Banks’ unrealized losses worsened in the first quarter after the interest rate-cutting mania briefly eased

Eternalcreative/iStock via Getty Images

The mania to cut prices eased the pain, but it’s over.

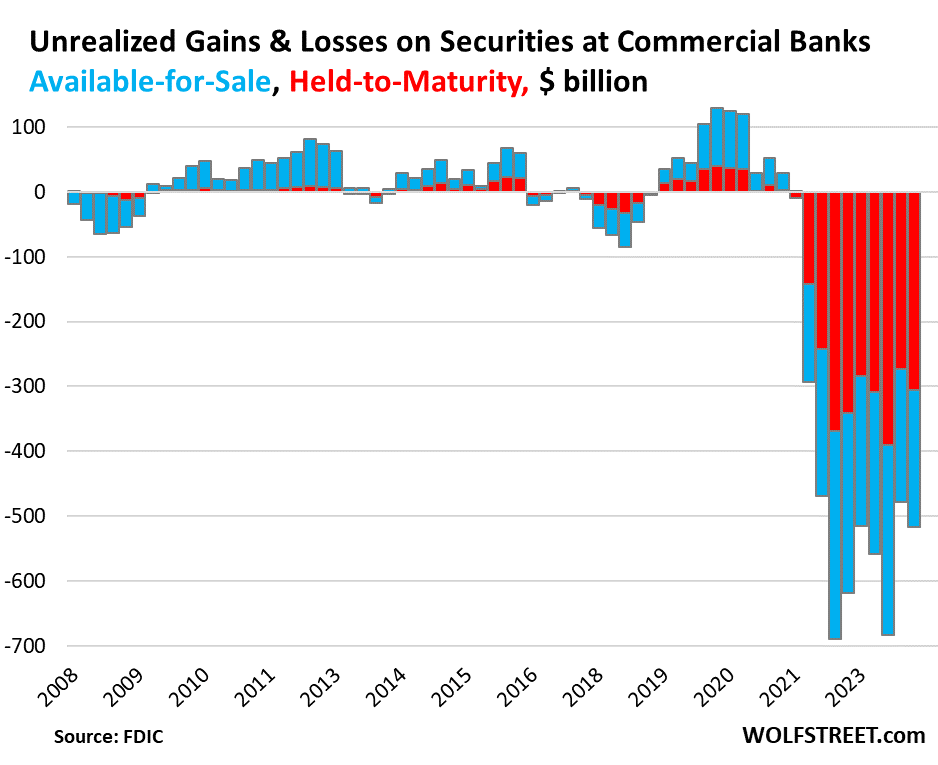

In the first quarter of 2024, “unrealized losses” on securities held by commercial banks increased by $39 billion (or 8.1%) compared to the fourth quarter to reach a cumulative loss of $517 billion. These unrealized losses amount to 9.4% of the total $5.47 trillion Securities held by those banks, according to the FDIC’s quarterly bank statements released today for the first quarter.

The securities are mostly Treasury securities and government-backed securities which do not produce credit losses, unlike loans where banks bear credit losses, especially in commercial real estate loans. These are pure securities whose market value has declined due to rising interest rates. When these securities mature—or in the case of MBS, when principal payments are made—the face value is paid to the holders of these securities. But even then, higher yields mean lower prices.

This is not achieved Losses were distributed over the securities accounted for in two ways:

- Held to maturity (HTM): +$31 billion in unrealized losses in Q1 from Q4 to a cumulative loss of $305 billion (in red).

- Available For Sale (AFS): + $8 billion unrealized losses in the first quarter from the fourth quarter to $211 billion (in blue).

HTM securities (in red) are valued at amortized purchase cost, and market value losses do not reach income in the equity portion of the balance sheet, but are noted separately as “unrealized losses.” It is with these HTM securities, and HTM accounting in general, that is where the problems lie.

Available-for-sale securities (in blue) are valued at market value, and losses resulting from changes in market value are taken against income in the equity section of the balance sheet.

