Crebloquin/iStock via Getty Images

Co-authored by Treading Softly

In 2001, the Oakland Athletics baseball team was devastated by a loss to the New York Yankees. In 2002, their general manager, Billy Beane, had to come up with a new team to… Replaced many stars who were leaving. The problem was that the Oakland A’s had a very small budget compared to many Major League Baseball teams. What Billy Beane ended up doing became the focus of the book (Moneyball: The Art Of Winning An Unfair Game) and eventually a movie starring Brad Pitt (Moneyball). Billy Beane decided to take an unconventional approach and apply mathematics to his baseball team’s roster. He wasn’t looking for individual star power or the standard method where scouts have a “feel” for a player. Instead, he applied strict calculations to try to put together a creative team The number of innings necessary to be able to win the majority of baseball games. To do this, he ended up assembling a sparse team with his roster full of rejects that others didn’t want to hire. Thus, he was able to obtain it at a steal price. The Oakland A’s, after taking some time to blend together, finished with a great season and attracted the attention of several other teams with bigger budgets. Today, Billy Beane’s method of building a baseball team is something even the biggest teams follow. He wasn’t interested in star players who could hit home runs all the time; It was more focused on singles and doubles.

When it comes to the market, many investors are fascinated by the big stars that shine in the investing world. People focus too much on big individual names, believing that these individual holdings can propel them to new levels of wealth, and in some cases they do. But when it comes to being an income investor, I’m more interested in getting those singles, evens and fundamental hits, because that way, my portfolio will continually provide me with an increasing stream of income.

Today, I want to take a look at the commercial real estate investment trust and its most recent quarter. The previous quarter had been a disaster, much like Billy Beane’s Oakland A’s loss to the New York Yankees. This quarter they have reached a fundamental base, and I am happy to collect a high yield and receive a bumper flow of dividends from them as they continue to move forward successfully.

Let’s take a deeper look!

Basic visits bring significant income

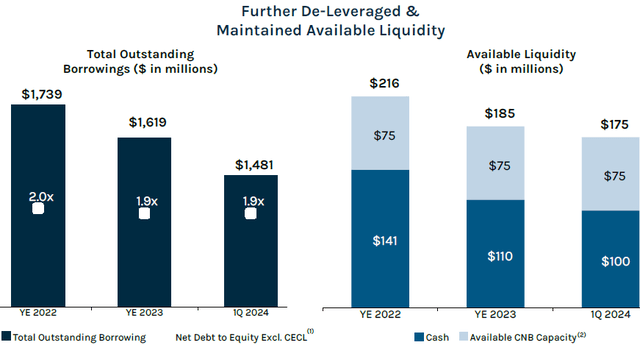

Ares Commercial Real Estate Company (New York Stock Exchange: Acre), which yields 15.3%, is a real estate investment trust that focuses on construction loans associated with commercial real estate as well as maintaining a diversified portfolio of these types of loans. If you remember, Q4 2023 earnings were just as bad. acre It experienced multiple defaults, a significant decline in cash flow, and significant capital tied up in distressed assets. As a result, ACRE decided to cut its dividend, saw its book value decline, and the stock price followed. The silver lining is that ACRE has continued to enjoy a strong balance sheet with leverage at just 1.9x debt/equity, meaning the negative impacts are more of a near-term earnings situation rather than a threat to permanently weaken ACRE’s balance sheet.

If the fourth quarter of 2023 was a strike, the first quarter of 2024 was a baseline strike. ACRE has resolved some of its problem characteristics, realized some already booked losses, and its distributable earnings, excluding realized losses, reached US$0.22 (versus US$0.20 in Q4 2023). It’s still a little shy of earnings. However, ACRE reported $0.25 for Q2, which management believes will be covered in Q2.

What happens when the borrower stops paying interest is that the earnings disappear immediately, but ACRE still pays interest on the portion of the debt used to leverage that loan. When ACRE is able to settle this loan, it gets some of the capital back, even if it makes a loss. This capital is redeployed or used to pay down ACRE’s debt, bring in new income or reduce interest expenses – either of which will improve earnings. In the first quarter, management chose to reduce debt and maintain a leverage-to-equity ratio of 1.9x. source

ACRE Q1 2024 Presentation

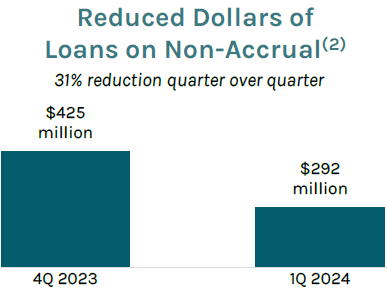

During the quarter, ACRE reduced the amount of its outstanding loans from $425 million to $292 million, a 32% decline in one quarter, a really strong pace.

ACRE Q1 2024 Presentation

The pace of resolution will be staggered, as each loan must be addressed individually.

