V2images

baidu (Nasdaq: BIDU) is engaged in providing online search and online marketing solutions and is often referred to as Google (GOOG) (GOOGL) in China. It works in two parts. Baidu Basic, which is the company’s pay Per-click advertising platform, iQIYI (I.Q), which is a Netflix-style video platform. Unlike Google and Netflix (NFLX), Baidu’s revenue is entirely limited to the Chinese market, and regulatory concerns and concerns regarding the real estate market have greatly impacted market sentiment. However, the stock is now trading at a significant discount to its US peers as well as its own history, and price action across Chinese stocks and options markets suggests a potential bullish reversal.

The free cash flow yield is now around 15%.

After peaking at a market capitalization of US$93 billion in March 2021, Baidu stock is now worth just US$34 billion despite having a net worth of US$10 billion. Net cash position. With free cash flow of $3.5 billion over the last 12 months, the stock trades at a free cash flow yield of 14.5%. While free cash flow has been supported by high levels of stock-based compensation in recent years, even if we add $900 million in SBC as a cost, the free cash flow yield is still very attractive at 10.8%.

Baidu’s Free Cash Flow Return with Enterprise Value (Bloomberg)

The table below shows how cheaply Baidu stock trades compared to Google and Netflix using a number of valuation metrics. Not only is Baidu cheap on an earnings basis, it’s also now trading at a slight discount to its book value. For context, only 6 of the 30 stocks in the Hang Seng IT Index trade at a discount to book value, and no member of the S&P 500 IT Index trades at less than 1.2x book value.

| Baidu | Netflix | ||

| FCF productivity with EV | 14.5% | 3.3% | 2.6% |

| Value Added/EBITDA | 5.78x | 17.8x | 34.8x |

| Price/earnings | 11.1x | 26.4x | 44.6x |

| Price/book value | 0.98x | 7.4x | 12.9x |

It was not always the case that investors applied a heavy discount to Baidu compared to Google. In fact, since 2007, Baidu has traded at a higher price most of the time, making the current discount particularly noteworthy.

Baidu vs. Google PE ratio (Bloomberg)

The valuation discount belies the positive growth outlook

Stocks that trade at such cheap valuations usually do so because of particularly weak earnings expectations. In Baidu’s case, earnings on Wall Street are expected to grow more than 20% over the next 12 months and rise further in 2026. While 20% earnings growth seems ambitious as macroeconomic weakness continues to weigh on ad revenue, The long term outlook is positive. As this article shows, Baidu has successfully integrated AI into its core services and is well-positioned to benefit from industry developments. The company launched a paid version of its AI-based conversational product, Ernie Bot, which now has 200 million daily users, 85,000 of whom are enterprise customers. Management also recently announced that it is strengthening relationships with Apple (AAPL) and Tesla (TSLA), using Chinese data laws to grow beyond research into artificial intelligence and autonomous technology.

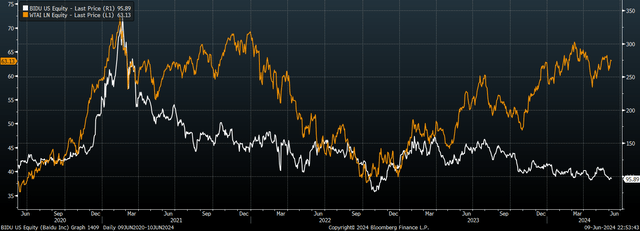

In light of these positive developments in the field of artificial intelligence, it was perhaps expected that investors would flock to the company’s shares. However, while investors have poured trillions of dollars into AI-related stocks since ChatGPT’s launch in late 2022, Baidu’s shares have weakened.

Baidu vs. WisdomTree AI Index (Bloomberg)

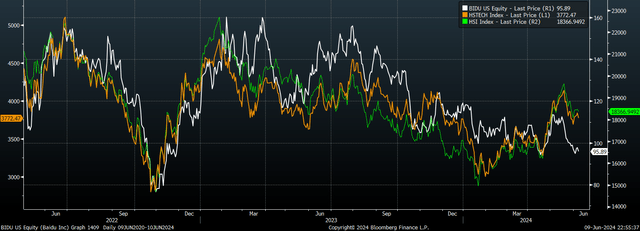

In part, this weakness can be explained by a widespread decline in investor interest in China, which has stemmed from the government’s increased regulatory scrutiny across the technology sector as well as the ongoing real estate market crisis. Baidu’s decline from its peak in 2021 has closely tracked the performance of the market in general and the performance of the technology sector in particular. However, over the past few months, Baidu shares have weakened even as the broader market and technology sector staged something of a rebound, which may indicate that the stock is about to catch up.

Baidu, Hang Seng Technology Index, Hang Seng Index (Bloomberg)

Options markets point to a strong rebound in stock prices

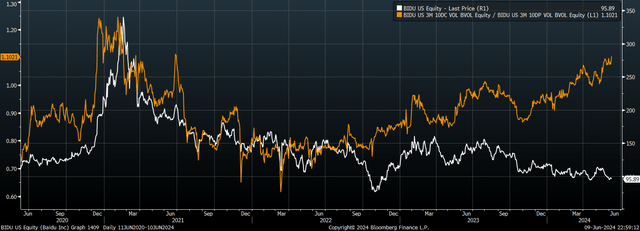

This view is supported by recent activity in the options markets, where the price of call options has increased compared to the price of put options. Options market activity has the ability to drive price movement in stocks, and as we saw in 2020, the rise in the buy/sell ratio preceded the rise in Baidu’s stock price.

Baidu stock price versus buy/sell ratio (Bloomberg)

The extremely low implied volatility of put options also allows investors to buy shares while simultaneously hedging against downward movement for a small fee in the event the range falls at $94.5. The cost of hedging is now less than 1% against any move below $90 by July 24.

Intense competition poses a risk, but growth is no longer necessary in these assessments

The biggest threat facing Baidu in the coming years comes from intensifying competition in all its business sectors and search in particular. Baidu has gradually lost search engine market share in recent years, falling below Microsoft’s Bing in terms of desktop space. Other, smaller companies are also going after Baidu, and as the collapse of Yahoo’s market share in global search in the early 2000s showed, first-mover advantage doesn’t mean much in this industry. However, at current valuations, even a managed decline in revenue and earnings could allow the stock to deliver reasonable returns given its free cash flow yield of 14.5%.

summary

Baidu is trading at valuations that imply investors expect lower profits over the coming years, which contradicts strong earnings estimates by Wall Street analysts and the company’s potential to benefit from artificial intelligence. Recent evidence of a rebound in the Chinese stock market and rising prices of call options compared to put options suggest there is increasing potential for a strong bullish reversal in Baidu’s stock price.