arsenisperos/iStock via Getty Images

background

Welcome back to the seventh edition of Bank Buzz, where we cover the community banking sector, with a particular focus on remittances, our favorite sector.

It’s a fun space. Many of these are small banks They are inexpensive and have multiple incentives to increase shareholder value.

Our approach is to identify conversions trading below Tangible Book Value (TBV) with over capitalized balance sheets, strong asset quality, and shareholder friendly management teams.

Then wait for the drive to unleash the triggers.

In today’s article, we’ll provide a set of quick notes and then revisit our site NB Bancorp, Inc. (Nasdaq: National Bank of Bahrain) Investment thesis.

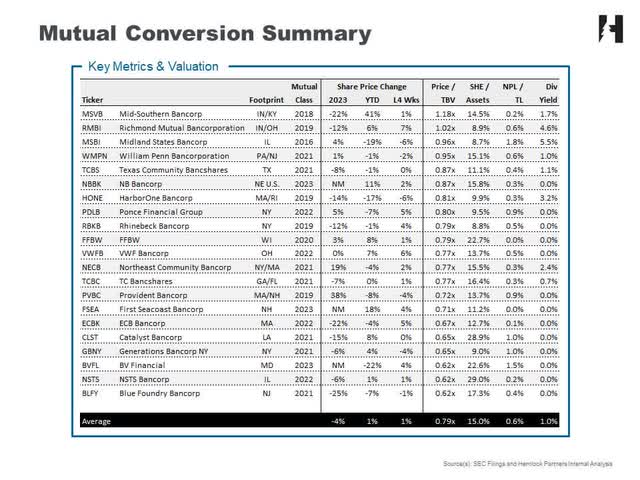

Comp table and quick clips

Earnings season is officially over. All 21 of our small banks reported first-quarter results, and here’s where they stand.

SEC filings and internal analysis of Hemlock

Buybacks

On Wednesday, Harbor One Bancorp (HONE) announced a new stock repurchase program, which allows the company to repurchase as many as 2.2 million shares (about 5%), or a total cost of $20 million. With the stock trading at around $10 per share, we expect HONE to pick up approximately 2 million shares, or about 4.8% of shares outstanding under the program. This ad is currently worth 81% TBV, which makes a lot of sense.

With expiration on June 6, 2024, Richmond Mutual (RMBI) has extended its stock repurchase program by 12 months. With 782,000 shares repurchased so far, the company has only used just over half of the total warrant (723,000 shares remaining). When trading TBV, we don’t expect a lot of activity in the near term, but we like to be flexible opportunistically in case the stock declines.

Although RMBI (4.6%) pays out a larger dividend yield than HONE (3.2%), we believe the latter is a better total return option because it offers a stronger capital position, a cleaner loan portfolio, and a lower-cost valuation.

Catalyst watch

William Penn Bancorporation (WMPN) celebrated its three-year anniversary in March and could be acquired at any time. Management is excellent, and a sale is only a matter of time.

Additionally, four banks became takeover targets in July, including: Blue Foundry Bancorp (BLFY), Northeast Community Bancorp (NECB), TC Bancshares (TCBC), and Texas Community Bancshares (TCBS).

Primarily due to loan quality concerns, BVFL Bank is down 22% in 2024 and now trades at just 62% of tangible book value. However, we are only two months away from the one-year anniversary of the conversion, which creates the possibility of a share repurchase announcement.

On a market capitalization basis, NB Bancorp, Inc. is The largest company in our coverage universe. Piper Sandler believes the bank will be added to the Russell 2000 (RTY) during the June rebalancing. This would enhance visibility going forward and likely boost the share price of this well-managed bank. With that in mind, let’s revisit NBB’s investment thesis.