Currently, ACRE has eight loans with a risk rating of 4 or 5, which make up the bulk of ACRE’s CECL (current expected credit loss) reserve. As these loans are resolved, ACRE will realize losses but will also increase cash flow as its capital is placed in productive assets or to pay down debt. On the earnings call, management directly addressed three of the 4/5 risk-rated loans that it expects to resolve in Q2 or early Q3. One is a multifamily property in Texas that they expect to sell, and two are office properties that ACRE is working to foreclose on. One characteristic is positive cash flow at the property level, so it will add to profits once ACRE passes the legal process.

It can be confusing because ACRE reports two book values - one including CECL, which is $11.04, and one excluding CECL, which is $13.63. The difference between them is the size of the ECL reserve, which is divided into two parts: general ECL and specific ECL.

General ECL is an amount that models determine to be the average credit loss that ACRE can expect, given current economic conditions. These models take into account interest rates, market default rates, expected economic growth, and many other economic factors in an attempt to predict default rates.

Specific expected credit losses are the amount that is expected based on a particular loan. This will be the amount of credit loss that ACRE expects when a particular loan starts having problems. ACRE may evaluate the collateral, or may update this number to reflect expected losses based on negotiations with the borrower.

In short, “general” ECLs are an estimate based on models of macro conditions. “Specific” ECL is an estimate based on known issues with a particular property.

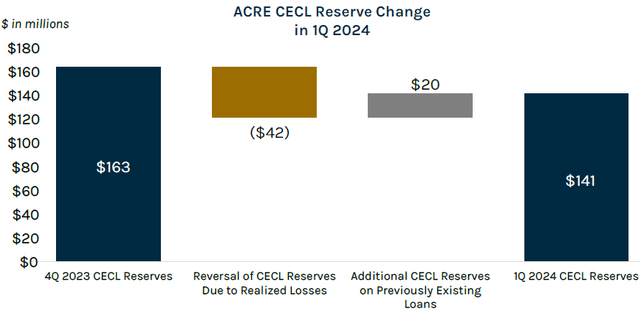

In the first quarter, ACRE’s identified expected credit losses decreased by $42 million. This is due to realized losses on loans for which a specific reserve for expected credit losses was previously recorded. However, at the same time, ACRE’s total expected credit losses rose by $20 million due to a further slowdown in the economy and expectations that interest rates will remain “higher for longer,” putting pressure on borrowers.

ACRE Q1 2024 Presentation

That’s why we saw ACRE’s book value decline from the fourth quarter. Carrying value before ECL decreased from $14.57 to $13.63 as a result of realized losses. Carrying value after ECL decreased from $11.56 to $11.04, with the increase in ECL overall playing the largest role.

Will ACRE’s book value decline in the second quarter? Book value before current expected credit losses will certainly do, because we know that ACRE intends to realize some of those losses that have already been recorded in current expected credit losses. The book value after expected credit losses is less clear. It will depend largely on the overall conditions. If the economy improves and/or expectations are for interest rates to decline, this number may stay the same or even rise. If macro conditions deteriorate, we may see larger reserves.

On the cash flow side, we expect ACRE’s distributable earnings to exceed $0.25 per quarter by the end of the first half. On the earnings call, management discussed the desire to go on the offensive, increase leverage, and take advantage of higher spreads. It is in negotiations with its lenders to ensure it has access to capital to finance the expansion without risking its flexibility to manage the remaining non-performing loans in its investment portfolio.

We expect that by the end of the year, ACRE will have successfully resolved the non-performing loans in its portfolio, book value will be more stable, and distributable earnings will exceed current earnings. We don’t expect management to be in a rush to raise the dividend, as it will likely want to retain some capital in 2024 and 2025 to help recover some of the realized losses.

Q1 was a major hit. For the second quarter, we expect another base hit. It will probably be Q3/Q4 before we can expect a reasonable possibility of some type of quarter that is managed domestically.

Conclusion

At the end of the year, I want to be able to look back and see that my income has continued to grow from the investments I have kept in my portfolio. My portfolio is considered successful if it generates a positive return and achieves positive income growth year after year. This is helped in part by the fact that I reinvest 25% of all profits that come into my portfolio to help her balance and income stream grow. This is what I call the Rule of 25 within my unique income method. I don’t need to own the most exciting property to be able to generate a premium income stream. You can make a lot of material wealth just by investing in passive market ETFs and letting them weather the various ebbs and flows of the market. However, for most retirees who need an income stream to cover their expenses, a passive market ETF lacks its ability to provide reliable income. Most of us don’t want to liquidate our savings so we can pay our energy bills. Instead, my dream for each of us in retirement is for our portfolio to pay for retirement and leave us room to be able to enjoy the best things life has to offer. You don’t need to hit a home run to be able to do this. All you have to do is be able to win baseball games.

That’s the beauty of my income method. That’s the beauty of income investing.