Khanshit Khirisuchalwal

Written by Robert Carnell

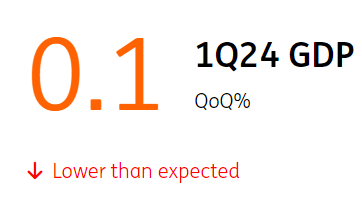

GDP for the first quarter of 2024 was weaker than expected

At just 0.1% QoQ, the Q1 2024 GDP result continues a remarkably steady deceleration in sequential growth since Q4 2022, when GDP grew at a rate of 0.8% QoQ. there was An upward revision to growth figures for the fourth quarter of 2023, which now show growth of 0.3%, up from the initially reported figure of 0.2%. But the year-on-year growth rate still fell to 1.1% year-on-year, and further declines are likely in the coming quarters.

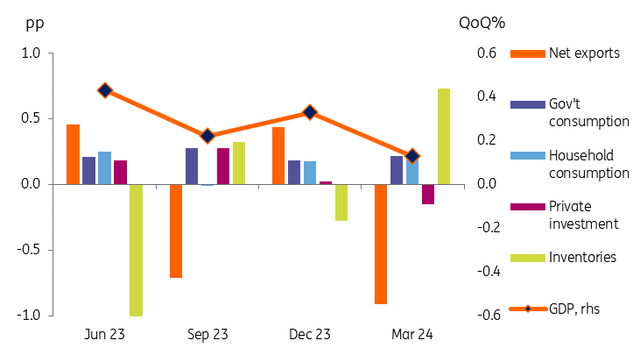

Contributions to GDP on a quarterly basis (pp)

Low fixed investment

Although the net exports number was a much bigger drag this quarter (-0.9 bps) than it was in Q4 2023 (+0.4 bps), we need to consider net exports alongside inventories. , where a significant amount of import withdrawal appears as a compensatory increase in inventories. When we do this, the combined inventory/trade contribution has declined from a positive 0.1 basis point increase in 4Q23. To withdraw 0.2pp in 1Q24.

Household spending growth provided a continuing, albeit small (0.2 percentage point) boost to GDP. Household consumption remains weak, but it is not collapsing.

Private fixed investment was the most obvious reason behind the slowdown in the last quarter. Investment did not provide any impetus to growth in the fourth quarter of 2023 and deteriorated to a decline of 0.2 basis points in this quarter.

Until interest rates start to fall, investment prospects in Australia remain rather bleak. With inflation remaining more stable than would be ideal, the prospects for any cuts this year look bleak.

We removed the last remaining rate cut from our forecasts this month, and now await more inflation data to consider how long the first cut will take place in 2025, or even if we need to consider further increases.

This is not an ideal situation for the Reserve Bank of Australia (RBA). The Reserve Bank of Australia will take economic and labor market activity into account when setting policy. But ultimately, if growth weakens, but inflation starts to rise again, it will be difficult for the RBA to look the other way and leave interest rates as they are. It will take inflation slowing – and soon – to dispel notions that interest rates may not have peaked yet.

Content Disclaimer

This publication has been prepared by ING for information purposes only without regard to a particular user’s means, financial situation or investment objectives. The information does not constitute an investment recommendation, nor is it investment, legal or tax advice or an offer or solicitation to buy or sell any financial instrument. Read more

Original post