Xie Wei

ARM Holdings PLC (NASDAQ:ARM) dominates the smartphone processor market, and is expected to penetrate more market share in the PC market amid the rapid growth of artificial intelligence computing. ARM is well positioned to partner with major scalers as well GPU providers. I’m bullish on ARM’s growth prospects, particularly thanks to the adoption of v9 chips, and the growth of AI-powered PCs as well as cloud computing chips. However, the stock is overpriced and I’m initiating a “sell” rating with a one-year price target of $90 per share. I encourage investors to wait for future declines before considering ownership of the company.

ARM-based CPUs developed by Hyperscalers

To reduce dependence on NVIDIA Corporation (NVDA) and Advanced Micro Devices, Inc. (AMD), all the major companies in the hyperscaler space have developed their own chipsets for Their public cloud clients, based on the ARM architecture.

In April 2024, Alphabet Inc. announced (GOOG) (GOOGL) announced that Axion processors, new ARM-based CPUs, will be available to Google Cloud customers later this year. It’s worth noting that Axion will be built on an open architecture, and customers using ARM anywhere can easily leverage the CPU’s functionality with existing applications. Google has claimed that the new Axion chip will have 50% better performance than current Intel Corporation (INTC) processors.

As reported by the media, Microsoft Corporation (MSFT) will launch the ARM-powered Azure Cobalt CPU later this year, to serve existing Azure customers. Finally, at the end of 2023, Amazon.com, Inc. revealed (AMZN) announced the Graviton4 SoC, a 96-core ARM-based CPU, to AWS customers.

As ARM-based CPUs start to gain momentum, I expect ARM to grow its business in the cloud infrastructure market. Because ARM-based solutions provide a better balance between costs and efficiency, enterprise customers will likely prefer ARM-based solutions.

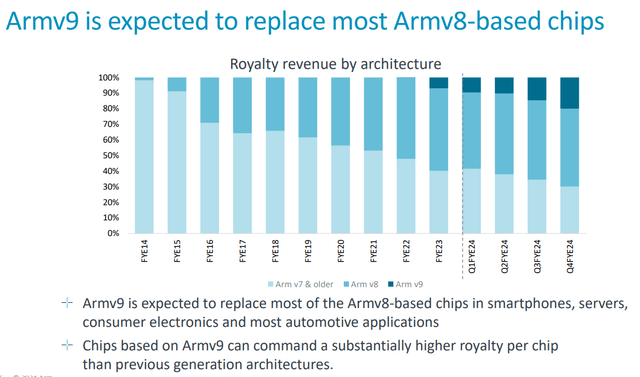

ARM v9 adoptions in the smartphone market

ARM started ramping up ARM v9 as of FY23, and the company expects a strong upgrade/conversion from v7 and 8 in the coming years, as shown in the chart below.

ARM Investor Presentation

I expect the ARM V9 to gradually gain market share in the consumer electronics and automotive markets for the following reasons:

- In the premium smartphone market, ARM is rapidly accelerating its move towards a 9th edition solution. ARM v9 has already been certified by several smartphones including the Samsung Galaxy S24, Google Pixel 8, Vivo X100, and X100 Pro. As today’s smartphones run more applications, these phones require fast CPUs for computing power. ARM’s Cortex-A725 can provide 35% more efficiency than Cortex-A720, and it is quite reasonable for the rapid adoption of the new ARM chip.

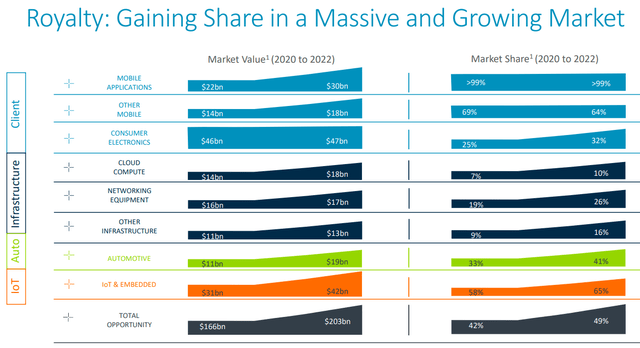

- ARM dominates the consumer smartphone market, powering almost every phone globally, as shown in the chart below. Since ARM has such a high market share in consumer electronics markets, smartphone vendors are unlikely to change their technology roadmap and risk adopting other technologies.

ARM Investor Presentation

Latest results and outlook for FY25

ARM released its Q4FY24 results on May 8, with record growth in royalties and licensing revenues. More specifically, its revenue grew 46.6% year-over-year and its annual contract value (ACV) rose 14.8% year-over-year.

My biggest takeaway during the quarter was that ARM continued to benefit from v9-based chip adoption and market share gains as more hyperscalers adopt ARM-based server chips.

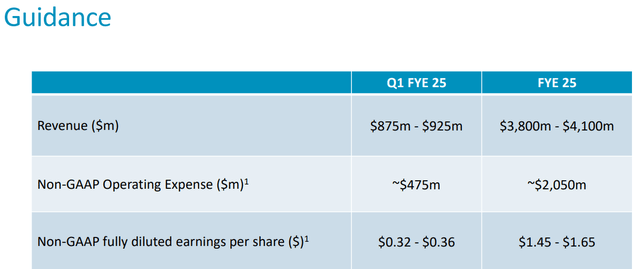

For fiscal year 2025, the company expects 17% to 27% growth in revenue, as detailed in the table below:

ARM Investor Presentation

As for its near-term growth, I consider the following factors:

- Research and Markets expects the smartphone processor market to grow at a CAGR of 16.7% from 2023 to 2028, driven by the adoption of 5G networks, AI computing and the Internet of Things. In the era of AI computing, smartphones are likely to integrate AI chips to enhance computing power and improve efficiency. Given ARM’s dominant position in the smartphone processor market, I expect ARM to continue to lead the market in the future.

