Apploquin

American bank (New York Stock Exchange: PAC) she is one from Main Retail banks in the United Statesthrough They were able to create their four business segments $93.359 billion In TTM revenue, $25.028 billion in net income, and Uniform amount of $293,552 Billion dollars in total equity. this Resulting in a market cap of $312.50 billion And a 2.35% TTM Dividend Yield.

In this analysis, I will review Bank of America’s earnings development, outlook, risks and valuation to decide on a Buy rating on the stock despite its impressive value. 18.68% The rise in prices since the beginning of the year has outperformed the S&P 500, Nasdaq 100, and the US Banking Index.

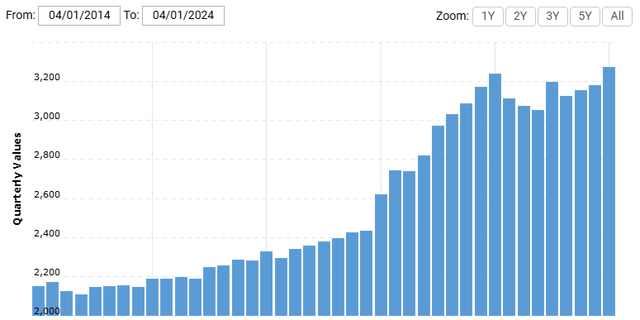

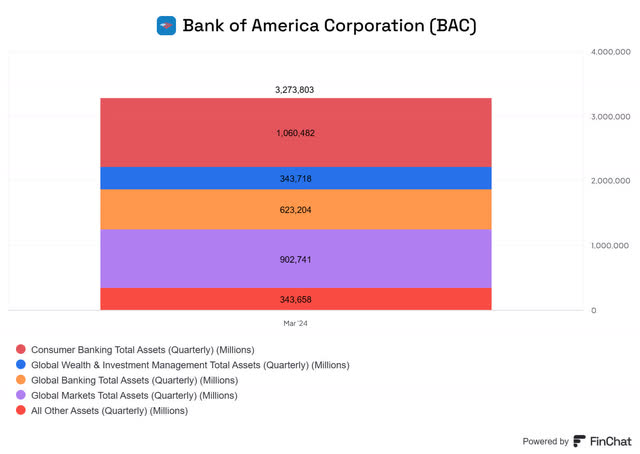

Growth of Bank of America’s assets

Total assets of Bank of America (macro trends)

Because of quantitative easing, the BAC did this He was able To grow quickly Its origins during the pandemic And now sitting in $3,274 Trillion In total assets. Hence, consumer banking and global markets are the main asset holders (which does not necessarily translate into revenue), followed by global banking, global wealth management and investing, as shown in the bar chart below.

com.finChat

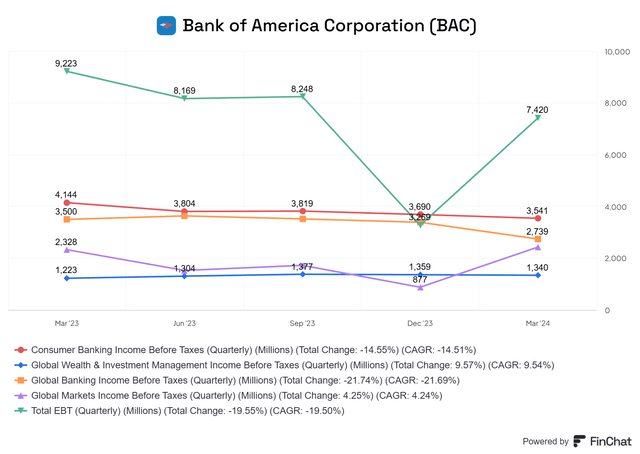

BAC Earnings

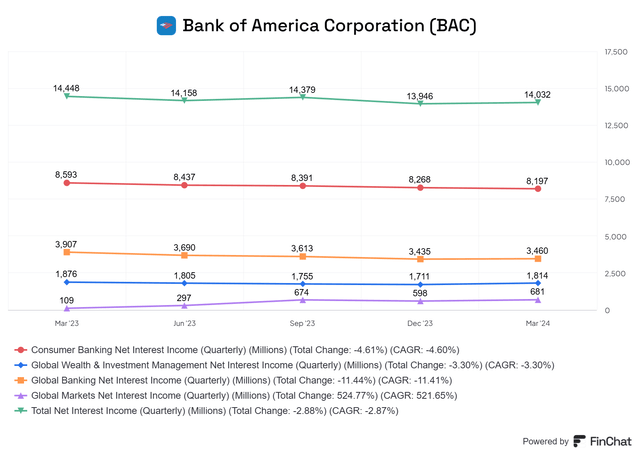

Net interest income (finches)

