Michael H

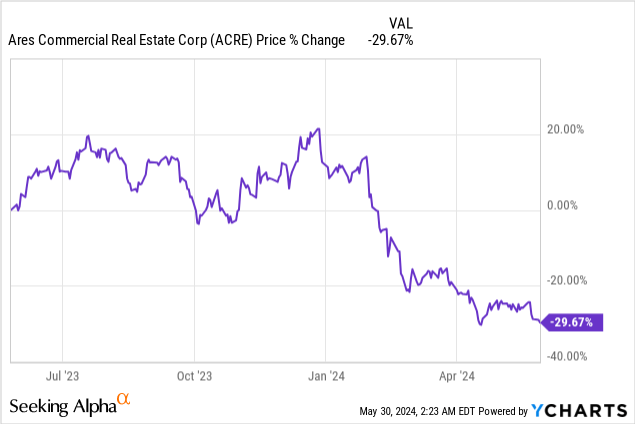

Distribution coverage file for Ares Commercial Real Estate Company (New York Stock Exchange: Acre) deteriorated again in the last quarter, as the Real Estate Investment Fund sold 3 loans, causing realized losses worth $46 million. As a result, the REIT did not support its price of $0.25 Quarterly earnings per share with distributable dividends, which increases the odds of further dividend cuts in the short term. The issue here, from a valuation standpoint, is that Ares Commercial Real Estate recently cut its dividend by 24% in order to account for the decline in earnings available for distribution. With a sudden loss impacting distributable earnings negatively, I think investors should take a more cautious approach to ACRE!

Previous evaluation

I recommended purchasing Ares Commercial Real Estate stock as a speculative purchase in February 2024 because I thought the REIT It will see improved dividend coverage after the company cut its dividend from $0.33 per share to $0.25 per share in February which represented a 24% decline. However, the REIT disposed of impaired loans at a loss in Q1 2024 in order to shed its balance sheet which came at the expense of Ares Commercial Real Estate’s distribution coverage… which means my expectations regarding the thesis were not met: ACRE shares have fallen 7% since then and continue to trade near one-year lows (due to concerns about the REIT’s dividend coverage). Given the fact that ACRE has underperformed its earnings in two straight quarters, I’m also erring on the side of caution here and accepting a wait-and-see approach.

Reduced ECL reserve due to realized loan losses

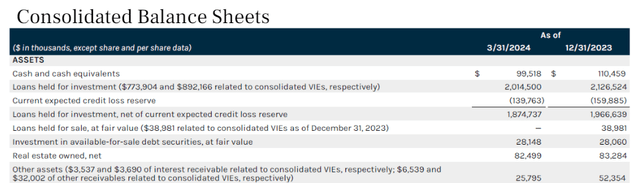

Ares Commercial Real Estate had a loan portfolio of $2.0 billion at the end of the March quarter, which remained impacted by ongoing quality issues. ACRE’s total loan amount was spread across 44 loans, 8 of which were said to be somewhat impaired. In its fiscal first quarter, Ares Commercial Real Estate exited three investments (including a $38 million mixed-use loan that was classified as held for sale).

Ares Commercial Real Estate

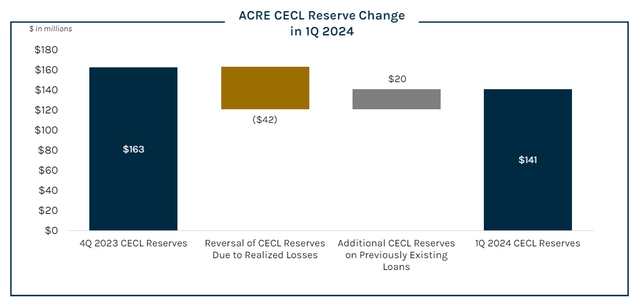

Loan sales caused a $57.6 million loan loss to Ares Commercial Real Estate and shareholders in the first quarter. Currently, the REIT has a current expected credit loss reserve of $141 million, which showed a 13% decline QoQ. However, Ares Commercial Real Estate recognized a reversal of $42 million in its ECL reserve solely due to realized loan losses. In other words, Ares Commercial Real Estate took an immediate loss on those loans rather than prolonging the position and risking increasing its long-term ECL reserve.

Ares Commercial Real Estate

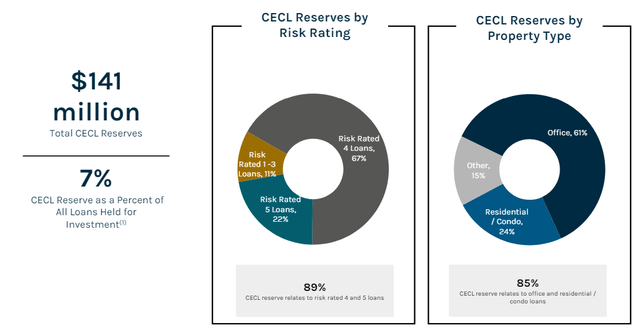

The majority of Ares Commercial Real Estate’s CECL reserve (61% to be exact) relates to the company’s office loans it has made in recent years. It is by far the most volatile asset class in the market as well as within the Ares Commercial Real Estate portfolio, and this unfortunately means that future sub-par loan sales are possible and likely. This will have a negative impact on the REIT’s distribution coverage profile and on Ares Commercial Real Estate’s valuation.