National Bank of Bahrain: We are still optimistic

introduction

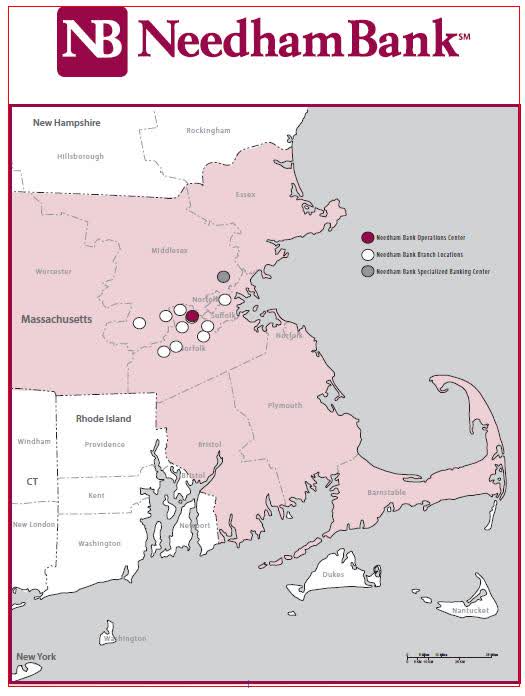

National Bank of Bahrain is the holding company for Needham Bank. Founded in 1892, the bank is headquartered in Needham, Massachusetts, and serves the greater Boston area and surrounding communities, including eastern Connecticut, southern New Hampshire and Rhode Island.

The bank’s footprint is shown below.

SEC filings

In December 2023, NBB completed its mutual conversion, making it a fully public institution.

Investment thesis

We maintain our Buy rating on NBB for the following reasons:

Attractive wallet: Asset quality is excellent, with the ratio of non-performing loans to total loans at 0.3% in the first quarter. To put this in context, the average NPL-to-TL ratio in our coverage universe is almost double, or 0.6%.

Strong balance sheet: With a tangible capital to assets (TC/A) ratio of approximately 16%, NBB has ample liquidity to enhance shareholder value through loan growth, dividends and share repurchases.

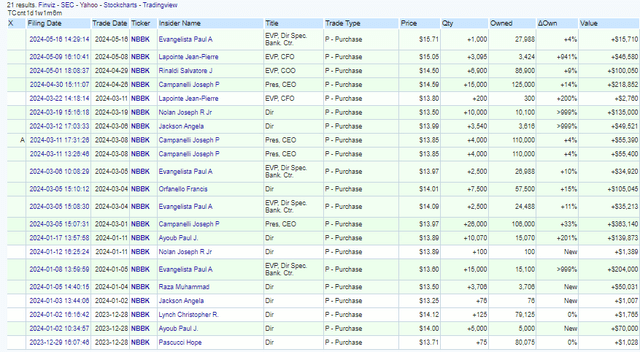

Inexpensive evaluation: As shown in the companies table above, the stock is trading at less than 90% TBV ($17.18 per share). This is inexpensive, given the quality of the work. Insiders seem to agree, with several recent purchases (see table below).

OpenInsider.com

Shareholder/Employee Consensus: Insiders own about 2% of the bank and an employee stock ownership plan owns another 8% – everyone wins as the share price rises.

Evaluation and risks

Looking ahead over the next three to five years, we expect management to stick to a well-established, shareholder-friendly “savings plan,” prioritizing conservative organic growth, dividends, prudent buybacks and, ultimately, a sale.

In the past, savings of about 130% of total turnover were obtained on average. To remain conservative, our approach designs an exit multiplier of 120% of the total workload.

For NBB, we expect book value per share to reach $20 by the end of 2026, suggesting an acquisition price of $25 per share or a return of ~70%.

Potential risks of our thesis include:

- Deterioration in the quality of the loan portfolio. As a community bank, NBB is highly exposed to economic conditions within its regional footprint.

- A material change in the local competitive environment may slow growth or reduce profitability.

- Leadership changes course and chooses to retain excess capital (versus returning it to shareholders via dividends and buybacks) or pursue a buy-side buyout.

Final thoughts

Despite having a significant capital position and attractive credit profile, NBB trades at just 87% of tangible book value. For patient long-term investors, we view the company as a relatively low holding, which offers a total return of around 70%.

Editor’s Note: This article discusses one or more small-cap stocks. Please be aware of the risks associated with these stocks.