Thomas Barwick

Elevator pitch

I am modified Atour Lifestyle Holdings Limited (NASDAQ:ATAT) as a contract.

Previously, I wrote about data related to Lunar New Year holiday travel and related readings for ATAT’s mainland Chinese hotel business in my February 21, 2024 article.

for me The current update focuses on Atour Lifestyle’s Q1 2024 financial results which were recently announced on May 23. I have chosen to keep my current Hold rating for ATAT unchanged. Although the revenue outlook for Atour Lifestyle’s hotel and retail businesses is favourable, I have concerns about the increase in the company’s selling and marketing costs and uncertainty about future return on capital.

The growth outlook for the core hotel business is positive

ATAT’s top line grew significantly by +90% year-on-year to reach CNY 1,468 million in Q1 2024 as revealed in its earnings call. The company’s latest quarterly revenue Beats sell-side analysts’ expectations of CNY1,370 million by +7%.

Atour Lifestyle’s revenue generated from its hotel business, including managed hotels and leased hotels, increased +58% year-on-year to RMB1,004 million. The core hotel business contributed 68% of the company’s most recent first-quarter total earnings.

In my view, ATAT’s core hotel business is likely to continue to record strong revenue growth in the future, considering two key factors.

The first key factor is that Atour Lifestyle’s hotel business has scope for further revenue expansion considering the mix of travelers and a potential recovery in business travel demand.

In a June 27, 2023 research report by Chinese research firm CMB International, it was noted that ATAT boasts a “higher sales mix from business travelers” versus leisure travelers.

In its Q1 2024 earnings call, Atour Lifestyle noted that “experience-based leisure tourism during holidays and weekends maintained its growth momentum” and also stated that “business travel recovery was relatively weak due to macro uncertainty.”

In other words, ATAT was able to grow its hotel business revenue in a significant way and achieve a +7% higher profit in Q1 2024, even though business travelers have not returned in a significant way. As such, it is realistic to believe that Atour Lifestyle’s hotel business could see an acceleration in revenue growth in the future if demand for business travel improves in the future.

The second key factor is that the company’s Atour Light brand has positive growth prospects.

In its FY2023 20-F filing, ATAT refers to Atour Light as a “mid-sized hotel brand” focused on “young urban travelers looking for the best value and experience” and which introduced the “refreshed hotel model” Atour Light 3.0 in February of last year.

Atour Lifestyle highlighted in its Q1 2024 earnings presentation slides that it recently rolled out “special platinum perks (for members)” and “joint collaborations with a fashion apparel brand” to differentiate Atour Light 3.0. ATAT’s efforts have paid off, with Atour Light 3.0 contributing more than 15% of recent quarterly new signings in the hotel sector. Looking to the future, the company’s goal is to increase the number of Atour Light 3.0 hotels from 36 hotels as of the end of the first quarter of 2024 to 100 hotels by the end of this year.

Retail is a major driver of growth

Atour Lifestyle noted in its fiscal 2023 20-F company filing that its retail business sells private-label products “sleep-related” and “personal care and fragrance” to travelers staying at its hotels.

Retail and other businesses accounted for 28% and 4% of Atour Lifestyle’s most recent quarterly revenue, respectively. Apart from the core hotel business, ATAT’s other major growth driver is its retail business. Revenue and gross merchandise value (GMV) of Atour Lifestyle’s retail business increased +269% YoY and +277% YoY to CNY417 million and CNY495 million respectively in 1Q24.

ATAT has revised its top-line growth guidance for the full year of fiscal 2024 from +30% previously to +40% now, as part of its Q1 2024 results release. Atour Lifestyle explained in its Q1 2024 results summary that “outstanding performance in the quarter the first, Especially in our retail business (my emphasis)“It was the primary reason for the upward revision in revenue guidance.

