Evening pictures

Barings PDC (New York Stock Exchange: BBDC) It is a lending-focused business development company with good credit quality and a dividend payout ratio low enough to suggest that a dividend at the current run rate of $0.26 per share per quarter could be Be sustainable.

Barings BDC has received very positive reviews recently as the company has worked to resolve its credit issues and improve its non-accrual setup. Although the dividend is still covered by net investment income, I think additional capital raising will be difficult to achieve as the business development company has largely regained credit quality.

My evaluation history

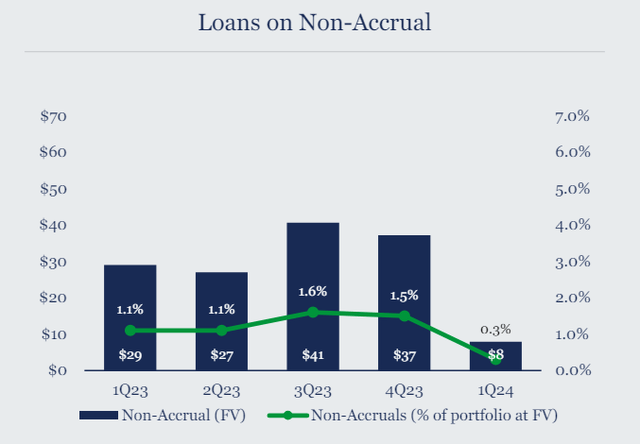

Barings BDC’s non-accrual trend improved significantly last quarter, with the company’s non-accrual ratio declining from 1.5% in 4Q23 to 0.3% in 1Q24. The improvement in credit quality was a catalyst for higher stock prices and lower discounting. On net asset value, which is what happened at my last census last February.The percentage was excessive, 22%.

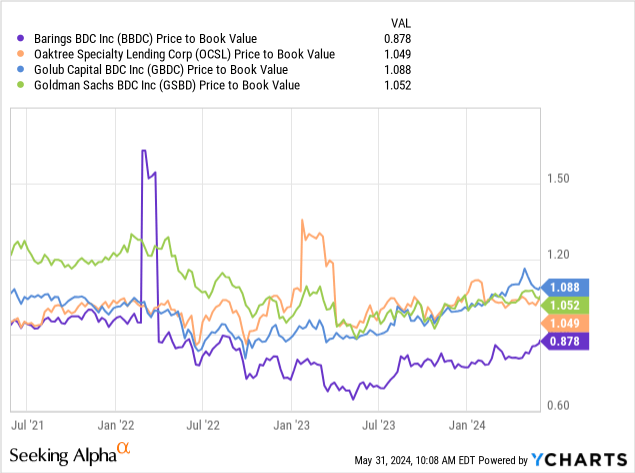

Since the NAV discount is down to 12%, and the Barings BDC has a slightly higher dividend payout ratio compared to last quarter, I’m recycling my investment dividends into another BDC that has recently fallen out of favor with passive income investors: Oaktree Specialty Lending (OCSL). This BDC has seen credit quality deteriorate recently, creating an opportunistic buying opportunity and leverage for earnings growth going forward.

Portfolio review

Barings BDC is a privately held, credit-focused business development company with a primary focus on senior secured lending products. At the end of the first quarter of 2024, Barings BDC maintained a dominant focus on senior secured lending at 72%, which represents a two percentage point decline from when I last reviewed the BDC in February of this year.

BDC has a higher than usual percentage of equity which has the potential to increase Barings BDC’s total returns if the company is able to achieve profitable equity exits.

Guaranteed focus for seniors (Barings PDC)

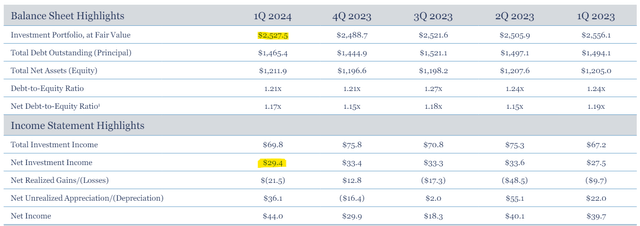

Barings BDC portfolio value reached $2.5 billion in Q1 2024, up 2% QoQ due to new innovations. The business development company also produced healthy underlying growth in net investment income, which passive income investors should use to determine dividend stability.