- For the equity business, ARM should be able to develop its own v9-based chips as discussed previously. The adoption of version 9 helped ARM to further penetrate the smartphone and automobile market.

- As reported by the media, Nvidia is preparing AI PC chips that connect ARM’s Cortex-X5 core with Nvidia’s Blackwell architecture. If so, Nvidia could enter the market dominated by QUALCOMM Incorporated (QCOM) in ARM-based Windows systems. ARM will likely generate some additional revenue from its Cortex+Blackwell combination of offerings.

Overall, near-term growth could be driven by ARM v9 adoption, ramp-up of hyperscale products as well as the potential growth of AI PCs, in my view. I expect ARM to achieve revenue growth of over 30% in the near term, assuming 15% growth from smartphone processors, 10% growth from PC processors, and 5% growth from other end markets like automobiles.

evaluation

Canalys predicts that 19% of computers shipped in 2024 will be able to use AI, rising to 60% by 2027, with a strong trend toward commercial adoption. Strong adoption of AI-powered personal computers would create a long-term growth engine for ARM. It is very likely that ARM will continue to lead the PC processor market in the future.

However, it is almost impossible for ARM to maintain a growth rate of more than 30% for many years, as the company expands. In the DCF model, I assume that its growth rate will slow from 30% to 25% from FY28, then to 20% from FY31, and to 15% from FY33, which is a reasonable growth path for a high-growth company.

ARM used to generate an operating margin of 25% due to its royalty and licensing business model. The company hired several engineers to enhance its R&D capabilities in FY24, causing an increase in stock-based compensation as well as R&D costs. I will discuss it further in the risks section. As the company expands its AI PC business, I expect the company to generate operating leverage from SG&A and R&D costs, resulting in 270 basis points of annual margin expansion, according to my calculations. In the model, I assume that its operating margin will reach 39.5% by fiscal year 2034, which is a very reasonable margin level for a semiconductor company.

ARM DCF – author’s calculations

I calculate free cash flow from equity as follows:

ARM DCF – author’s calculations

The cost of equity was calculated at 16.8% assuming: a risk-free rate of 4.2% (10-year US Treasury yield); Beta 1.8 (author’s calculation based on historical stock price); Equity risk premium of 7%.

Discounting all future FCFE, the one-year price target is calculated to be $90 per share. The stock is trading at over 110x its forward payout. Free cash flow, which I think reflects enormous and unrealistic optimism about future growth from AI. However, ARM is not the same as Nvidia, and the processor market is unlikely to see the explosive growth that GPUs have seen over the past few years, as ARM’s growth is largely tied to the overall smartphone and PC markets.

Main risks

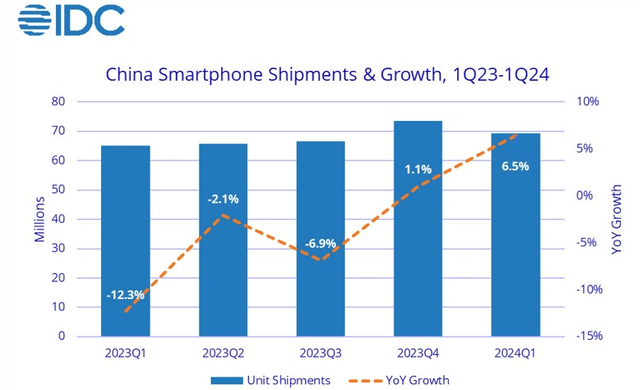

- Exposure to China: China represents 21% of ARM’s total revenue, mostly from its smartphone equity business. The growth of ARM’s business in China will be linked to the Chinese smartphone market. According to IDC, smartphone shipments in China have seen sluggish growth in recent quarters, as shown in the chart below. The rapid penetration growth in China’s smartphone market has already passed. I expect the domestic smartphone market to witness slow growth in the near future, mostly driven by smartphone alternatives.

IDC report

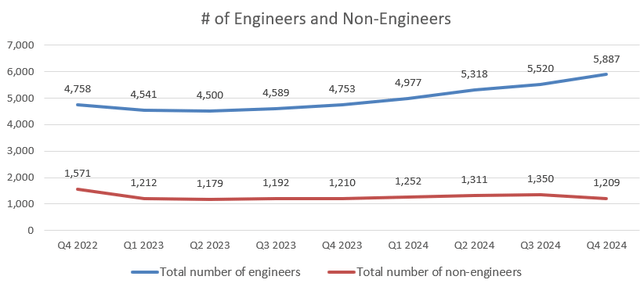

- High Stock Options: ARM allocated 32.1% of total revenue to stock-based compensation (SBC) in FY24, which is very high compared to other technology companies. ARM added more than 1,100 engineers in FY24, as shown in the chart below, putting significant pressure on small business expense (SBC) costs. Investors need to pay attention to SBC moving forward.

ARM quarterly results

- SoftBank Ownership: SoftBank Group Corp. (OTCPK:SFTBY) represents approximately 88.1% of ARM’s total issued and outstanding common shares. As an investment company, SoftBank could begin selling/reducing its stakes in the future, which could cause near-term headwinds to ARM’s stock price.

Conclusion

Although I am optimistic about ARM’s future growth in the PC and AI smartphone markets, I believe its current stock price reflects unreasonable expectations for future growth. I encourage investors not to follow the herd and be patient with the stock. Therefore, I’m initiating a “sell” rating with a one-year price target of $90 per share.