Brett_Hondo

Investment thesis

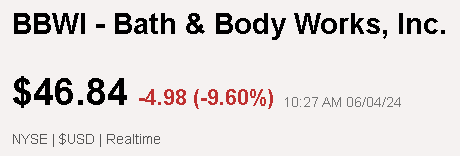

After impressive results in the first quarter of 2024, where the company exceeded guidance provided by management during the fourth quarter of 2023, Bath & Body shares are down nearly 10%, which seems a bit counterintuitive to me given the high revenues and EPS. while A 0.9% decline in revenue is not a positive in and of itself, and considering that the guidance was for a 2-4% decline this quarter, you can understand why I’m bullish on the company.

I think the guidance for FY2024 was conservative given the economic uncertainty, but the company will likely end up in or even exceeding the high range, so it will end up trading at an attractive P/E of 13-14, making it a buy. At the current price.

Find the price of Alpha BBWI

A giant in the perfume industry

Bath and Body Works (New York Stock Exchange: BBWI) is one of the most popular brands among people looking for perfumes, personal care creams, soaps, candles, air fresheners, home fragrances and any other type of flavoring products.

According to IBISWorld Industry Reports, BBWI will have approximately 5% market share in the competitive beauty, cosmetics and fragrance store industry. This is very interesting if we consider that they are only dedicated to fragrances and do not offer cosmetics, as does Ulta Beauty (ULTA), which IBIS estimates has a market share of 20%, or Sephora (OTCPK:LVMHF) with a market share of almost 20%. 7%. So, we can say that Bath & Body has almost a monopoly on perfume product stores.

However, if we were to keep BBWI’s competitors in mind, Ulta Beauty and Sephora would be the biggest competitors out there, while Victoria Secret, The Body Shop, and even stores like Walmart or Target would be somewhat “minor” competitors, although also important. .

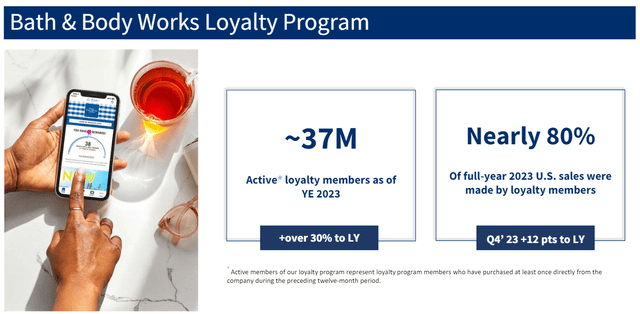

Successful loyalty program

Bath & Body, like other brands in this sector, has a loyalty program that offers you points for every dollar you spend. In your particular case, for every $1 you spend, you get 10 points and once you reach 1,000 points (or $100) in spending, you’ll get a coupon that allows you to get a free item worth up to $16.50, which will represent up to 16.5% cash back. It is delivered in the form of products.

It’s a great rewards program, so it’s no surprise that according to 2023 numbers, the company has reached 37 million members, which is impressive considering Ulta Beauty has about 43 million members. This is important because it encourages repeated consumption, which was already something of the kind in the case of BBWI, keeping in mind that when you run out of lotion or home fragrance, the first thing you want is to replace it.

Presentation for bath and body investors

Q12024 Routing bypass

On June 4, the company announced corresponding results for the first quarter of 2024, which exceeded expectations. Net sales of $1.4 billion beat analysts’ expectations of $1.37 billion and EPS of $0.38 was a big surprise compared to expectations of $0.33, given the downbeat guidance we had for full-year 2024.

At the end of the fourth quarter of 2023, management commented that it expects sales to decline between 3% or remain flat through the year, while it expects sales in the first quarter of 2024 to decline between 2% and 4.5%. The result was a decline of only 1% in the first quarter of 2024, which makes me believe that management is conservative in its forecasts and there is real potential to meet the high range of guidance.

Another example of this is that the company has narrowed its guidance and now expects EPS to be between $3.05 and $3.35 (previously forecasting between $3 and $3.35). A small change, but relevant when evaluating the possibility of beating expectations (as in Q1) or at least finishing in the high range of this guidance.

Full-year 2024 diluted earnings per share are now expected to be between $3.05 and $3.35, compared to diluted earnings per share of $3.84 and adjusted earnings per diluted share of $3.27 in fiscal 2023. The company’s full-year guidance includes the expected impact Approximately $300 million in cash was distributed on stock buybacks.

The second quarter of 2024 is expected to be better and the guidance is for net sales to range from a 2% decline to flat. If the company can improve on this score, which does not seem difficult to overcome, I think the market could become very positive about BBWI.

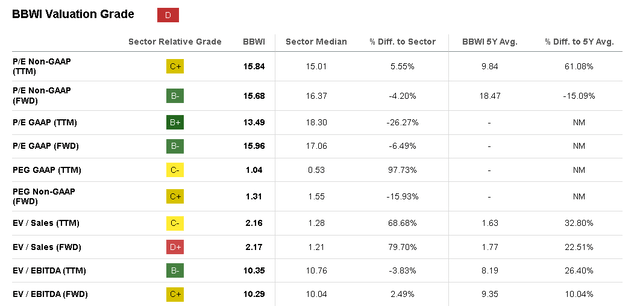

evaluation

With current guidance of $3-$3.35 EPS, the company will trade at a forward EPS of 14-15, which is within the industry, market and company average. Therefore, if it remains in the low guidance range, it will not be expensive to trade and can be considered a good buy currently.

While the current valuation looks good, that’s largely due to the fact that shares fell 10% after the presentation. In my opinion, there is nothing that makes me think that this decline is justified, other than the fact that before the price adjustment the valuation was not very attractive.

Seeking alpha

Risks

When thinking about the risks of Bath & Body, the first thing I think of is competition and how it can intensify in an adverse economic environment for the consumer. First, because BBWI has much less variety than Ulta or Sephora in terms of product range, offering only fragrance-related products. Although you won’t find scented candles at Ulta stores, it’s a good idea to plan on purchasing your perfume and makeup in the same place (which is a fairly common plan).

In addition, BBWI offers its own branded products, and although they are of high quality, they also come at a higher price. So when I want to save a few dollars on scented hand sanitizer, I prefer to choose a generic brand from Walmart, even if the shopping experience isn’t the same. So, I don’t think Bath & Body is as good a company as Ulta, Sephora, or even Sally Beauty (SBH), although I do think it’s the best company in its space.

Bottom line

As can be seen throughout the article, I am more inclined to believe that management is conservative and given the strength of the company’s brand and frequent use of its products, the results will be in the high range of guidelines rather than I would rule out beating them. This means that the company is trading at a forward P/E of 13-14, and we would have a margin of safety in terms of its average valuation.