James O’Neill

introduction

Utilities have been out of favor for a while now. In a recent article, I looked at another utility with a growing renewables portfolio and laid out the reasons why I believe in Northland Power (NPI:CA).) was a compelling buy in the space. Today, I’ll be taking a look at a smaller company, Avista (New York Stock Exchange: AFA), highlighting why I’m optimistic about the name. While the long-term thesis on renewables is the same, Avista in particular has seen growth in margins and ROE, and the rate rule over time should lead to additional EPS growth. With a strong balance sheet and secure earnings, Avista makes an attractive investment in the utilities sector.

Company overview

Avista is primarily a regulated corporation that holds an interest in the operations of regulated utilities in the Pacific Northwest where it provides electricity distribution and moving to eastern Washington and northern Idaho. In addition, it also distributes natural gas in Oregon and has power generation facilities throughout Washington, Idaho, Oregon and Montana. Avista also supplies electricity to a small number of customers in Montana. And finally through him CompanyAvista, an Alaska energy and resources company, provides retail electricity service in the city and suburb of Juneau.

Investor presentation

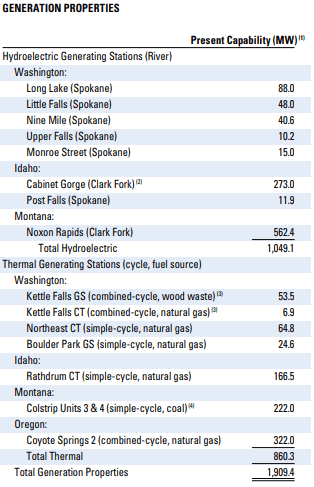

One of the reasons you like Avista is because of its renewable energy business. Of its total operations, 48% is hydropower, 9% is wind power, and 2% is biomass. But the company also owns 33% natural gas and 8% coal, which provides some diversification. As for generation characteristics, Avista has 1,049 MW of current hydropower capacity and 860 MW of thermal capacity.

Annual report 2023

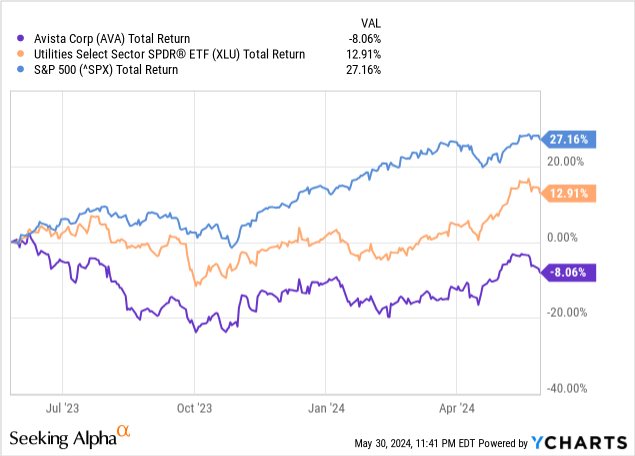

Avista shares have performed poorly over the past year, generating a total return of -8.1%, compared to the S&P500’s return of +27.2%. With a dividend yield of 5.3%, the decline was mitigated by dividends to shareholders. Additionally, Avista’s negative total return over the past 12 months also lags the Utilities ETF (XLU) at +12.9%.

Why the poor performance? Avista, like most utilities, has been under pressure recently as rising interest rates to combat inflation are impacting utility companies. There are two influences driving this trend.

First, utilities are generally considered leveraged companies, choosing to borrow due to the low return on assets generated by their facilities. They are able to leverage leverage because demand from electricity transmission and distribution tends to be very stable and predictable, with not much variation in cash flow from year to year. When interest rates rise, the cost of debt when refinancing means that its interest expenses rise, despite often generating the same revenues, so higher expenses versus stable revenues have a net negative effect on them.

Second, when interest rates rise, from an investor’s perspective, it often becomes more attractive to buy safer, fixed-income investments rather than to buy utilities, which are generally viewed as riskier (stocks). Given this, as interest rates rose, investors were selling utilities.

Finance and forecasts

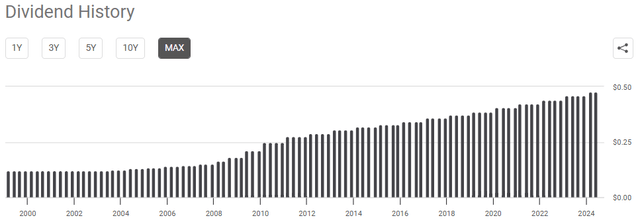

One of the reasons I like Avista (something I think is underappreciated by investors regarding the company) is its track record of consistent earnings growth over time. Over the past 21 years, the company has paid increasing monthly dividends to shareholders; A proven track record that is very rare in the facilities industry. With a growing dividend, you would probably expect that the company would pay out nearly all of its earnings per share as dividends, however, the payout ratio is 76%, so the dividend appears to be well covered. This should provide some earnings insulation as well as comfort for investors, knowing that the company will likely continue to grow its dividend, even if earnings per share remain flat for a few years.

