Dragon Claws/iStock via Getty Images

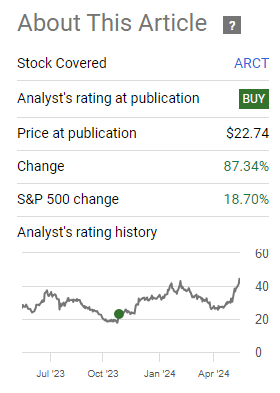

stingray fish (NASDAQ:ARCT) is one of my top picks for the biotech sector as I explained in a previous article. The performance of the stock market is a testament to the bullish rationale in… This stock.

Seeking alpha

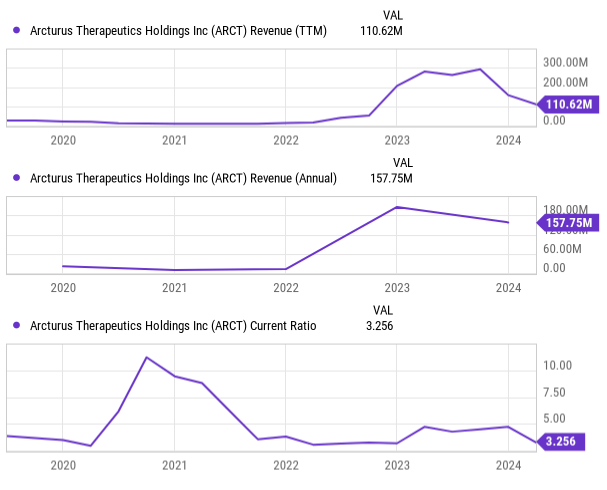

The factor that sets this company apart, compared to other similar counterparts in the sector, is that it is not a money-burning company, even without generating revenue from any proprietary commercial product yet. The unique element is that the company has been able to generate revenue from R&D partnerships, which has helped it maintain cash on the balance sheet.

YCharts

Sources of income

The revenue stream is not stable, as it depends on achieving milestones, but over the past two years, the company has consistently generated significant revenue from research agreements. Revenues are expected to expand Due to the imminent commercial launch of the Kostaev vaccine,… Vaccination deployment in fall and winter in Japan. The company also has a quadrivalent seasonal influenza program in collaboration with CSL.

The commercial launch of the Kostaive vaccine will also trigger a significant payment under the CSL agreement. In its 1Q24 earnings call, the company committed to revealing more details about CSL’s milestones and the vaccine’s revenue impact later in Q4.

Another noteworthy program is ARCT-032, an inhaled messenger RNA (mRNA) therapy for cystic fibrosis. This treatment aims to improve lung function in patients. The interim results were very encouraging and the stock price followed suit after the test results were announced.

Overall, the revenue growth prospects are very good in both the short and long term. Current estimates support this.

Seeking alpha

Finance

In the first quarter of 2024, the company reported revenues approaching $38 million, mostly stemming from the CSL agreement and BARDA grant revenue. However, operating expenses also increased to 68.4 million due to higher R&D expenses related to the preparation of CSL programs, production expenses related to the Meiji partnership, and internal pipeline development.

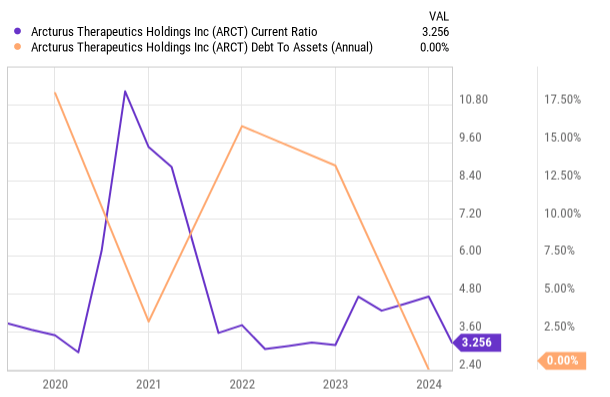

However, part of the higher costs are non-cash items such as stock-based compensation. This means that the company’s cash position has not been significantly affected. Cash-like instruments total $345.3 million at the end of 1Q24 compared to $348.9 million in 4Q23.

YCharts

Even as the company increases its launch capacity for Kostaive, it has maintained a strong balance sheet. The company stated that the cash runway is sufficient for three years, without taking into account any revenues from the commercial launch of Kostaev.

The company also made a strategic decision to monetize its stake in ARCALIS. Currently, Arcturus owns 38% of the organization. ARCALIS is a manufacturing joint venture, established in Japan to manufacture mRNA-based products. The company has completed construction of an mRNA manufacturing facility after receiving a $165 million grant from the Japanese government during the coronavirus (COVID-19) outbreak. Arcturus is now working with JP Morgan to evaluate options for monetizing the asset. The management team sees this as a strategic pivot for the company to become more asset-light and reduce fixed costs.

