eye

Market racket

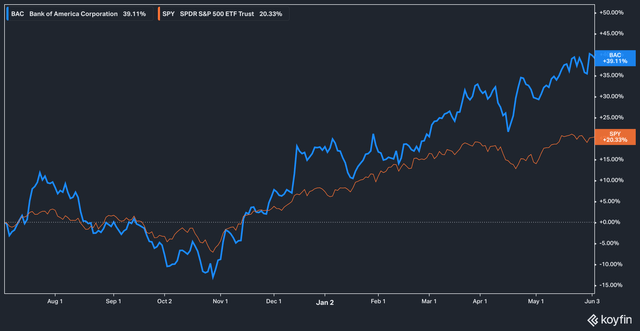

We recently covered banking giant Bank of America (New York Stock Exchange: PAC) in July 2023 (you can read this article here). At that time, we were optimistic about the bank’s prospects. During that year the bank’s shares increased It has been hammered by the regional banking crisis (remember that?) and fears that the bank (and others like it) are putting themselves at risk with huge hold-to-maturity (HTM) loan balances on their books.

But time was on our side. Since July 2023, Bank of America stock has easily outperformed the broader S&P 500 Index (SPY), generating a total return of 39% versus the index’s 20% return.

BAC vs SPY (Quevin)

So, where do we think things stand with the bank today? Does it still feel like a good time to be in, or have the boom times come and gone? Let’s dig deeper.

Valuable question

All things in investing are relative, so let’s start with valuations. When we last wrote about Bank of America, the stock was trading at less than 1x book value — what we thought at the time was an irrational valuation. Today things look a little rosier, but not much. While the stock is no longer trading below book price, the premium it carries seems a bit small compared to its peers.

BAC vs. JPM, WFC, CP/B (Quevin)

Today, Bank of America shares are trading at 1.2x trailing-month book, a relative bargain compared to JP Morgan’s (JPM) 1.9x valuation, Wells Fargo (WFC) trading just above it, and Citigroup (C) fetching behind, trading With a book value of just 0.6x.

Is this a rational assessment? From our point of view, it’s a bit skewed. While JPMorgan is unquestionably the leader in the money banking space, it’s not at all clear that Wells Fargo — which often finds itself the target of lawmakers’ wrath — is equal or equal to Bank of America.

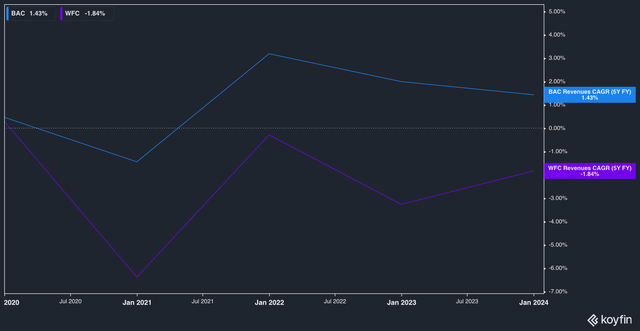

Let’s take, for example, the following chart:

WFC vs. BAC, 5-year revenue CAGR (Quevin)

While B of A only had a 5-year CAGR of 1.43% (honestly not terrible, but not great), Wells Fargo’s CAGR has been negative for some time. Although this is not the only point to make, it does illustrate our belief that the current valuation of B of A stock is slightly dislocated at the moment.

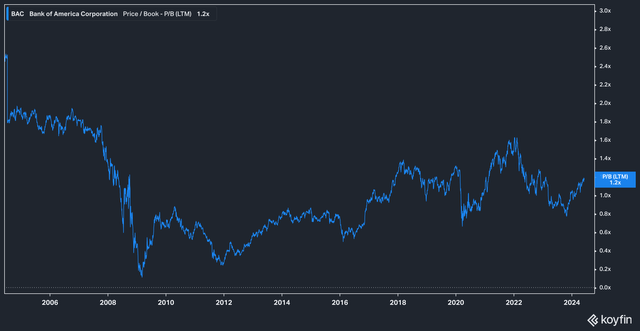

Let’s go back to the price of the book question. However, pulling the lens back a bit will allow us to get a better perspective on where the bank rate to book valuation currently lies.

BAC price per book 20 year chart (Quevin)

On the eve of the Great Financial Crisis, Bank of America was trading between ~1.6x-1.9x P/B on a trailing basis. The devastation of the global financial crisis sent the stock price plummeting, taking it down to an incredible 0.1x (yes, you read that right), a bookable price. Since then, the stock has been unable to achieve its previous highs, for several reasons. Increased regulatory scrutiny, for example, coupled with the introduction of the Fed’s ZIRP policy, has made it difficult for banks to make the same kinds of profits they did before, while at the same time discouraging investors from seeing large, money-center-focused banks as attractive banks. . Investments they have made before.

