy” rating and plan to add to my current position in the company.

- My PT for MT remains conservative at US$37 per share, with the company currently trading below US$30 per share as of early 2024.

Remember, all I care about is:

- Buy undervalued companies – even if that devaluation is minor rather than staggeringly massive – at a discount, allowing them to normalize over time and reap capital gains and dividends in the meantime.

- If the company goes beyond normalization and goes into overvaluation, I take the gains and roll my position into other undervalued stocks, repeating #1.

- If a company is not overvalued but is hovering within fair value, or falling below its true value, I would buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash flows as defined in #1.

Below are my criteria and how the company meets them (in italics).

- This company is all about quality.

- This company is fundamentally safe/conservative and well managed.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a high enough realistic upside, based on earnings growth or multiple expansion/retracement.

I wouldn’t call the company “cheap” here, but it meets all my other criteria for an investment, making it a “buy.”