When it comes to BAC’s net interest income, Generally All sectors of the bank faced declines compared to last year, mainly due to appreciation Borrowing costs. In the case of consumer banking, the National Insurance contribution was reduced by $396 million, following a -7.2% decrease in average deposits and a 358.3% increase in the interest rate paid on deposits, starting from 0.12% In the first quarter of 2023 to 0.55% in the first quarter of 2024.

At the same time, global banking showed downward momentum in National Insurance despite deposit growth of 7% from the first quarter. although Main The contributor to global banking revenue is net interest income, as is non-interest income from investment banking fees as well Important contributed to this segment’s revenues and helped partially offset the overall decline in global banking revenues of -4%.

Now, when all National Insurance from all sectors are combined, the trend has declined every quarter over the past year. However, the overall decline of -2.88% is much smaller than the decline seen in the core national insurance sector, Consumer Banking.

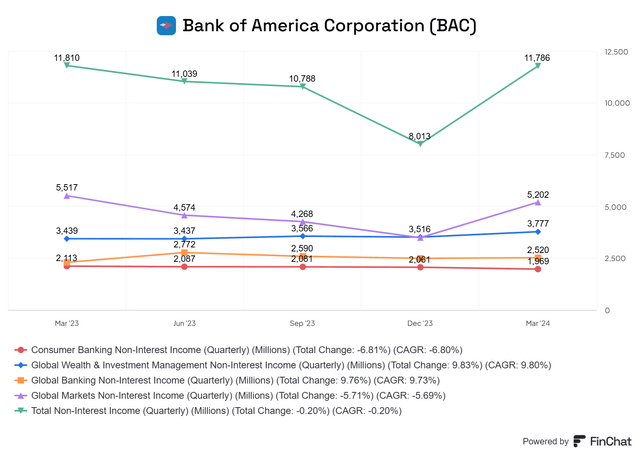

Income other than interest (finches)

On the non-interest income side, global markets saw a significant jump of 48.0% from the previous quarter due to strong sales and trading revenues, particularly in FICC sales. The non-interest income sector is still -5.7% lower than a year ago, but the reversal is more pronounced based on the image above.

Global Wealth and Investment Management saw a year-on-year increase of 9.8% after benefiting from strong inflows and generally higher asset valuations, resulting in record revenues despite lower net interest income. Finally, retail banking was the only sector to see a year-on-year decline in net interest and non-interest income.

Now, when adding all the sectors together, the bank saw a marked improvement from the previous quarter and finished near the level seen a year ago. For comparison, Wells Fargo an act be seen that Important Non-interest income increased with a significant growth of 16.8% like commented in my last analysis of they.

EBT (finches)

From the pre-tax income contribution of each segment, it can be seen that the momentum in FICC revenue helped the Global Markets segment grow EBT on a quarterly basis at an impressive rate of 176.7%. In contrast, global consumer banking and bakery pre-tax earnings showed some weakness after falling in almost every quarter of the past 12 months.

Overall, the bank’s total GAAP pre-tax profit was up significantly from the previous quarter, following a 101.1% increase. However, this comes with a caveat, as with both Q4 and Q1 There were materially unusual expenses that affected the bank’s profitability, such as a special assessment by the FDIC of uninsured deposits to fail Banks like Silicon Valley and Signature. This evaluation resulted in non-interest expenses of $2.1 billion In the fourth quarter and $700 million in the first quarter. However, even when those expenses are excluded from pre-tax profit, quarter-on-quarter growth remained flat High By 40.0%.

Bank of America 2024 Forecast

Although Bank of America is a well-diversified bank and has components of revenue that could mitigate National Insurance declines, at this point, lower interest rates will allow it to generate higher loan demand, particularly in loans that have significantly shrunk in the portfolio. . This is amazing like Residential mortgages.