Earnings history (Searching for Alpha)

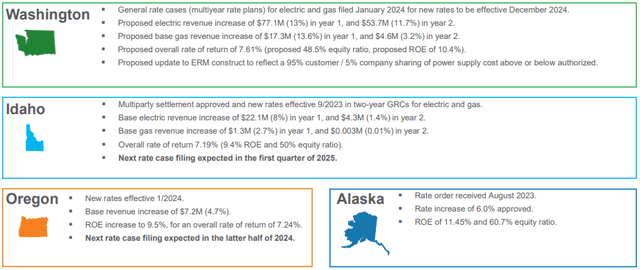

But from my point of view, I do not think that earnings per share will remain constant. In fact, Avista has been quite clear about why that shouldn’t happen. Given approximately half a billion capital expenditures annually, the underlying growth rate should continue to grow at 5% through 2026. With strong equity returns allowed across the four geographies (10.4% in Washington, 9.4% in Idaho, and 9.4% in 5% in Oregon, 11.5% in Alaska), and especially in Alaska, the regulatory environment is surprisingly favorable with multi-year rate plans that insulate the company’s cash flows.

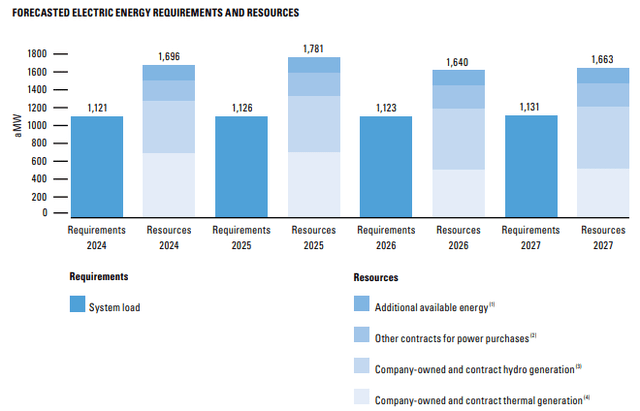

We can also see that the company has been proactive in keeping its resources ahead of requirements to meet demand, regardless of operating conditions. Average hourly load was 1,115AW in 2023, 1,142AW in 2022, and 1,113AW in 2021.

Annual report 2023

With a market capitalization of US$2.84b, long-term debt of US$2.60b, and cash of US$12m, Avista’s implied enterprise value is approximately US$5.42b. Its debt-to-enterprise value ratio is 48%, which is in line with other peers. Trailing twelve-month EBITDA is $550 million, so total debt to EBITDA is 4.7 times, down from a high of 6.3 times two years ago ( Source: S&P Capital IQ). As leverage continues to decline alongside increased earnings growth through 2026, leverage should decline slightly, barring no new growth capital expenditures.

On the earnings call, management noted that it was able to leverage $83.7 million in financing from 3.875% tax-exempt bonds, about 140 basis points below the taxable market. These cost savings should also support earnings per share growth. In addition, management also does not expect to issue more debt during the year, but merely issue stock worth about $70 million later in the year to fund capital expenditures.

Evaluation and conclusion

When looking at Avista’s 4 sell-side ratings, there are 3 “hold” ratings and only 1 “buy” rating. The average price target is $40.00, which implies an upside of ~10.6%, not including the dividend yield of 5.3%. With total returns likely to rise 15.8% over the next year, despite majority ratings, analysts see an upside with Avista.

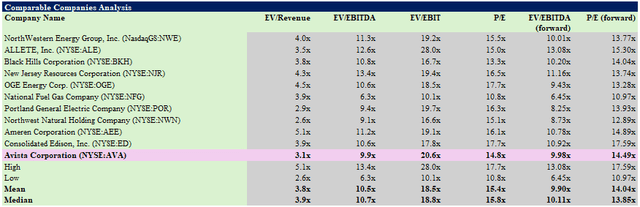

Avista trades at 9.9x EV/EBITDA and 14.8x P/E (or 14.5x forward earnings) (Source: S&P Capital IQ). Compared to similar companies, it trades at a premium of one turn to both EBITDA and earnings, so the company is roughly in line with its peer group.

Author, based on data from S&P Capital IQ

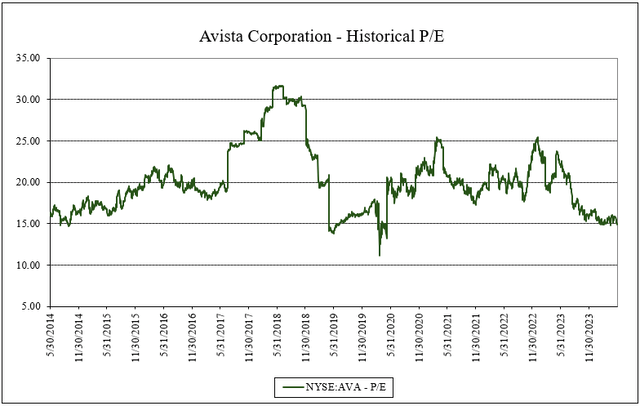

However, when comparing the company to its historical P/E, the company is trading at a discount of more than 5 cycles compared to its 10-year historical average P/E of 20.1x P/E. In my view, this is likely due to the interest rate environment, which has toppled its peers to its side.

Author, based on data from S&P Capital IQ

But if history is any indication, it’s historically been a great time to buy in this range, as Avista has rarely been this cheap. In my view, the current valuation provides investors with an opportunity to buy discounted shares. With a growing rate base, a growing renewables portfolio, strong financials, and a balance sheet that provides the company with flexibility, I believe Avista offers a combination of growth and income. There is still weakness in the sector, and this may not go away for a while until sentiment changes, however I believe that as the company continues to execute on its growth plans and leverages its diversified energy portfolio, shareholders may benefit from capital appreciation and continued stability. Income generation, especially given the track record of consistent dividend increases. I’m optimistic about Avista’s prospects and will add to the stock.