Against this historical backdrop, we see Bank of America stock as still undervalued — or at least inexpensive when viewed against the post-Global Financial Crisis valuation range the stock has seen.

Are consumers starting to crack?

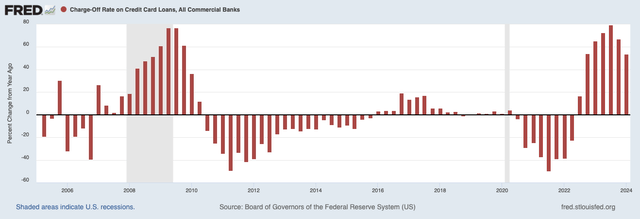

Much has been made of the fact that consumer credit card debt has ballooned to all-time highs over the past two years, largely due to rapid interest rate hikes by the Federal Reserve that have naturally seeped into the consumer lending sphere.

All of this has raised fears among investors that the American consumer will begin to collapse under the pressure, and eventually exhaust its collective ability to service all this debt. There was cause for concern — interest rates on credit card loans (balances that banks write off as bad) have jumped significantly over the past year.

However, when we pull the lens back to observe a broader historical perspective, things are not as bad as they seem.

Discount rate on credit card loan fees from Commercial Bank, percentage change from the previous year (unique)

The year-over-year percentage change in credit card loan charge-offs over the past four quarters has not exceeded the speed of change seen in the global financial crisis. In fact, it is the weak comps on which 2023 and 2024 are judged that make the numbers look worse than we think – on an absolute basis, the peak shipping rate during the global financial crisis was 10.5% (in Q4 2009). ). In the first quarter of 2024, it was 4.4%, which is a more manageable number.

Brian Moynihan, CEO of Bank of America, addressed this fear at Bernstein’s annual Strategic Decisions conference at the end of last month. Here’s what he had to say to an analyst’s question regarding the state of consumer credit:

So the concern was, are you normalizing and will it depend on the consumer side in terms of deviation and irregularities in that? And so if you look – and it was happening everywhere. You see the trust data, all the things that you guys look at, as well as the quarterly reports, and you’ve seen that. And what we’re seeing is that the 5- and 30-day delinquencies have come back, and they’ve been resolved. And so we’re very comfortable that with our customer base in cards, at the end of the day, cards are leading the entire savings line now just because of their dynamics.

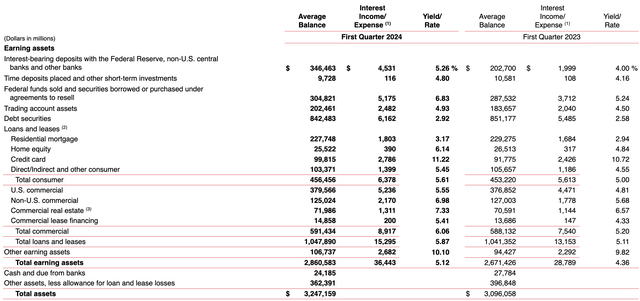

This is not a trivial matter. Credit card lending is one of the bank’s most profitable businesses. Consider this snapshot of the bank’s lending assets from the company’s most recent 10th quarter:

BAC Origins (company files)

The image above shows that consumer credit card lending makes up nearly $100 billion in consumer B loans out of $456 billion. It’s also the company’s most profitable form of lending by a wide margin, with a yield of 11.2% — nearly double the bank’s second most profitable line of credit, home equity.

The risks facing our thesis

The main risk we see in Bank of America’s thesis (and banks in general as investable businesses) is the eventual implementation of the “endgame” Basel III regulations, which every major US bank CEO has strongly opposed and which may have only been partially implemented. It is useful for financial sector investors to familiarize themselves with these regulations and understand the basics of what the new regulatory regime may mean for the global banking system. In our view, further interest rate hikes would be next on the list, which could increase pressure on consumers, but we see this possibility as far-fetched as of now.

Bottom line

We believe Bank of America’s upward trajectory is likely to continue – deposit flight is no longer the concern it was just a year ago, and returns on assets (such as consumer loans) are rising significantly. Even an interest rate cut should not have a negative impact on the bank, because a more flexible monetary environment generally encourages lending. However, at the end of the day, we remain optimistic about Bank of America’s outlook.