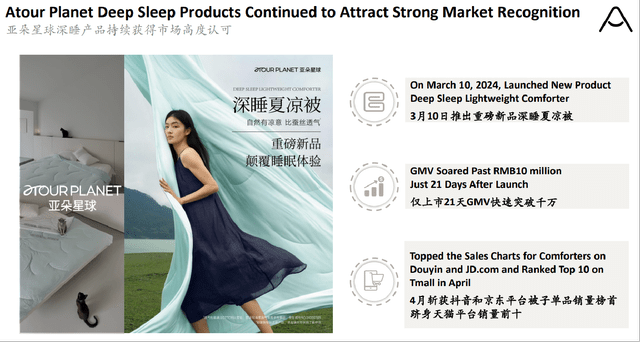

An overview of the retail business’s new offering known as ‘Lightweight Comforter for Deep Sleep’

Atour Lifestyle Q1 2024 Results Presentation Slides

As shown in the chart above, the retailer’s latest offering called the “Deep Sleep Lightweight Comforter” recorded strong sales on leading Chinese online platforms last month. Going forward, ATAT revealed in its recent quarterly analyst call that the retailer will “launch its next generation deep sleep pillow or deep sleep temperature control duvet in the coming quarters.”

The positive growth momentum of Atour Lifestyle’s retail business is likely to continue thanks to strong new product launches.

The sharp increase in selling and marketing costs is a concern

In contrast to the company’s impressive Q1 revenue increase of +7%, ATAT’s Q1 EBIT margin of 22.11% was -36 basis points below consensus expectations of 22.47% (Source: Standard & Poor’s Capital IQ).

Atour Lifestyle’s operating profitability for the fourth quarter may have been below expectations due to a significant increase in the company’s selling and marketing expenses.

In specific terms, ATAT’s selling and marketing costs jumped +212% year-on-year from CNY56 million in the first quarter of 2023 to CNY175 million in the first quarter of this year. The ratio of selling and marketing costs to sales increased +4.7% percentage points year over year from 7.2% for the first quarter of 2023 to 11.9% for the fourth quarter.

ATAT cited “enhanced investment in brand recognition” as a key reason for the significant rise in selling and marketing expenses during the latest quarter. Therefore, there are good reasons to be concerned that higher-than-expected investments and expenditures could impact ATAT’s financial performance in the future.

Uncertainty about the future return of shareholders’ capital

Return on shareholders’ capital is a key investment consideration for two reasons. First, companies that actively return capital to shareholders are usually more disciplined regarding capital allocation due to the need to allocate capital for buybacks or dividends. Second, stock buybacks and dividends can provide investors with fixed returns that are not affected by market fluctuations and stock price movements.

In the case of Atour Lifestyle, the company does not pay regular recurring dividends and does not have an active stock buyback program.

One sell-side analyst asked whether “management has any plans regarding returns to shareholders” in the company’s last earnings briefing on May 23. In response, ATAT highlighted that it had “declared a one-off dividend” in August 2023 and “will consider plans to increase shareholder returns, including dividends.” However, the company stopped short of providing specific details regarding potential capital return initiatives to shareholders in the future.

In short, there is uncertainty regarding Atour Lifestyle’s capital return approach and future moves.

Final thoughts

My decision is to maintain a Hold rating for Atour Lifestyle after analyzing ATAT’s revenue, expenses and shareholder capital return.

The market is now valuing ATAT with a consensus EV/EBITDA ratio for the next 12 months of 9.7x (Source: Standard & Poor’s Capital IQ). This is relatively lower than their peers Shanghai Jinjiang International Hotels (600754:CH) and BTG Hotels (600258:CH) EV/EBITDA multiples of 10.0 times and 11.2 times, respectively.

But I think Atour Lifestyle deserves some form of valuation discount given the approach and size of its shareholder capital return. ATAT does not pay a dividend, unlike Shanghai Jinjiang International Hotels and BTG Hotels. Also, the volume of Shanghai Jinjiang and BTG hotels is about five times that of Atour Lifestyle based on the top line of the respective company’s last fiscal year according to Standard & Poor’s Capital IQ Data. Therefore, I see Atour Lifestyle’s ratings as reasonable and the stock warrants a Hold rating.