Daria Guseva/iStock via Getty Images

Investment thesis

Having endured a difficult period since 2022, the business recently showed a significant improvement in profitability resulting in lower cash burn during its 2024 financial year which ended on 31 March. Guidance for next year calls for almost no organic growth and weak margins, limiting the upside in the stock price today. Despite having a strong balance sheet and a cheap valuation, I think it’s wise for investors to wait on the sidelines until the company can re-stimulate its revenue growth and demonstrate its ability to generate much higher margins.

Company overview

barking (New York Stock Exchange: Bark) provides a direct-to-consumer subscription service for dog toys and treats. The company leverages its brand to sell food, dental products and other accessories for dogs through its website as well As retail partners. The company went public Via SPAC In July 2021, it was valued at $1.6 billion with revenue Growth rates well above 50%.

As pandemic-related tailwinds faded, the company struggled to show profitable growth. Company co-founder Matt Meeker returned to the CEO position in January 2022 and has focused on the company’s profitability at the expense of growth. This led to a restructuring of the company in February and July last year, which resulted in a workforce reduction of approximately 20%. These actions, combined with inventory reduction, helped the company significantly reduce its cash burn to $2.8 million in fiscal 2024, compared to $16.6 million in fiscal 2023.

Financial highlights

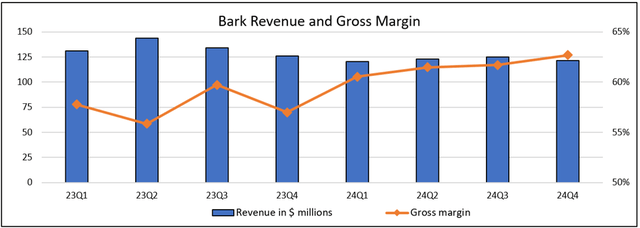

Gross margins rise despite lower revenues

Created using company data

The company’s growth has been largely stagnant in recent quarters as shown above, after seeing sharp declines during FY23. The company faced declines in both DTC and commerce channels. In the latest quarter, merchandising revenue was up 21% year over year but represented only 11% of BARK’s total revenue. On the other hand, DTC revenue declined 5.7% in the quarter. Overall, the company’s revenue declined 8.4% in fiscal 2024 compared to the previous year. On the positive side, the steady improvement in the company’s gross profit margins resulted in gross profit declining by only 1.9% by comparison.

Management’s guidance for FY25 calls for revenue of $495 million at the midpoint, which would represent almost no organic growth. This was well below analyst estimates. During the fourth quarter 2024 earnings call, the CEO pointed to some potential tailwinds for the company from pet adoptions when he said:

As you heard from Chewy (CHWY) last week, they reported that calendar quarter was the first time since 2022 that adoptions were greater than abandonments within shelters. This is a positive sign.

Profitability has improved, but is still weak

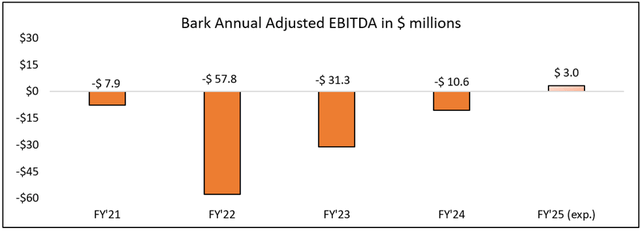

Created using company data

As shown above, the company showed a dramatic improvement in its profitability with Adjusted EBITDA losses declining from -$31.3 in FY23 to -$10.6 in FY24. This was primarily driven by the company’s focus on reducing operating expenses as well as To seek to increase gross margins.

Management’s guidance for next year calls for an adjusted EBITDA of $3 million at the midpoint. This means an adjusted EBITDA margin of just 0.6%. Furthermore, the company is likely to achieve negative free cash flow next year, as maintenance capex of about $9 million is well above expected EBITDA. In FY25, the company’s cash flow fund will also benefit to a lesser extent from the inventory decline that occurred the previous year, as inventory levels have now largely returned to normal.

balance sheet

The company has a cash position of $125 million offset by debt approaching $40 million. Its net cash position of $85 million has given it the opportunity to double the share repurchase program it began last year, to $15 million, representing about 6% of its current market value.

evaluation

At a share price of $1.4, the company is worth about $165 million, after accounting for its net cash. Given an expected EBITDA of $3 million for FY2025, this means an EV to Adjusted EBITDA ratio of 55. Given the somewhat lower EBITDA margins expected for next year, I think it’s more important to evaluate a business on an EV to revenue basis and use that metric to compare it to peers like Chewy. BARK is trading against EV for just 0.33 forward earnings. By comparison, Chewy trades at a multiple of 0.73, which is more than double BARK’s valuation. There’s clearly plenty of room to revalue BARK to a higher level if it can grow its EBITDA margins to close to Chewy’s margins, which are expected to be around 4%.

Potential growth stimulants

The company has ambitious plans to significantly increase its merchandising revenue through retail partners like Target and PetSmart, as its CEO described during its fourth-quarter earnings call:

Trade this year was about 11% of our revenue in fiscal 2024. Next year we expect it to be about 12% to 13% of our revenue. And then, looking beyond fiscal year 2026, over the next three years, we expect commerce to be about 30% to 35% of our business.

The company recently launched BARK Air by partnering with a jet charter company to address the challenge many dog owners face when traveling long distances with their pets. BARK CEO praised the program’s success during the fourth quarter earnings call, saying:

Since its announcement in April, the response has been amazing. BARK Air has received more coverage than anything else in BARK’s 12-year history. Here are some numbers from the first month before the first flight took off. BARK Air has over $1 million in bookings, and many of our flights are already sold out. Since there are only a few days left until actual flight operations begin, we will need more time to report the results here. However, it is clear that the effect on consciousness is amazing.

Although BARK Air’s impact on the company’s overall profitability is likely limited, it does help increase BARK brand awareness among consumers, which should in turn help fuel its growth.

Risks

The company operates in a very competitive space in the pet industry. This in turn poses a major challenge to its profitability. Despite management’s aggressive measures, adjusted EBITDA and free cash flow remain fairly weak, which may lead investors to believe there are structural issues with the profitability of its business model. Additionally, if significant headwinds emerge in the coming quarters, the company will likely suffer since pet toys and treats are somewhat discretionary in nature.

Conclusion

BARK’s future looks somewhat disappointing as management expects almost no revenue growth and weak profitability in FY25. However, the company has a strong financial position and is returning cash to shareholders through buybacks. The company is trading at a very cheap valuation and would likely be a takeover target for a larger player. Although potential catalysts exist, it remains to be seen if they can reignite the company’s growth in the future. Until there is evidence of this happening, I think it is wise for investors to remain on the sidelines.