September 2024 – Target Price Possibilities (CME FedWatch Tool)

this week both of them The Bank of Canada and the European Central Bank have begun a cautious cycle of interest rate cuts after keeping them at record levels for nearly a year in both cases. And with this The possibility that the Fed will start The interest rate cut in September increased depending on how interest rate futures traded. currently, the Likely A downward movement of 25 basis points stands at 58.0%, when this same measure was at 45.1% one week ago. Meanwhile, the odds of holding next week’s meeting and the one at the end of July remain low 2.5% And 20.1%.

Despite interest rate cuts by the European Central Bank, inflation expectations for 2024 rose from 2.3% to 2.5%, making the market believe that despite the start of interest rate cuts, they are likely to maintain a restrictive policy by holding interest rates above Neutral rate.

Meanwhile, if things do not unfold, these interest rate cuts would allow the yield curve to become steeper as short-term interest rates fall, and long-term interest rates will naturally rise as a result of the combination of higher long-term inflation expectations. A steeper yield curve is the ideal scenario for a bank as the spread widens from the rates at which it borrows and lends, or maturity shifting. But currently, the 2- to 10-year spread has been reversed for 482 business days, and so far, it has not acted as an early indicator of a recession.

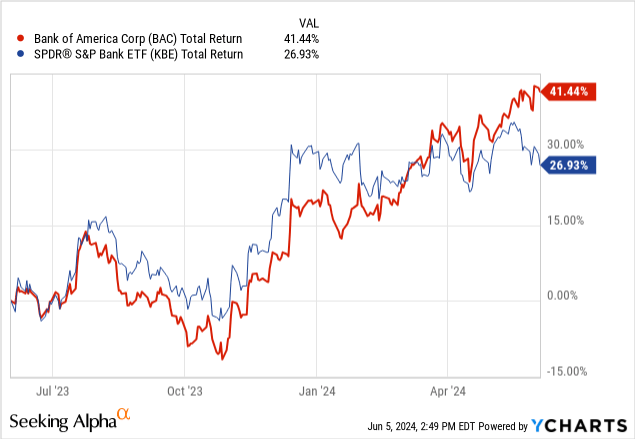

BAC stock performance

Bank of America stock has performed admirably. Over the past year, the stock has gained 41.4% in total return, outperforming its natural benchmark, S&P Bank (KBE) by 14.5%. This was also the case for other major US banks such as Wells Fargo (WFC), Citi (C), and JPMorgan (JPM), all of which posted gains around the 40% total return level last year.

The performance of all of these banks has benefited from essentially the same reason. For example, in general strong The credit quality (along with CRE) of loans, supported by the falling unemployment rate, and expectations of interest rate cuts that would allow these banks to reduce the cost of funding, boosting demand for loans. At the same time, these banks benefited from a rebound in non-interest activities in investment banking and asset management due to rising equity valuations and deal activity.

Bank of America stock valuation

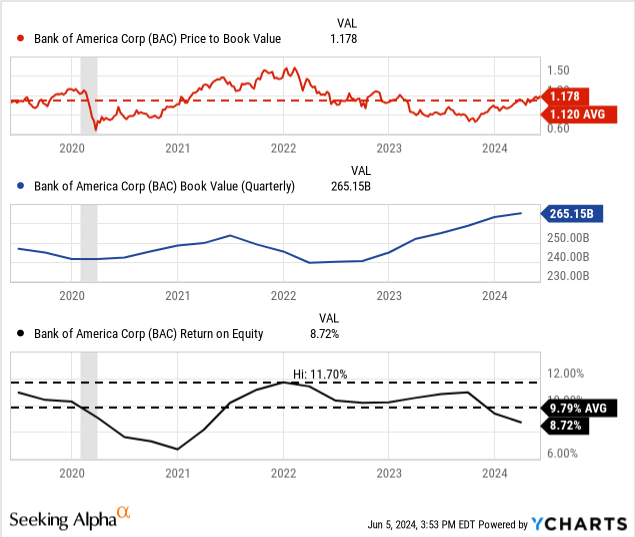

On the valuation side, based on the five-year historical average, the price-to-book multiple sits at its historical average above book value of 1.12x. And in November last year, even Bank of America I got the trade At a multiple of less than the book value 0.77x. now that it several It has expanded significantly, but not to the point that we would consider it exaggerated.