The mania to cut prices eased the pain, but it’s over

Yields on longer-term securities began falling in November and bottomed out early this year amid a general mania for lowering interest rates. Lower revenues caused prices to rise, bringing unrealized losses in the fourth quarter down from massive levels in the third quarter.

But in the latter part of the first quarter, the interest rate cutting mania began to subside, yields rose again but did not return to October levels, so unrealized losses rose in the first quarter as well.

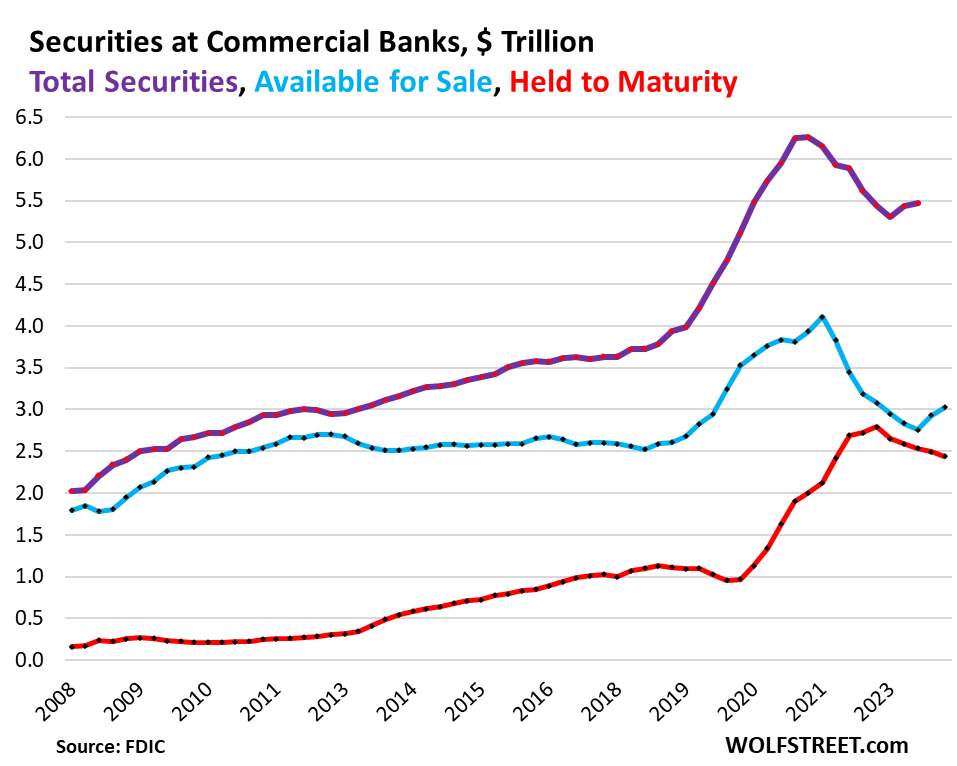

$5.47 trillion in securities held by banks

During the era of pandemic money printing, banks, flush with cash from depositors, loaded up on securities to put that cash to work, essentially loading it on long-term securities because they still had a clearly higher-than-zero yield, unlike short-term bonds. Long-term Treasury securities that were yielding zero, close to zero, and sometimes less than zero at the time. During that period, banks’ holdings of securities rose by $2.5 trillion, or 57%, to a peak of $6.2 trillion in the first quarter of 2022.

This turned out to be a massive miscalculation of future interest rates. The miscalculation has already caused four regional banks — Silicon Valley Bank, Signature Bank, First Republic and Silvergate Bank — to collapse in the spring of 2023 when panicked depositors withdrew their money.

In theory, the “unrealized losses” on securities held by banks do not matter because at maturity, the face value will be paid to the banks, and the unrealized loss diminishes as the security approaches its maturity date and reaches zero at maturity.

In fact, they are of great importance, as we saw with the four banks mentioned above after depositors discovered what was on their balance sheets and withdrew their money, forcing the banks to try to sell those securities, which would have forced them to take those securities. Losses, at which point there was not enough capital to absorb the losses, and the banks collapsed. Unrealized losses don’t matter unless they happen suddenly.