Ares Commercial Real Estate

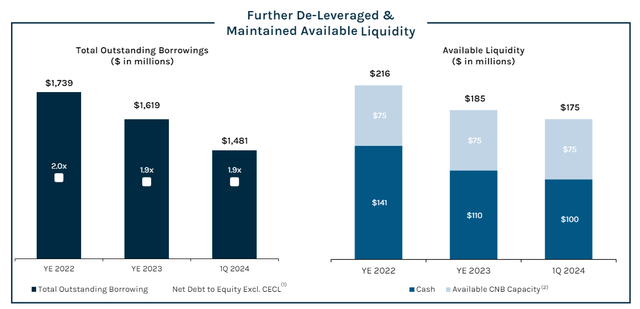

Liquidity and the trend of deleveraging

Ares Commercial Real Estate recognizes that loan problems cause investors to worry about dividends, and the real estate investment trust reduced its leverage ratio last year. From a liquidity perspective, the REIT is well positioned, with access to $100 million in cash as well as an undrawn credit facility of $75 million. However, the biggest risk facing Ares Commercial Real Estate is not liquidity, but rather the potential for increased loan fees and book value losses.

Ares Commercial Real Estate

Forecast for fiscal year 2024

The most important metric now is the distribution coverage ratio. If distribution coverage takes another hit in the second quarter of 2024, earnings could be headed for a cut. From a strategic perspective, FY2024 is likely to be a transitional year as new assets and portfolio growth take a back seat to the restructuring of the loan portfolio, especially in the office sector. As a result, I expect the REIT to clean up its portfolio, continue to add to its reserves and potentially sell more impaired loans at a loss in order to de-risk the portfolio. In other words, Ares Commercial Real Estate will likely see its investment portfolio shrink this year, but it may return to portfolio growth (and book value) once its underperforming loans are retired or sold.

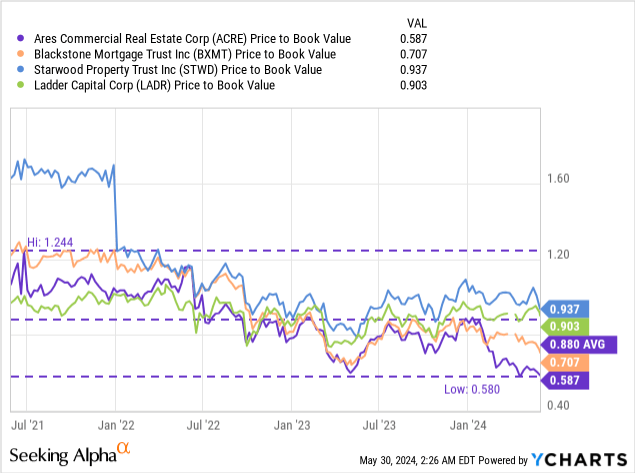

ACRE’s price is now less than 0.6x book value…

The increased likelihood of the dividend being cut again is reflected in Ares Commercial Real Estate’s uniquely large discount to book value. Currently, shares of the REIT are trading at a 41% discount to book, which represents a 33% discount to the long-term average stock price-to-book value of 0.88X and a 25% discount to the average price-to-book ratio. The industry group’s carrying capacity was 0.78. … Blackstone Mortgage Trust (BXMT) has also faced tough times recently, due to similar issues in its loan portfolio. I’ve detailed the problems with BXMT in my business here: Potentially cutting profits.

In my opinion, Ares Commercial Real Estate is trading at a slightly high discount to CECL’s adjusted book value of $11.04 (my fair value estimate), but I realize this is due to increased uncertainty about the REIT’s earnings. I think with the deterioration in REIT distribution coverage, a hold rating makes the most sense at this point.

Deterioration of distribution coverage profile

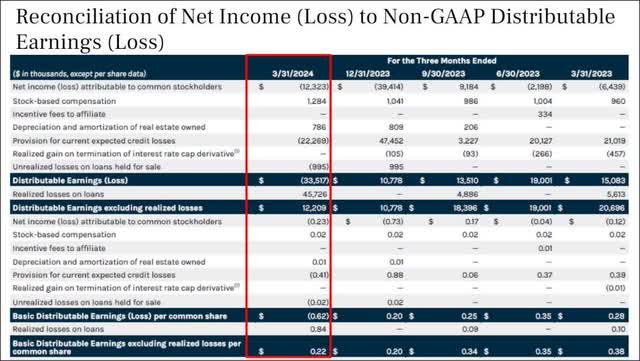

Due to Ares Commercial Real Estate moving impaired office loans off its balance sheet in the first quarter, the REIT had a $46 million realized loss that negatively impacted its earnings available for distribution. In the first quarter of 2024, Ares Commercial Real Estate had distributable earnings of ($0.62) per share adjusted for realized loan losses of $0.22 per share. Even on an adjusted basis, Ares Commercial Real Estate did not back up its $0.25 earnings per share with earnings (0.88X coverage in Q1 2024) and this was the second straight quarter that ACRE did not meet my coverage expectations. This does not mean that a dividend cut is imminent, but it certainly increases the odds of such a cut occurring in the future.

Ares Commercial Real Estate

Risks with Ares Commercial Real Estate Company

Ares Commercial Real Estate faces elevated near-term earnings risks, especially if the company exits its other office investments in the fiscal second quarter at a loss and fails to support its distribution with profits available for distribution. A third straight quarter of insufficient profits available for distribution would certainly increase the risk of another dividend cut, which dividend investors would find difficult to accept.

Final thoughts

Unfortunately, I think my latest buy recommendation came too soon, as shares are trading near new one-year lows. Although I believe it is good for Ares Commercial Real Estate to remove nonperforming loans from its balance sheet, the associated loss has unfortunately negatively impacted the REIT’s distribution coverage profile very negatively. If Ares Commercial Real Estate also sells other impaired office loans at a loss in 2Q24, which I think it is not unreasonable to suspect given its pressure to divest itself of other loans in 1Q24, the investment fund may have to Real estate to age reduce profits again in a very short period of time. Out of an abundance of caution, I’m changing my review to keep it!