Photos by Martin Baroud/OJO via Getty Images

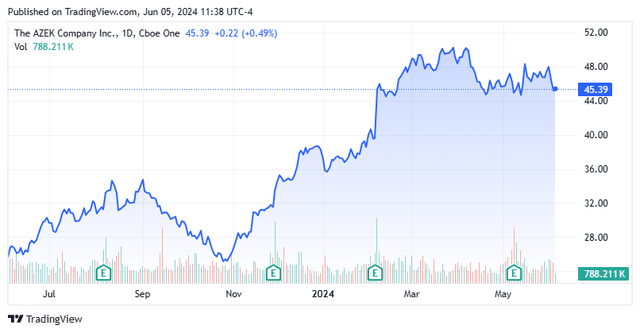

Today we put AZC Company (New York Stock Exchange: AZC) In the spotlight. This building products supplier’s stock is up nearly 80% from its lows in late October, when summer took hold The market is generally at a bottom. However, real estate still faces significant headwinds, thanks in large part to rising interest rates. There has also been a notable recent rebound in insider selling. Can stocks rise further, or is it time to take some profits off the table? The analysis follows below.

Seeking alpha

AZEK Company Inc. is headquartered in In chicago. The company manufactures and supplies various products primarily in the field of decking, railings, trim, moulding, siding and cladding. Its main markets are in the residential, commercial and industrial real estate sectors. The stock is currently trading at around $45.00 per share and has an approximate market cap of $6.6 billion. Company The fiscal year begins on the first of October. A series of acquisitions and divestitures over the past several years has enabled the company to capitalize on the recent boom in offshore living. AZC Company It was stripped Its Vycom business, which accounts for the bulk of commercial sector sales, was closed late last year.

Latest results:

AZEK Company Inc. registered Initial second quarter results On May 8th. Revenue posted an estimated 10.8% year-over-year rise to $418.4 million, about $6 million above current consensus. Net residential sales reached $402.5 million, an 18% improvement over the same period last year. Net income for the quarter is estimated at $74 million to $75 million. Management enhanced fiscal year 2024 guidance across some key metrics as well.

Mayo Company Presentation

It should be noted that on May 17, the NASDAQ rose I was informed The company said it was in non-compliance with stock exchange listing requirements because it had not yet filed a 10-Q for the fiscal second quarter. At the time, the Department stated that it would do so within 30 days of the notification date.

Analyst Comments, Inside Sales, and Balance Sheet Considerations:

The analyst community is globally optimistic about the company’s prospects currently. Since preliminary Q2 results came out, eight analyst firms, including Barclays, Jefferies and RBC Capital, have reissued/assigned buy ratings for AZEK. Price targets offered range from $49 to $58 per share.

However, insiders appear to be taking some chips off the table. Since February 12 of this year, several insiders have disposed of just over $10 million worth of shares collectively. For comparison purposes, insiders sold roughly $2.5 million in the fourth quarter of last year before the stock’s recent big rally.

The 10-Q filed for the first quarter of 2024 showed approximately $280 million of cash and marketable securities on the balance sheet versus approximately $580 million of long-term debt. Management has directed that it expects net interest expense for fiscal year 2024 to be between $34 million and $38 million. The company bought back $25 million of its own stock in the second quarter of this year as well. a company Announce Authorizing a $100 million stock buyback late last year.

Conclusion:

AZEK Company Inc. has achieved 74 cents on revenue of $1.37 billion in fiscal 2023. Current analyst firm consensus Earnings will jump to $1.19 per share in fiscal 2024 with sales rising to $1.43 billion. They see $1.39 earnings per share in fiscal 2025 with revenue growth of eight percent.

There are three current reasons why I see the rally around AZEK fading and why I don’t think the stock is worth investing here at these trading levels.

First, the uptick in insider selling and the delay in filing the fiscal second quarter 10-Q. This is a minor concern since the filing process should be completed soon and insider selling tends to spike early in the year since insiders have taxes to pay among other needs.

The second concern is greater, and relates to the ongoing challenges of construction and real estate activity in general. On the residential side, existing home sales in 2023 fell to their lowest levels since 1995. Additionally, pending home sales fell in April, reaching the lowest reading since the country was in lockdown mode in the spring of 2020. The residential side represents the largest portion of the company’s end users and revenues. Home Depot (HD) I’ve noticed a decrease in the number of DIY projects and larger home improvement projects this year. If the country enters a recession or a prolonged bout of stagflation, one of the many areas consumers are likely to cut back is on large outdoor projects.

Mayo Company Presentation

On the commercial side, most of the commercial real estate sector is experiencing problems, with increasing default and delinquency rates impacting many areas of CRE loans. The problems with the office sector are well known. However, as I noted in my last report condition around Builders FirstSource, Inc. (BLDR), That company indicated that it believes multifamily construction starts will decline by 20% to 30% in 2024 in the region that the giant construction suppliers are interested in. This stock is down over 20% since I made a sell recommendation on it on April 1st. As previously mentioned, AZEK now has very little exposure to the commercial side of the business, with Vycom being divested in the fourth quarter of last year.

Mayo company presentation

Finally, we have the evaluation. After a recent surge, shares of AZEK Company Inc. are trading… Nearly 40 times forward earnings. This is a significant premium to the forward earnings of just over 21 times the S&P 500 (SP500) trades at. AZEK’s expected earnings and sales growth over the next two years don’t seem to merit that kind of valuation.