Barings BDC earned $29.4 million in net investment income in the first quarter of 2024, an increase of 7% year over year. Going forward, higher interest rates for a longer period could be a catalyst for national insurance growth, which depends on central bank stability.

If the central bank takes action and lowers short-term interest rates, Bangladesh Bank’s floating rate position of 97% will likely not be as valuable to the company and its shareholders as it was last year.

Highlights of the balance sheet (Barings PDC)

The main consideration that prompted my change in rating on Barings BDC stock relates to a business development company experiencing improvement in its underlying credit quality. In the first quarter of the current fiscal year, Baring’s BDC nonaccrual ratio fell to 0.3%, down from 1.5% in the previous quarter. Better credit quality in BDC’s debt portfolio is also the primary reason for BDC stock’s 15.4% upward rerating so far in 2024.

Non-accrual loans (Barings PDC)

The dividend payout ratio still looks good

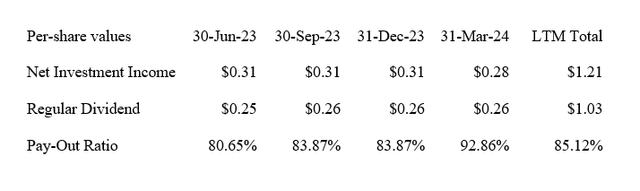

Barings BDC earned $0.28 per share in net investment income last quarter which was more than enough to cover the steady $0.26 per share per quarter dividend payout.

With a dividend payout ratio of 93% in the last quarter and 85% in the last 12 months, I believe the dividend is adequately supported by net investment income and is not at risk of being cut.

However, I think it’s fair to point out that the dividend payout ratio has risen recently, due to lower net investment income, reducing the margin of dividend safety for passive income investors.

I don’t think Barings BDC is willing to cut its dividend, but the dividend trend has been leaning toward negative in the past year.

Dividend (The author created a table using BDC information)

Lower business value (BV) discount driven by improved credit quality

In February, Barings BDC recommended to passive income investors that when stocks are sold, they add a discount to book value of 22%. Given the positive impetus from the improving credit backdrop, the discount to BBDC’s book value has fallen to 12% today.

However, I believe BDC has much less upside given its non-accrual ratio improved much in Q1 2024, making the stock less compelling for passive income investors looking for capital appreciation as well as recurring and covered leverage. Dividend.

The net asset value of Barings BDC as of March 31, 2024 was $11.34, which reflects the underlying intrinsic value of the BDC. Considering that Barings BDC’s payout ratio rose in Q1 2024 and that BDC now has less potential to grow its dividend as its credit profile recovers, I think BBDC presents a less compelling value proposition than it did in February.

Why an investment thesis may or may not work?

I am adjusting my stock rating to ‘hold’ as BDC has now seen a significant improvement in its non-accrual ratio. As such, I believe the upside potential may now be limited, although I also believe earnings are not headed for the chopping block.

As I explained above, Barings BDC had a dividend payout ratio, based on net investment income, of 93% which is enough to cover the dividend. However, the margin of dividend safety declined last quarter and passive income investors should remain aware of this.

deductive

I recommended Barings BDC to passive income investors in February because I thought the 21% discount to net assets was excessive at the time. The catalyst for the stock price rise was the successful restoration of BDB’s credit quality profile in the last quarter.

Dividends are still strongly covered by net investment income, but the dividend payout ratio has increased quarter-on-quarter to over 90% and the trend is slightly negative. I think the dividend is sustainable here, but I see less upside potential for the stock when considering the big jump in the share price this year.

As a result, I am adjusting my stock rating to “hold” and recycling the profits from my investment into another BDC that is also currently experiencing a high non-accrual ratio, Oaktree Specialty Lending.