One element that helps justify the price to book is return on equity. From there, the company offers a return on equity of 8.72%, which is slightly below average, making it less attractive. However, as net income improves in the future through improved interest margins and higher loan demand, I see this ratio increasing in the future, which will likely lead to an expansion of the syndication partnership.

Finally, a bank’s growth can be measured by growth in book value, and in the case of Banque du Caire, it has grown unabated every quarter since the first quarter of 2022, representing a cumulative growth of 10.72% since that date to become a positive sign for investors.

Bank of America Dividend Discount Form

| Discount rate | Risk-free rate | Beta | Equity risk premium |

| 8.89% | 4.28% | 1.12 | 4.12% |

| growth rate | Return on shareholders’ equity | Retention rate | |

| 6.85% | 9.79% | 70.01% | |

| Profits 1 | FY24 dividends | FY25 dividends | |

| $1.04 | $1 | $1.07 | |

| Upside down | price | Intrinsic value | |

| +26.93% | $39.96 | $50.72 |

Moving to the second valuation method, based on a one-period dividend discount model, BAC shares appear undervalued with an upside of 26.94%. For the model inputs, I calculated a cost of equity of 8.89%, a growth rate of 6.85%, and a weighted average of expected dividends for FY24 and FY25 which resulted in The numerator is $1.04. Hence the intrinsic value stood up Priced at $50.72. It is $10.76 higher than the current price, representing an upside of 26.93% and a margin of safety of 21.21%.

Risks of investing in Bank of America

Although I fundamentally believe BAC remains undervalued based on thinking about DDM and historical PB multiples, the stock has shown strong momentum since November, along with the overall index, and in these situations antiquities Big correction for stocks natural. From a technical point of view, the entry level is not the best as it is now Highest level in 52 weeks.

View Q1 BAC

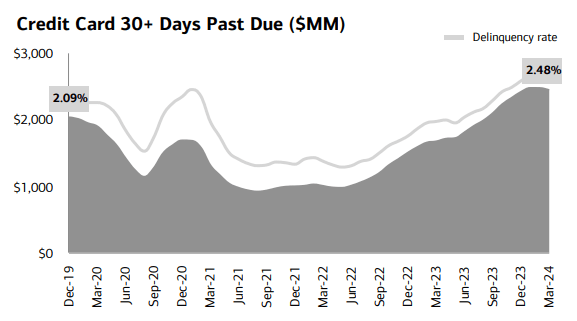

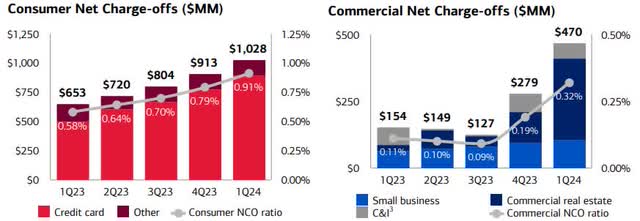

Now moving on to the reported results, there has been an upward trend in delinquency rates on credit cards. Although unemployment in the United States remains low, the era of fiscal transfers from the government during the pandemic is over, and if you couple that with higher interest rates, it will naturally lead to higher delinquency rates. From here, I expect the bank to become more restrictive on credit card limits due to the trend being shown.

View Q1 Baccalaureate

Taken together, the bank’s net debits increased each quarter from last year, again primarily due to increased credit card losses, but also due to its exposure to commercial real estate office loans affected by secular trends and rising interest rates. interest rates. Currently, the bank holds $17.4 billion in assets attributed to office properties, $7 billion of which is scheduled to mature in 2024. However, Bank of America remains well capitalized with a CET1 ratio of 11.8%, which It is 184 basis points above the regulatory requirements from Basel III.

BAC buy or sell?

In conclusion, this stock is definitely a buy. Based on the DDM model, it is undervalued, with a great margin of safety of 21.21% despite the recent rise in the stock price. Also, in terms of historical PB, it is at average, which provides room for further margin expansion if ROE normalizes and helps justify a higher multiple. At the same time, lowering interest rates would increase demand for loans, which would help improve National Insurance, which has been suffering from general declines, especially in consumer banking. Interest rate cuts can also help estimate unrealized losses that have been recorded in long-term assets over the past years, mostly due to higher interest rates.