The value of securities held by banks rose in the first quarter to $5.47 trillion, after having already risen in the fourth quarter, but they were still down $786 billion, or 12.6%, from the peak in the first quarter (in purple in the chart below). ).

HTM securities have declined steadily from their peak in the fourth quarter of 2022, and fell further in the first quarter, to $2.44 trillion, down 12.7% from the peak (in red).

AFS securities rose for the second straight quarter to $3.02 trillion but remain 26.4% below the peak recorded in Q1 2022 (in blue).

Several factors account for the decline in securities on banks’ balance sheets from their peak, including:

- The portion of failed bank securities that the FDIC sold to nonbanks is no longer part of it.

- Banks have written down securities available with AFS to market value.

- Some securities have matured.

- Banks may have sold some securities.

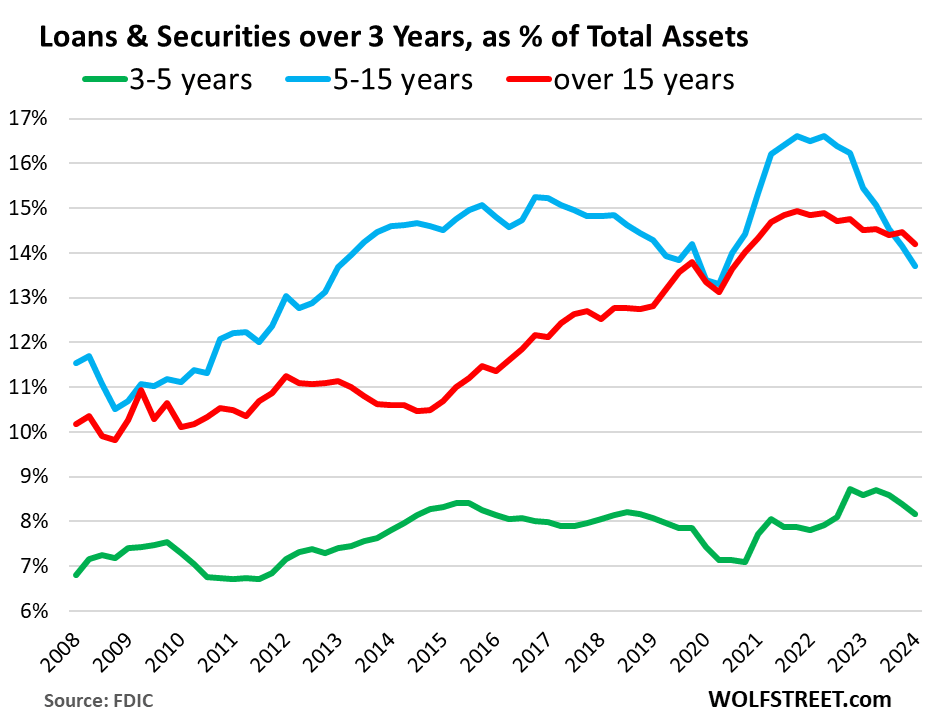

The longer the maturity period, the greater the interest rate risk

Interest rate risk—the risk that prices will fall as yields rise—increases with the term of the security or loan. The 30-year Treasuries sold in the summer of 2020 lost the most market value, while the 5-year Treasuries sold at the same time only have one year left to maturity and are trading at small losses from face value.

To measure these risks on banks’ balance sheets, the Federal Deposit Insurance Corporation (FDIC) provides data on securities and loans by remaining maturity:

- Least risky (green): 3-5 years: 8.2% of total assets.

- Riskiest (blue): 5-15 years: 13.7% of total assets, the lowest level since Q2 2020, after significant declines.

- Riskiest (in red): Over-15s: 14.2% of total assets, the lowest level since Q2 2020.

Original post

Editor’s note: The summary points for this article were selected by Seeking Alpha editors.