Prospects

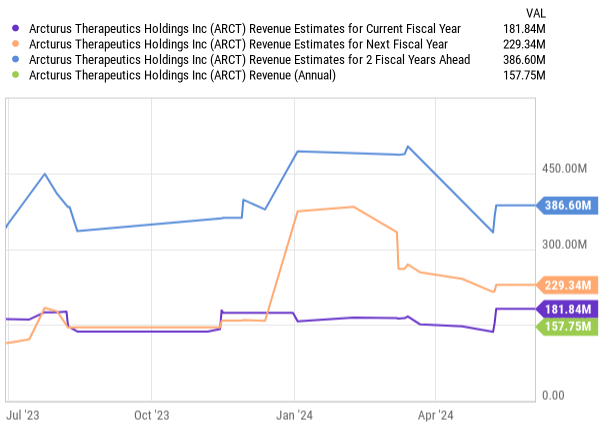

The preceding paragraphs provide positive evidence regarding the future prospects of the company. They have several payment agreements based on R&D achievements, and are at a turning point for the launch of the Kostaive vaccine. Current revenue estimates reflect that positive outlook.

YCharts

In addition, 2026 is also estimated to be the turning point for the company to become consistently profitable. Obviously the estimates should be read with a grain of salt, but they are a good sign nonetheless.

Seeking alpha

Evaluation and risks

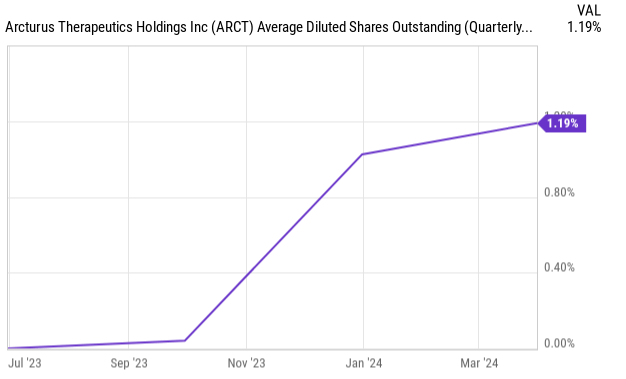

Given recent developments, we are now in a position to review the upside and downside scenarios we identified in the previous sections. Therefore, by updating our bullish and bearish estimates through 2026, we are increasing revenue to the current analyst estimates shown previously. Given the current strength of the balance sheet and potential asset monetization, we will now consider the same dilution for both bull and bear scenarios at 28.4 million shares, a growth rate of 1.19% per year.

YCharts

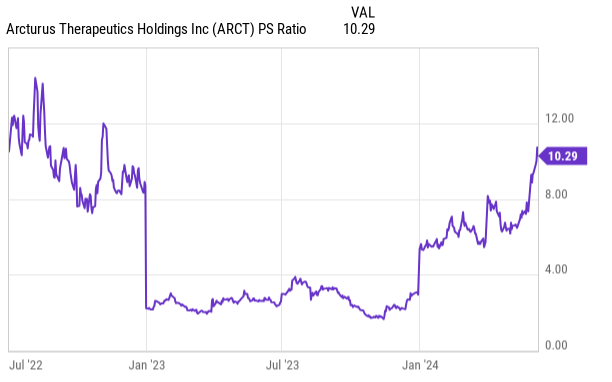

We also adjust the multiples for the downside scenario, which would now be 3, to reflect the historical development of the sales multiple, which has trended toward 3 during stock weakness and trended above 10 in times of strength.

Ycharts

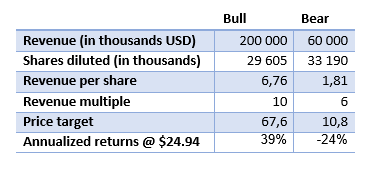

Below are the previous bull and bear scenarios, from the 2023 plot.

Author’s calculations

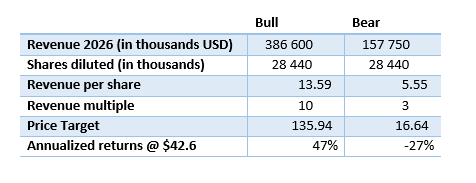

This is the revised version, based on the latest developments and updated model.

Author’s calculations

The results are very positive, and I believe this is one of the best buy and hold opportunities in the industry, but caution is needed. This investment involves many risks, and overall we can say that this investment involves higher risks than other more established alternatives in the pharmaceutical sector. As mentioned, the company consistently derives its revenue only from R&D agreements, meaning that revenue is dependent on achieving results that are inherently unpredictable.

In addition, the company is currently launching its first commercial product in partnership with Meiji and CSL. However, the company is yet to release more details about revenue sharing among all participants. So, although it is a very good prospect, we cannot understand with any degree of certainty its impact on the company’s top line. Finally, a lot of things can go wrong with the company’s current trajectory. There is significant public controversy surrounding the alleged side effects of mRNA vaccines, and we cannot be certain that this will not be a major issue in the launch and approval of these treatments, and the company is essentially an mRNA-only play.

Conclusion

The company’s prospects are very interesting, and our bullish and bearish scenarios suggest an asymmetric risk/reward proposition favoring the upside. There are inherent risks as we discussed, but I think this company makes sense in a diversified portfolio, and therefore I rate it a Buy.

I will continue to monitor the company, and more specifically the launch of the Kostaev vaccine, the company’s financial impact disclosure, and the development of its asset monetization program.